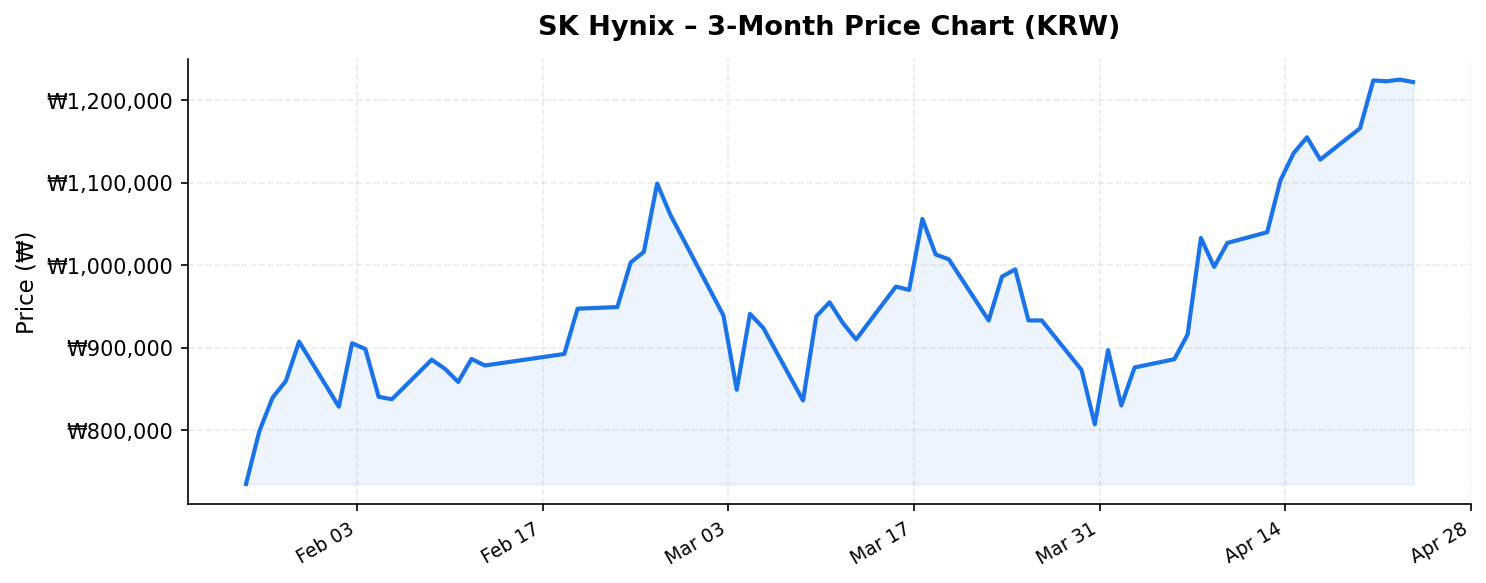

In the global semiconductor landscape, few stories have been as dramatic — or as rewarding for investors — as the meteoric rise of SK Hynix (SK하이닉스, 000660.KS). As of April 25, 2026, the company’s shares trade at ₩1,222,000, just 3.6% below their 52-week high of ₩1,267,000 and a staggering 591% above their 52-week low of ₩176,700. With a market capitalization of ₩866 trillion (approximately $640 billion USD), SK Hynix has firmly cemented itself as one of the most valuable companies in Asia and a cornerstone holding for any investor with exposure to the AI-driven semiconductor supercycle. But what’s perhaps most jaw-dropping is the company’s trailing dividend yield of 25%, a figure that demands careful analysis. Let’s break down whether SK Hynix at these levels still represents a compelling opportunity for international investors — or whether the best of the rally is already priced in.

Business Overview: The Indispensable Memory Powerhouse

SK Hynix is the world’s second-largest manufacturer of memory semiconductors, trailing only Samsung Electronics in DRAM market share and competing fiercely with Micron Technology for the number-two spot in NAND flash. The company is headquartered in Icheon, South Korea, and operates advanced fabrication facilities in South Korea and Dalian, China. Its product portfolio spans conventional DRAM, NAND flash storage, and — most critically for the current investment narrative — High Bandwidth Memory (HBM), the specialized DRAM used in AI accelerators like NVIDIA’s GPUs and AMD’s Instinct series.

It is HBM that has transformed SK Hynix from a cyclical commodity chipmaker into one of the most sought-after technology stocks on the planet. The company secured an early and dominant lead in HBM3 and HBM3E production, becoming the primary supplier to NVIDIA at a time when demand for AI training and inference hardware has been virtually insatiable. This first-mover advantage has translated directly into the financial results: trailing twelve-month (TTM) revenue stands at ₩132.1 trillion, a figure that would have seemed unimaginable just two years ago when the memory industry was mired in a deep cyclical downturn.

The company’s return on equity (ROE) of 61.2% underscores just how profitable this HBM-led cycle has been. For context, an ROE above 20% is generally considered excellent in the semiconductor industry. SK Hynix’s 61.2% figure reflects a combination of premium pricing on HBM products, high utilization rates across its fabs, and operating leverage that comes from selling high-value products at scale. This is a business firing on all cylinders.

Valuation and Dividend: Parsing the Extraordinary Numbers

Perhaps the single most striking data point for SK Hynix right now is its dividend yield of 25%. At first glance, this seems almost too good to be true — and international investors are right to approach it with a degree of caution. The yield reflects the company’s decision to distribute a significant portion of its extraordinary cyclical profits to shareholders. SK Hynix adopted a more shareholder-friendly capital return policy in recent years, committing to return a meaningful share of free cash flow via dividends and buybacks. Given the unprecedented profitability driven by HBM, the absolute dividend payments have been massive.

However, investors must understand that this yield is calculated on trailing dividends. Memory semiconductors remain a cyclical industry, and while the AI-driven demand cycle shows no signs of imminent collapse, the 25% yield should not be extrapolated indefinitely into the future. If HBM pricing normalizes or if competitors (particularly Samsung and Micron) close the technology gap, margins could compress, and dividend payments could adjust downward. That said, even a significant reduction from the current payout would still leave SK Hynix with an attractive yield relative to most global technology peers.

On a price-to-earnings basis, SK Hynix’s valuation looks surprisingly reasonable given its growth trajectory. With ₩132.1 trillion in TTM revenue and the implied net income behind that 61.2% ROE, the stock is trading at a forward P/E that many analysts estimate in the low-to-mid single digits — a fraction of what Western AI beneficiaries like NVIDIA command. The ₩866 trillion market cap is enormous in absolute terms, but relative to the cash generation machine this company has become, the valuation multiples tell a story of a stock that the market still treats with some cyclical skepticism.

The stock’s proximity to its 52-week high — just 3.6% below ₩1,267,000 — signals strong momentum and continued investor confidence. Yet the distance from the 52-week low of ₩176,700 is a sobering reminder of the volatility inherent in memory stocks. Investors who bought at or near the lows have enjoyed nearly a 7x return, but those entering at current levels are buying into a fundamentally different risk-reward equation.

Competitive Position and Growth Catalysts

SK Hynix’s competitive moat in HBM is the single most important factor supporting the current valuation. The company was first to mass-produce HBM3E chips and has been aggressively developing next-generation HBM4, which is expected to enter volume production in late 2026 or early 2027. NVIDIA, the undisputed leader in AI accelerators, has publicly validated SK Hynix as its preferred HBM partner, and this relationship provides significant revenue visibility.

Several growth catalysts remain on the horizon:

- HBM4 Ramp: The next generation of High Bandwidth Memory promises higher capacity and bandwidth, with SK Hynix expected to maintain its technology lead. Each successive generation commands premium pricing during the early production phase.

- Expansion of AI Infrastructure: Hyperscalers including Microsoft, Google, Amazon, and Meta continue to increase capital expenditure on AI data centers. Every new GPU cluster requires substantial HBM content, creating a structural demand tailwind for SK Hynix.

- Edge AI and On-Device AI: As AI workloads migrate from the cloud to devices — smartphones, PCs, automobiles — demand for advanced memory solutions increases across SK Hynix’s entire product portfolio, not just HBM.

- NAND Recovery: After years of oversupply and depressed pricing, the NAND flash market is also recovering, providing an additional earnings tailwind beyond the HBM story.

Samsung Electronics, the perennial rival, has been investing heavily to catch up in HBM, and Micron Technology has also made strides. However, as of early 2026, SK Hynix’s yield rates and technology roadmap continue to lead the industry. The competitive gap, while narrowing, remains meaningful — and in semiconductors, being 6-12 months ahead in production technology translates directly into pricing power and customer lock-in.

Key Risks for International Investors

Despite the compelling fundamentals, international investors should carefully weigh several risks before allocating capital to SK Hynix at current levels:

- Cyclicality: Memory semiconductors are among the most cyclical segments in technology. The current upcycle has been extraordinary, but all cycles eventually turn. A slowdown in AI spending or an overbuild of data center capacity could lead to significant pricing pressure on DRAM and HBM products.

- Geopolitical Risk: SK Hynix operates a major NAND fab in Dalian, China, making it vulnerable to escalating US-China technology tensions. Export controls, trade restrictions, or political instability on the Korean Peninsula could disrupt operations or market access.

- Currency Risk: International investors buying a KRX-listed stock are exposed to the Korean won. Significant won depreciation against the US dollar or euro could erode returns even if the share price remains stable.

- Dividend Sustainability: As discussed, the 25% dividend yield is based on peak-cycle earnings. Investors attracted primarily by the yield could be disappointed if payouts are reduced during a cyclical downturn.

- Concentration Risk: SK Hynix’s outsized reliance on NVIDIA and a handful of hyperscalers for HBM revenue means that any shift in these customers’ procurement strategies — or a technology pivot away from GPU-centric architectures — could have an outsized negative impact.

- Valuation Entry Point: With the stock up nearly 600% from its 52-week low and trading near all-time highs, the margin of safety is thin. Any negative earnings surprise or guidance reduction could trigger a sharp correction.

Investment Thesis: Where Does SK Hynix Go From Here?

For international investors, SK Hynix presents a fascinating case study in the tension between extraordinary current fundamentals and the inherent cyclicality of the memory business. The bull case is straightforward: AI infrastructure buildout is a multi-year megatrend, SK Hynix is the technology leader in the most critical component (HBM), the stock trades at modest multiples relative to its earnings power, and the 25% dividend yield provides substantial cash returns while you wait.

The bear case is equally clear: this is a cyclical stock at or near peak earnings, trading near its all-time high, in an industry with a long history of boom-bust dynamics. The dividend yield, while spectacular, may be unsustainable, and the stock’s 591% appreciation from its 52-week low suggests that much of the good news is already reflected in the price.

The most balanced view may be that SK Hynix remains a core holding for investors with a structural view on AI adoption, but position sizing and entry timing matter enormously. Dollar-cost averaging, rather than a large lump-sum investment at ₩1,222,000, could help manage the volatility risk that comes with the territory. For those already holding significant gains, trimming positions to lock in profits while maintaining exposure to the ongoing AI cycle is a prudent consideration.

With ₩132.1 trillion in TTM revenue, a 61.2% ROE, and a market cap that still implies reasonable earnings multiples, SK Hynix is not an overvalued momentum stock by traditional metrics. But it is a stock where investor expectations are sky-high, and where the penalty for disappointment could be severe. International investors should enter with open eyes, a long-term horizon, and a clear understanding of both the opportunity and the risks.

Disclaimer: This blog post is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy, sell, or hold any security. All data is based on publicly available information as of April 25, 2026, and may be subject to change. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.