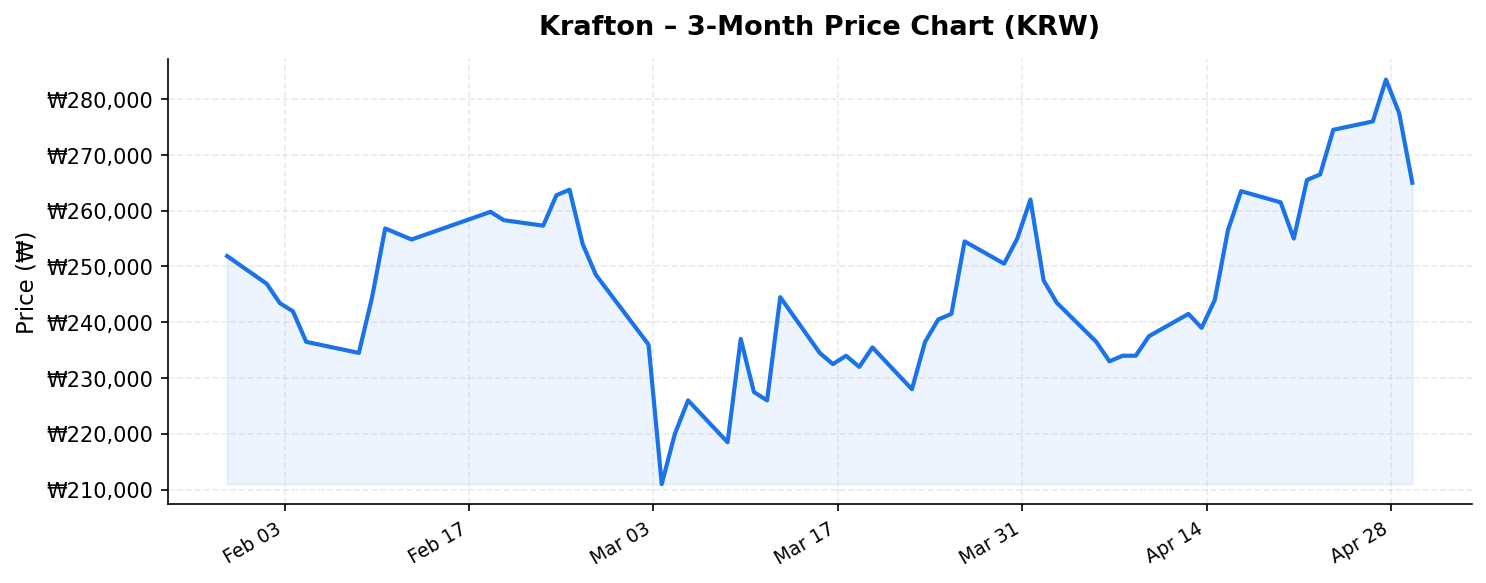

Krafton (크래프톤, 259960.KS), the South Korean gaming powerhouse behind the global phenomenon PUBG: Battlegrounds, has seen its share price slide significantly from its 52-week highs. As of May 3, 2026, shares are trading at ₩265,000 — a steep 32.6% decline from the 52-week peak of ₩393,000. With a market capitalization of approximately ₩11.6 trillion (roughly $8.5 billion USD), trailing twelve-month revenue of ₩3.3 trillion, and an eye-catching dividend yield of 85.00% that demands closer scrutiny, Krafton presents a complex investment case for international investors. Is this pullback a value trap or a rare window of opportunity in one of Asia’s most prominent gaming companies?

Business Overview: More Than Just PUBG

Krafton was established in 2007 and rose to global prominence with the release of PlayerUnknown’s Battlegrounds (PUBG) in 2017, a title widely credited with popularizing the battle royale genre. The company went public on the Korea Exchange in August 2021 and has since worked aggressively to diversify its portfolio beyond its flagship franchise.

Today, Krafton operates through multiple studios and subsidiaries. Its core revenue streams include:

- PUBG: Battlegrounds — The PC and console version remains a steady cash generator with a loyal global player base, particularly in Southeast Asia, India, and the Middle East.

- PUBG Mobile (via licensing to Tencent) — While Krafton doesn’t directly operate the mobile version in most markets, royalty income from Tencent’s operation of PUBG Mobile contributes meaningfully to the top line.

- Battlegrounds Mobile India (BGMI) — Krafton’s self-published version of the game for the Indian market, one of the world’s largest mobile gaming populations.

- The Callisto Protocol, inZOI, and other new IPs — Krafton has invested heavily in new intellectual properties to reduce dependency on a single franchise. inZOI, a life simulation game often compared to The Sims, generated significant buzz and has become a meaningful contributor to the company’s revenue diversification strategy.

- Deep learning and AI initiatives — Krafton has allocated capital toward AI-driven content creation and virtual human technology, positioning itself at the intersection of gaming and emerging tech.

With TTM revenue of ₩3.3 trillion, Krafton is solidly among the top-tier Korean gaming companies by revenue, competing with peers like NCSoft and Netmarble, while trailing only the diversified conglomerate operations of Nexon.

Valuation and Financial Health: Parsing the Numbers

At ₩265,000 per share, Krafton trades at a price-to-sales ratio of approximately 3.5x based on its ₩3.3 trillion in trailing revenue and ₩11.6 trillion market cap. For a gaming company with global IP and strong cash generation, this multiple is relatively modest compared to Western peers like Electronic Arts or Take-Two Interactive, which have historically traded at 4-6x sales.

The return on equity of 10.5% signals a respectable but not exceptional level of profitability. This figure likely reflects the company’s significant reinvestment in new game development, acquisitions, and AI research — spending that suppresses near-term returns but could pay dividends (literally and figuratively) in the future. For context, leading global gaming companies typically report ROE in the 12-20% range, suggesting Krafton has room to improve capital efficiency as its newer titles mature.

Now, the elephant in the room: the reported dividend yield of 85.00%. This extraordinary figure almost certainly reflects a special or extraordinary dividend distribution rather than a sustainable recurring payout. Krafton has historically maintained a relatively conservative dividend policy, and a yield of this magnitude likely stems from a massive one-time capital return — possibly funded by accumulated cash reserves or a strategic decision to distribute proceeds from asset sales or licensing deals. International investors should treat this yield with extreme caution and investigate whether this payout is recurring or a one-off event. A sustainable dividend yield in the low single digits would be more realistic for a growth-oriented gaming company of this profile.

Looking at the stock’s 52-week range of ₩208,500 to ₩393,000, the current price of ₩265,000 sits roughly 27% above the 52-week low and 32.6% below the high. This positions Krafton in the lower third of its annual trading range, which may appeal to value-oriented investors seeking entry points — provided the fundamental thesis remains intact.

Competitive Position and Growth Catalysts

Krafton’s competitive moat rests on several pillars that international investors should evaluate carefully:

- PUBG’s enduring franchise value: Despite being nearly a decade old, PUBG continues to generate consistent revenue through seasons, battle passes, and in-game purchases. The franchise’s cumulative sales and player count place it among the most commercially successful games in history.

- India market exposure: Through BGMI, Krafton has direct access to India’s rapidly growing mobile gaming market, projected to exceed $10 billion by 2027. Few Korean gaming companies have this level of direct engagement with Indian consumers.

- IP diversification with inZOI: The launch and ongoing development of inZOI represents Krafton’s most ambitious attempt to build a second franchise-scale IP. Early player reception and sales figures have been promising, and the life simulation genre has demonstrated remarkable longevity through The Sims franchise.

- AI and technology investments: Krafton’s bets on AI-generated content, virtual humans, and deep learning could create entirely new revenue streams or significantly reduce content creation costs, giving the company a structural advantage over competitors.

- Strong balance sheet: Krafton has historically maintained a net cash position with minimal debt, giving it financial flexibility to pursue acquisitions, invest in R&D, and return capital to shareholders — as evidenced by the extraordinary dividend distribution.

The competitive landscape in global gaming is fierce, with Tencent, Sony, Microsoft, and numerous other players vying for consumer attention. However, Krafton’s focused approach — combining a proven flagship franchise with strategic bets on new IPs and emerging technology — gives it a differentiated position within the Korean gaming sector.

Key Risks for International Investors

No investment thesis is complete without a thorough consideration of risks. For Krafton, international investors should weigh the following:

- PUBG dependency: Despite diversification efforts, PUBG and its variants still account for a disproportionate share of revenue. Any significant decline in the franchise’s player base or monetization effectiveness would materially impact financial performance.

- Regulatory risk in key markets: India has previously banned PUBG Mobile, and while BGMI has been reinstated, the regulatory environment for gaming in India, China, and other Asian markets remains unpredictable. New regulations on gaming hours, loot boxes, or content restrictions could impair revenue.

- New IP execution risk: Game development is inherently unpredictable. Not every new title will succeed, and the capital invested in projects that underperform represents a real opportunity cost. The Callisto Protocol, for example, received mixed reviews and fell short of commercial expectations.

- Currency risk: International investors buying Korean won-denominated shares are exposed to KRW/USD (or KRW/EUR) exchange rate fluctuations, which can amplify or diminish returns independent of the stock’s performance.

- Dividend sustainability: The 85% dividend yield is almost certainly not repeatable on an annual basis. Investors buying at current levels in expectation of a similar payout next year may be severely disappointed. Understanding the nature of this distribution is critical before making an investment decision.

- Share price momentum: A 32.6% decline from the 52-week high can signal either a value opportunity or deteriorating fundamentals. Investors should determine whether the selloff has been driven by sector-wide de-rating, company-specific concerns, or broader market conditions in Korea.

Investment Thesis: A Calculated Bet on Korean Gaming’s Evolution

For international investors with a medium-to-long-term horizon, Krafton at ₩265,000 presents an intriguing risk-reward profile. The stock trades at a meaningful discount to both its 52-week high and its historical valuation multiples, while the underlying business continues to generate ₩3.3 trillion in annual revenue with a clean balance sheet and multiple growth vectors.

The bull case rests on successful diversification beyond PUBG — particularly through inZOI’s growth trajectory and the monetization of AI capabilities — combined with continued expansion in high-growth markets like India. If Krafton can demonstrate that its newer IPs are gaining commercial traction, the current valuation multiple could re-rate meaningfully upward.

The bear case centers on PUBG fatigue, failed new IP launches, and regulatory headwinds in key markets. The extraordinary dividend yield, while attention-grabbing, should not be the primary reason for investment, as it is almost certainly non-recurring.

For global investors seeking exposure to the Korean gaming sector with a company that has a proven global franchise and credible growth ambitions, Krafton deserves serious consideration at these levels — but thorough due diligence on the dividend structure and competitive dynamics is essential before committing capital.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any securities. All data referenced is based on publicly available market information as of May 3, 2026. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.