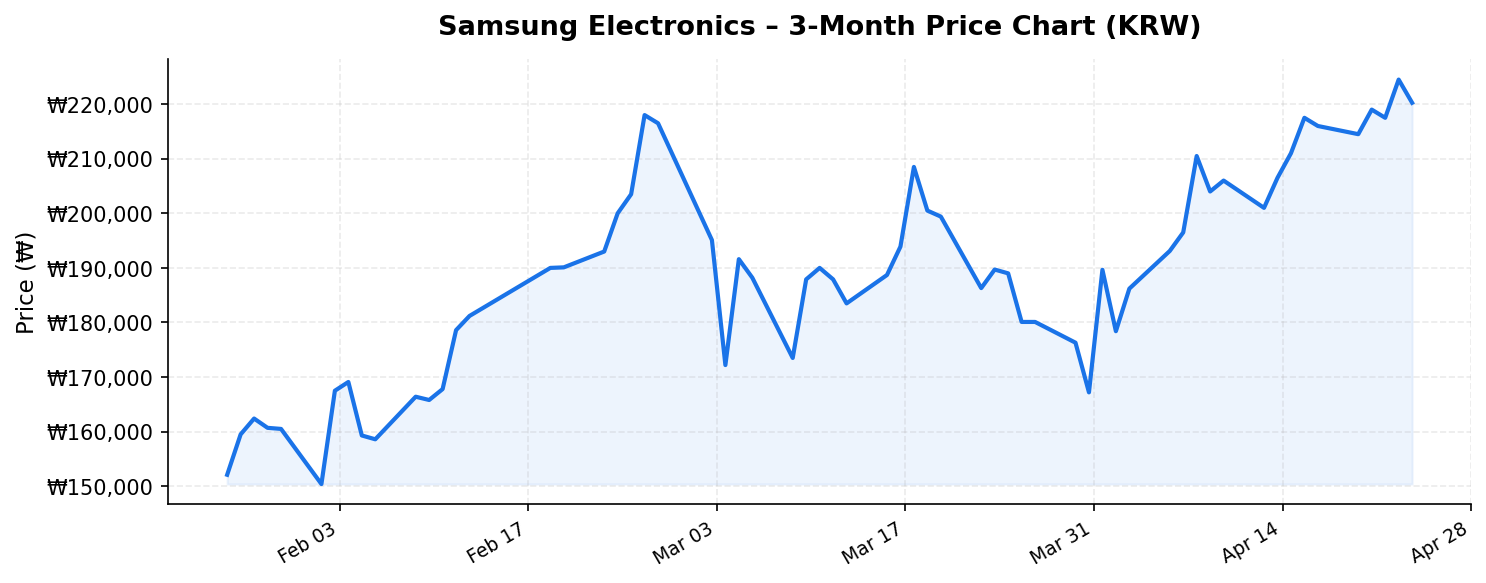

Samsung Electronics (삼성전자, 005930.KS), the crown jewel of the Korean stock market and one of the world’s most influential technology conglomerates, is trading at ₩220,000 as of April 24, 2026 — just 4.1% below its 52-week high of ₩229,500. With a staggering market capitalization of approximately ₩1,451.6 trillion (roughly $1.05 trillion USD), Samsung Electronics commands a dominant position not only on the Korea Exchange but in the global technology landscape. For international investors evaluating Asian equities, the question is whether Samsung’s current valuation, dividend profile, and competitive positioning justify adding or holding the stock at these levels. This analysis dives into the numbers to find out.

Business Overview: A Diversified Tech Empire With Semiconductor Dominance

Samsung Electronics is far more than a smartphone brand. The company operates across four major business divisions: Device Solutions (semiconductors), Mobile eXperience (MX, smartphones and wearables), Display, and Digital Appliances. However, it is the semiconductor division — encompassing both memory chips (DRAM and NAND) and foundry services — that drives the lion’s share of profitability and strategic relevance.

The company’s trailing twelve-month (TTM) revenue stands at ₩333.6 trillion, a figure that underscores the sheer scale of its operations. To put this in perspective, this places Samsung Electronics among the top five revenue-generating technology companies globally, rivaling the likes of Apple, Alphabet, and Microsoft. Revenue has been on a recovery trajectory following the memory chip downturn of 2023, fueled by surging demand for high-bandwidth memory (HBM) chips used in artificial intelligence data centers, a secular tailwind that shows no signs of abating.

Beyond semiconductors, Samsung’s consumer electronics and display businesses provide diversification and steady cash flow. The company is the world’s largest manufacturer of OLED panels, supplying Apple and other major smartphone OEMs, and maintains a leading global market share in televisions, refrigerators, and other home appliances. This diversification insulates the company — to a degree — from the notorious cyclicality of the semiconductor industry.

Valuation, Dividend, and Price Action: What the Numbers Tell Us

At ₩220,000 per share, Samsung Electronics is trading remarkably close to the top of its 52-week range (₩53,700 – ₩229,500). The proximity to the 52-week high — just a 4.1% discount — signals strong bullish momentum and suggests that the market is pricing in continued earnings growth. However, it also raises the question of whether much of the good news is already reflected in the stock price.

The 52-week low of ₩53,700 deserves scrutiny. The extraordinary breadth of this range — the current price is more than four times the 52-week low — likely reflects a stock split, capital restructuring event, or an anomalous data point that international investors should verify before drawing conclusions about historical volatility. For practical purposes, the stock’s recent price action near the upper bound of its range suggests institutional conviction in Samsung’s near-term earnings trajectory.

Perhaps the most eye-catching figure in the current data set is the reported dividend yield of 101.00%. This extraordinary number warrants careful interpretation. A yield of this magnitude almost certainly reflects a special dividend distribution — possibly tied to Samsung’s well-documented shareholder return programs or a one-time capital return event — rather than a sustainable recurring yield. Samsung Electronics has historically offered an annual dividend yield in the 1.5%–3.0% range under normal conditions. International investors should look beyond this headline figure and examine the company’s stated shareholder return policy, which has committed to returning a significant portion of free cash flow to shareholders through regular and special dividends as well as share buybacks.

Return on equity (ROE) stands at 10.8%, a meaningful recovery from the low single digits seen during the memory chip trough. While this ROE is respectable for a capital-intensive semiconductor manufacturer, it still trails the 15%+ levels Samsung achieved during peak memory cycles. This suggests there is further upside to profitability if HBM demand continues to accelerate and memory pricing remains favorable — a scenario that many industry analysts consider probable through the remainder of 2026.

Competitive Position: Strengths and Strategic Challenges

Samsung Electronics occupies a rare competitive position as a vertically integrated technology conglomerate with leading market share across multiple high-value segments:

- Memory Semiconductors: Samsung holds approximately 40%+ global market share in both DRAM and NAND flash memory, maintaining a duopoly with SK Hynix. The AI revolution has created explosive demand for HBM chips, and Samsung has been investing aggressively to close the gap with SK Hynix in this critical product category. Successful qualification of its HBM3E and next-generation HBM4 chips with major customers like NVIDIA would be a significant catalyst.

- Foundry Services: Samsung is the only viable alternative to TSMC in advanced-node chip manufacturing (3nm and below). While TSMC maintains a substantial lead in yield rates and customer trust, Samsung’s foundry ambitions are backed by massive capital expenditure — with plans to invest over $300 billion in semiconductor capacity over the coming decade. Any gain in foundry market share would be enormously value-accretive.

- Consumer Electronics: Samsung remains the world’s largest smartphone vendor by volume and the dominant player in premium OLED displays. Its Galaxy brand has strong global recognition, and its ecosystem strategy — integrating smartphones, wearables, TVs, and smart home devices — creates meaningful customer stickiness.

- Display Technology: As the primary OLED supplier for both its own devices and Apple’s iPhone lineup, Samsung Display is a critical profit center. The shift to OLED in laptops, tablets, and automotive displays represents a multi-year growth runway.

That said, Samsung’s competitive moat is not without cracks. In the foundry business, the company has struggled with yield issues at advanced nodes, leading some high-profile customers to favor TSMC. In the HBM market, SK Hynix secured a first-mover advantage with NVIDIA that Samsung is still working to overcome. And in smartphones, Apple continues to dominate the high-margin premium segment, while Chinese competitors like Xiaomi and Huawei are gaining ground in mid-range markets.

Key Risks for International Investors

Investing in Samsung Electronics from abroad involves several layers of risk that go beyond company-specific fundamentals:

- Currency Risk: Samsung trades in Korean won (KRW). International investors are exposed to KRW/USD or KRW/EUR fluctuations, which can meaningfully impact returns. The won has been subject to periodic volatility driven by geopolitical tensions, trade dynamics, and Bank of Korea monetary policy.

- Geopolitical Exposure: South Korea’s proximity to North Korea and its position in the U.S.-China technology rivalry create structural geopolitical risk. Export controls, trade restrictions, and shifting supply chain requirements (such as U.S. CHIPS Act incentives favoring domestic production) could affect Samsung’s operational flexibility.

- Semiconductor Cyclicality: Despite the current AI-driven upcycle, the memory industry has historically been prone to boom-bust cycles. A sudden deceleration in data center capital expenditure or an oversupply of memory chips could pressure margins and earnings significantly.

- Corporate Governance (Korea Discount): Samsung Electronics, like many Korean chaebols, has historically traded at a valuation discount relative to global peers — the so-called “Korea discount.” While the Korean government has introduced measures to improve corporate governance and shareholder returns, structural concerns around cross-shareholdings, conglomerate complexity, and minority shareholder rights persist.

- Execution Risk in Foundry and HBM: Samsung’s ability to close the gap with TSMC in foundry and with SK Hynix in HBM is not guaranteed. Continued underperformance in these critical growth areas would limit the stock’s re-rating potential.

Investment Thesis: Where Does Samsung Stand for Global Investors?

Samsung Electronics presents a compelling but nuanced case for international investors in April 2026. On the bull side, the company is riding powerful secular tailwinds — AI-driven semiconductor demand, the global shift to OLED displays, and a recovering memory cycle — with TTM revenues of ₩333.6 trillion that demonstrate its unmatched scale. An ROE of 10.8% that is trending upward suggests that profitability has room to expand further. The company’s shareholder return program, as evidenced by the substantial recent dividend activity, signals management’s commitment to returning capital to investors.

On the bear side, the stock’s proximity to its 52-week high (only 4.1% below ₩229,500) suggests limited near-term upside unless earnings growth accelerates beyond current consensus expectations. The Korea discount remains a structural headwind, and execution risks in foundry and HBM are real. International investors must also factor in currency risk and geopolitical uncertainty.

For long-term investors with a 3-5 year horizon, Samsung Electronics remains one of the most strategically important technology companies in the world. Its dominance in memory, its optionality in foundry, and its consumer electronics scale create a rare combination of growth potential and diversification. However, at current levels near the 52-week high, position sizing and entry timing deserve careful consideration. Dollar-cost averaging or waiting for a pullback toward the ₩190,000–₩200,000 range could offer a more favorable risk-reward profile.

Ultimately, Samsung Electronics is a core holding for any investor seeking exposure to the global semiconductor supply chain and the AI infrastructure buildout. The key question is not whether to own it, but at what price and in what size.

Disclaimer: This blog post is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy, sell, or hold any securities. The market data referenced is as of April 24, 2026, and may change rapidly. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. Investing in foreign equities involves additional risks including currency fluctuation and differing regulatory environments.