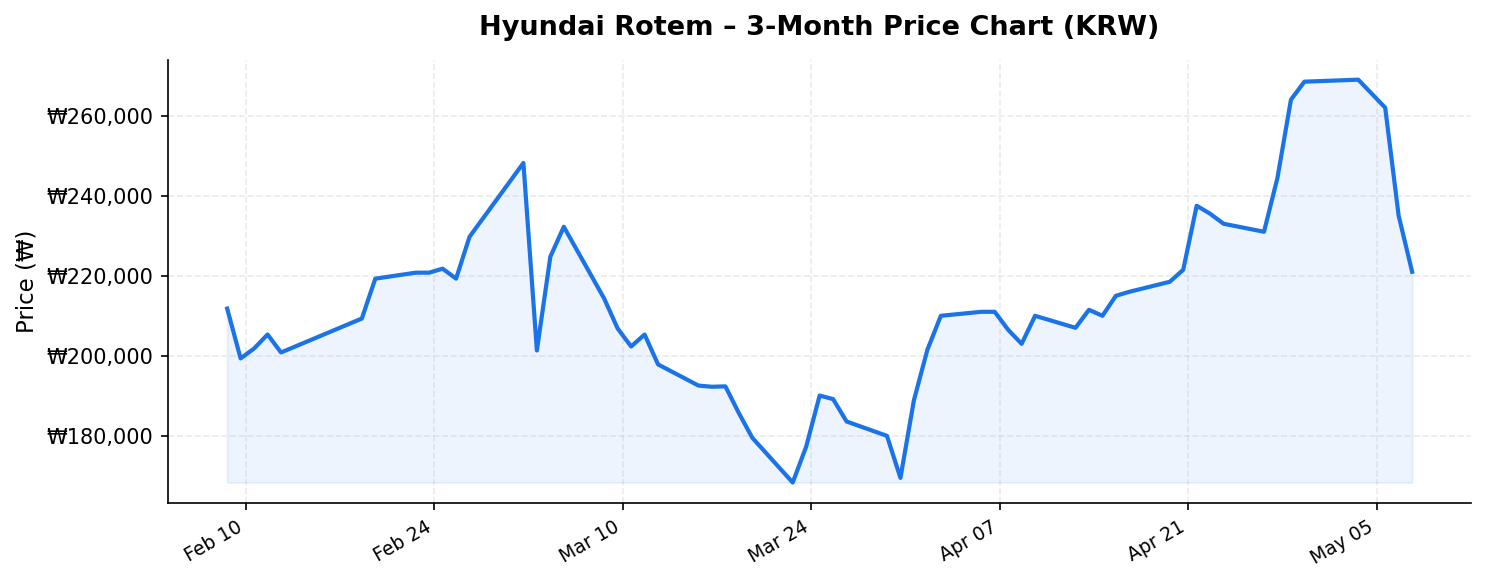

In the rapidly shifting landscape of global defense spending and infrastructure investment, few companies sit at the intersection of both megatrends quite like Hyundai Rotem (현대로템, 064350.KS). The South Korean manufacturer of tanks, rolling stock, and defense systems has undergone a remarkable transformation from a niche industrial player into one of the most closely watched defense-adjacent names on the Korea Exchange. Trading at ₩220,500 as of May 8, 2026, the stock sits roughly 22% below its 52-week high of ₩282,000 — a pullback that raises a compelling question for international investors: is this a buying opportunity, or a signal that the explosive growth narrative has run its course?

With a market capitalization of ₩24.1 trillion (approximately $17.5 billion USD), trailing twelve-month revenue of ₩6.1 trillion, and a return on equity of 30.6%, Hyundai Rotem’s financial profile demands serious attention. Add a headline-grabbing dividend yield of 26.00%, and the numbers tell a story that is both enticing and complex. Let’s unpack it.

Business Overview: Where Tanks Meet Trains

Hyundai Rotem operates across three core business segments: defense systems, rail solutions, and eco-friendly energy (primarily hydrogen fuel cell systems). The company is a subsidiary of the Hyundai Motor Group, one of the world’s largest industrial conglomerates, which provides both strategic backing and an extensive global distribution network.

On the defense side, Hyundai Rotem is the sole manufacturer of South Korea’s K2 Black Panther main battle tank — widely regarded as one of the most advanced tanks in the world. The K2 has become a critical export product, with Poland signing a landmark framework agreement for nearly 1,000 units in a deal valued at over $12 billion. This Polish contract, along with growing interest from NATO-aligned nations accelerating their rearmament programs, has been the primary catalyst behind the stock’s meteoric rise from around ₩25,000 in early 2023 to its 52-week high of ₩282,000.

On the rail side, the company manufactures high-speed trains (KTX), metro cars, and light rail vehicles. It has won contracts across the Middle East, Southeast Asia, and Europe. While this segment lacks the explosive growth narrative of defense, it provides steady, recurring revenue and diversification.

The hydrogen fuel cell segment remains nascent but strategically important. Hyundai Rotem produces hydrogen extraction systems and fuel cell power packs, aligning with South Korea’s national hydrogen economy roadmap. This positions the company for potential long-term upside as hydrogen infrastructure scales globally.

Financial Performance: Exceptional Profitability, But That Dividend Yield Needs Context

The numbers behind Hyundai Rotem are striking. Trailing twelve-month revenue of ₩6.1 trillion reflects the escalation in defense order fulfillment and rail project deliveries. More impressive is the return on equity of 30.6% — a figure that places the company in elite territory not just among Korean industrials, but globally among defense contractors. For comparison, major Western defense primes like Rheinmetall and BAE Systems typically generate ROE in the 15-25% range. Hyundai Rotem’s superior figure reflects both operational leverage from scaling production and a still relatively modest equity base that is being put to highly efficient use.

Now, let’s address the elephant in the room: the 26.00% dividend yield. At face value, this figure is extraordinarily high and warrants careful scrutiny. There are a few possible explanations international investors should consider:

- Special dividend: Hyundai Rotem may have issued a one-time or special dividend tied to the extraordinary cash flows generated by the Polish K2 contract and other defense orders. Special dividends inflate the trailing yield calculation but are not necessarily recurring.

- Capital return policy shift: The company or its parent, Hyundai Motor Group, may have adopted a more aggressive shareholder return policy — a broader trend across Korean conglomerates under pressure from the government’s “Corporate Value-Up” program launched in 2024.

- Sustainability question: A 26% yield on a ₩24.1 trillion market cap implies annual dividend payments of roughly ₩6.3 trillion — a figure that exceeds the company’s TTM revenue of ₩6.1 trillion. This strongly suggests the yield is based on a non-recurring special dividend rather than a sustainable payout. International investors should not underwrite this yield as repeatable without further confirmation from the company’s dividend policy disclosures.

Regardless of the dividend’s sustainability, the underlying profitability is real. The combination of high-margin defense contracts and improving rail economics has fundamentally altered Hyundai Rotem’s earnings power compared to just three years ago.

Competitive Position and Growth Catalysts: Riding the Global Rearmament Wave

Hyundai Rotem’s competitive moat rests on several pillars:

- Proven product excellence: The K2 Black Panther is combat-proven technology that competes favorably against Germany’s Leopard 2A7 and America’s M1A2 Abrams on both capability and cost. Korea’s defense products increasingly offer a “best value” proposition — advanced technology at price points 20-40% below Western equivalents.

- Geopolitical tailwinds: NATO’s expansion, Europe’s rearmament imperative following Russia’s invasion of Ukraine, and rising defense budgets across the Indo-Pacific create a multi-decade demand environment for exactly the products Hyundai Rotem manufactures. Poland’s commitment alone provides revenue visibility well into the 2030s.

- Production capacity expansion: The company has been aggressively investing in expanding its Changwon production facilities to meet surging demand. Capacity that was designed for peacetime production rates of 30-50 tanks per year is being scaled to potentially 100+ units annually.

- Rail infrastructure spending: Global rail investment continues to grow, driven by urbanization and decarbonization trends. Hyundai Rotem’s competitiveness in high-speed and urban rail gives it access to a $200+ billion global market.

The stock’s current price of ₩220,500, representing a 118% premium over its 52-week low of ₩101,000, reflects how dramatically the market has re-rated the company. Yet the 21.8% discount to the 52-week high suggests some investor caution — likely tied to concerns about execution risk on the massive Polish order, potential currency headwinds (the won-dollar exchange rate significantly impacts export profitability), and the broader question of whether defense spending momentum will sustain or plateau.

Key Risks: What Could Go Wrong

No investment thesis is complete without a clear-eyed assessment of risks. For Hyundai Rotem, international investors should weigh the following:

- Execution and production scaling risk: Ramping tank production from dozens to hundreds of units annually is an enormous industrial challenge. Supply chain bottlenecks, quality control issues, or delays could erode margins and damage the company’s reputation with export customers.

- Geopolitical risk (both ways): While current geopolitical tensions are a tailwind, any de-escalation — a ceasefire in Ukraine, for instance — could reduce the urgency of European rearmament and dampen order momentum. Conversely, escalation on the Korean peninsula would create operational risk for the company’s domestic facilities.

- Customer concentration: The Polish K2 contract represents a disproportionate share of the defense backlog. Any renegotiation, cancellation, or payment delay would have outsized impact on financial projections.

- Valuation re-rating risk: At a market cap of ₩24.1 trillion against ₩6.1 trillion in revenue, the stock trades at roughly 4x trailing revenue — a significant premium for an industrial manufacturer, reflecting high growth expectations. If growth disappoints, multiple compression could be severe.

- Currency and repatriation risk: International investors face won/dollar exchange rate exposure. Additionally, Korea’s withholding tax on dividends (typically 22% for foreign investors) reduces the effective yield.

- Chaebol governance concerns: As part of the Hyundai Motor Group, Hyundai Rotem is subject to the typical governance dynamics of Korean conglomerates, including potential related-party transactions and decisions that may not always prioritize minority shareholder interests.

Investment Thesis: A Compelling but Complex Opportunity

For international investors seeking exposure to the global defense spending upcycle with a differentiated Asian angle, Hyundai Rotem presents a genuinely compelling case. The company’s 30.6% ROE demonstrates that it is not merely riding a narrative — it is converting geopolitical demand into real, high-quality earnings. The 22% discount from the 52-week high offers a more attractive entry point than was available at the peak, while the stock’s position well above its 52-week low of ₩101,000 confirms that the structural re-rating is largely intact.

The astronomical 26% dividend yield should be treated with significant caution — it almost certainly reflects a special distribution rather than a sustainable payout. Investors should focus instead on the underlying earnings trajectory, the massive defense backlog providing multi-year revenue visibility, and the optionality offered by the hydrogen and rail businesses.

The key question is whether ₩220,500 adequately prices in both the upside potential and the execution risks. At approximately 4x trailing revenue with ROE above 30%, the valuation is demanding but defensible if the company can continue delivering on its defense contracts and expanding its export customer base. A resumption of momentum toward the ₩282,000 high — representing roughly 28% upside — is plausible if upcoming quarterly results confirm strong backlog conversion and margin sustainability.

For portfolio construction purposes, Hyundai Rotem is best viewed as a high-conviction thematic position within a broader international or defense-focused allocation, rather than a core holding. Position sizing should reflect the inherent volatility of a stock that has traded in a ₩101,000–₩282,000 range over the past year — a spread of nearly 180%.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice, a recommendation, or a solicitation to buy or sell any security. All data is sourced from publicly available market information as of May 8, 2026, and may be subject to change. Investors should conduct their own due diligence and consult with a qualified financial advisor before making investment decisions. Past performance is not indicative of future results.