In a market where high-growth technology companies rarely offer substantial income to shareholders, Isu Petasys (이수페타시스, 007660.KS) stands out as a remarkable anomaly. Trading at ₩152,300 as of April 30, 2026, with a staggering 16.00% dividend yield and a return on equity of 29.6%, this Korean printed circuit board (PCB) specialist has transformed itself from a mid-cap industrial player into an ₩11.2 trillion market cap powerhouse. For international investors seeking exposure to the AI infrastructure buildout and advanced electronics supply chain, Isu Petasys demands serious attention — but so do the risks that accompany its meteoric rise.

Business Overview: From Niche PCB Maker to AI Infrastructure Beneficiary

Isu Petasys is a South Korean manufacturer specializing in high-layer-count printed circuit boards (MLB — Multi-Layer Boards) used in servers, networking equipment, telecommunications infrastructure, and increasingly, AI accelerator systems. A subsidiary of the Isu Group conglomerate, the company has operated in the PCB space for decades, but its fortunes have been radically reshaped by the explosive demand for AI-related hardware.

The company’s core competency lies in producing ultra-high-layer PCBs (20+ layers) that are essential for high-performance computing servers, GPU-based AI training clusters, and next-generation 800G/1.6T networking switches. These are not commodity products — manufacturing multi-layer boards with the precision, thermal management, and signal integrity required for AI workloads demands specialized expertise and significant capital investment, creating meaningful barriers to entry.

With trailing twelve-month revenue of ₩1.1 trillion, Isu Petasys has experienced extraordinary top-line growth. To put this in perspective, the company’s revenue was approximately ₩300-400 billion just two to three years ago, meaning the business has nearly tripled in scale. This growth trajectory is directly tied to the global surge in AI data center construction, where hyperscalers like Microsoft, Google, Amazon, and Meta are spending tens of billions of dollars annually on infrastructure that requires exactly the type of advanced PCBs Isu Petasys produces.

Valuation and Market Performance: Parsing the Numbers

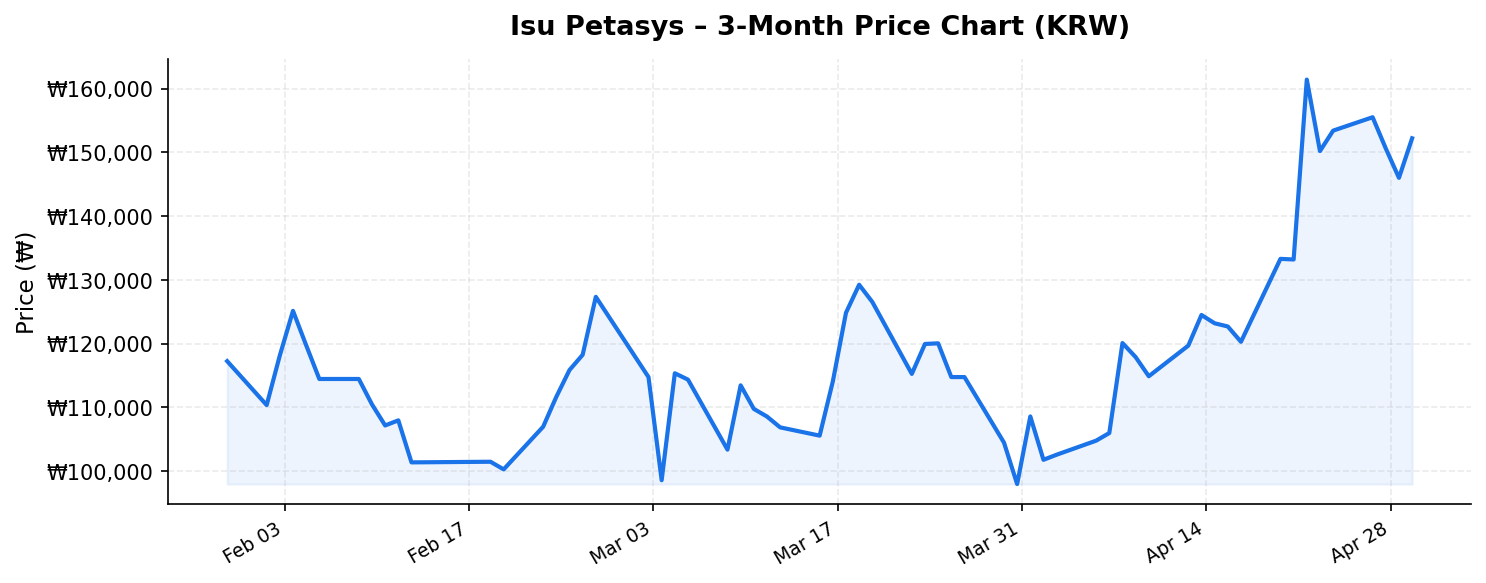

The stock’s 52-week range of ₩31,850 to ₩164,400 tells a dramatic story. At its current price of ₩152,300, Isu Petasys trades just 7.4% below its 52-week high and has appreciated roughly 378% from its 52-week low. This kind of price action reflects a fundamental re-rating of the business as investors priced in the structural shift toward AI-driven PCB demand.

At a market capitalization of ₩11.2 trillion against ₩1.1 trillion in TTM revenue, the stock trades at approximately 10.2x price-to-sales. For a hardware component manufacturer, this is a premium valuation by traditional standards. However, the 29.6% return on equity suggests this is no ordinary component maker — the company is generating exceptional profitability that justifies a significant premium over commodity PCB peers. For context, ROE levels approaching 30% are more commonly associated with asset-light software businesses or dominant brand-driven consumer companies, not industrial manufacturers.

Perhaps the most eye-catching figure is the 16.00% dividend yield. At first glance, this seems almost too good to be true, and international investors should examine this figure carefully. A yield this high typically signals one of three things: the market expects the dividend to be cut, the stock price has recently collapsed (which is clearly not the case here), or the company is returning an extraordinary proportion of its profits to shareholders during a period of peak earnings. Given the stock’s proximity to its 52-week high, the latter explanation appears most likely — Isu Petasys is likely distributing a large share of its dramatically increased earnings as dividends. The sustainability of this payout level depends entirely on whether current demand conditions persist.

Competitive Position and Growth Catalysts

Isu Petasys operates in a competitive landscape that has, paradoxically, become more favorable as the technology demands have intensified. The global high-end PCB market is dominated by a handful of Taiwanese, Japanese, and Korean manufacturers. Key competitors include:

- Unimicron (Taiwan) — The world’s largest PCB manufacturer and a major supplier to AMD and Intel

- Ibiden (Japan) — A key substrate and PCB supplier for Intel’s server platforms

- Samsung Electro-Mechanics (Korea) — A diversified component maker with PCB capabilities

- TTM Technologies (USA) — A significant player in aerospace and defense PCBs

What differentiates Isu Petasys is its focused specialization in ultra-high-layer networking and server PCBs, combined with its qualification as a supplier to major North American hyperscalers and networking OEMs like Cisco, Arista, and Broadcom’s ecosystem partners. Customer qualification in the high-end PCB space typically takes 12-18 months, creating meaningful switching costs that protect incumbent suppliers.

Several catalysts continue to support the growth thesis:

- AI training and inference infrastructure expansion: Global AI capex continues to accelerate in 2026, with major hyperscalers increasing their spending commitments. Each AI server rack requires multiple high-layer PCBs.

- Networking upgrade cycle: The transition from 400G to 800G and 1.6T ethernet switching drives demand for more complex, higher-layer-count PCBs in networking equipment.

- Capacity expansion: Isu Petasys has been aggressively investing in new manufacturing capacity, including facility expansions in Korea, to capture growing order volumes.

- Geopolitical supply chain diversification: As global customers seek to diversify away from concentrated Taiwanese supply chains, Korean PCB manufacturers benefit from “China+1” and “Taiwan+1” sourcing strategies.

Key Risks: What Could Go Wrong

Despite the compelling growth story, international investors must weigh several material risks before allocating capital to Isu Petasys:

Cyclicality and peak earnings risk: The semiconductor and electronic component industries are notoriously cyclical. The current AI spending boom has driven extraordinary demand, but any slowdown in hyperscaler capex — whether due to macroeconomic weakness, shifts in AI investment sentiment, or overcapacity concerns — could rapidly compress revenues and margins. The 16% dividend yield may itself be a signal that the market harbors some skepticism about the permanence of current earnings levels.

Valuation compression: At 10.2x trailing revenue and near its 52-week high, much of the good news appears priced in. Any earnings miss or guidance reduction could trigger significant downside given the elevated expectations embedded in the stock price. The 378% appreciation from the 52-week low leaves substantial room for a pullback.

Customer concentration: High-end PCB suppliers often derive a significant portion of revenue from a small number of large customers. Loss of a major hyperscaler or OEM account could have an outsized impact on financial results.

Currency risk: For international investors, the Korean won introduces an additional layer of volatility. A strengthening won benefits foreign holders of KRW-denominated assets, but a weakening won can erode returns even if the stock price appreciates in local currency terms.

Capacity expansion execution: Rapid expansion carries execution risk. Delays in bringing new capacity online, cost overruns, or yield issues at new facilities could impact profitability during a critical growth phase.

Competition from Chinese manufacturers: While Chinese PCB makers have historically focused on lower-end products, their technological capabilities are advancing. Any breakthrough in high-layer-count manufacturing by Chinese competitors could pressure pricing and market share over the medium term.

Investment Thesis: A Compelling but High-Conviction Play on AI Infrastructure

For international investors, Isu Petasys represents a concentrated bet on the continued expansion of AI infrastructure — specifically, the physical layer of computing hardware that often gets overlooked in favor of more glamorous chip designers and software platforms. The investment case rests on several pillars: a structural demand tailwind from AI and high-performance networking, demonstrated execution evidenced by the near-tripling of revenue, elite profitability with a 29.6% ROE, and a remarkably generous 16% dividend yield that provides substantial income while investors wait for further appreciation.

The stock’s position just 7.4% below its 52-week high suggests the market broadly agrees with this bullish narrative. However, the magnitude of the rally from ₩31,850 to ₩152,300 means that latecomers face a meaningfully different risk-reward profile than early investors. Position sizing is critical — this is a stock with the potential for further upside if AI spending continues to accelerate, but also one that could experience sharp corrections if the cycle turns.

For investors who believe the AI infrastructure buildout is still in its early innings — a view supported by the continued acceleration of hyperscaler capex commitments through 2027 and beyond — Isu Petasys offers a rare combination of growth, profitability, and income that is difficult to find elsewhere in the global technology supply chain. The key question is not whether the company is well-positioned today, but whether today’s price already reflects tomorrow’s opportunity.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or an endorsement to buy or sell any securities. All data referenced is based on publicly available information as of April 30, 2026. Investing in foreign equities involves risks including currency fluctuation, political and economic instability, and differences in accounting standards. Always conduct your own due diligence and consult with a qualified financial advisor before making investment decisions.