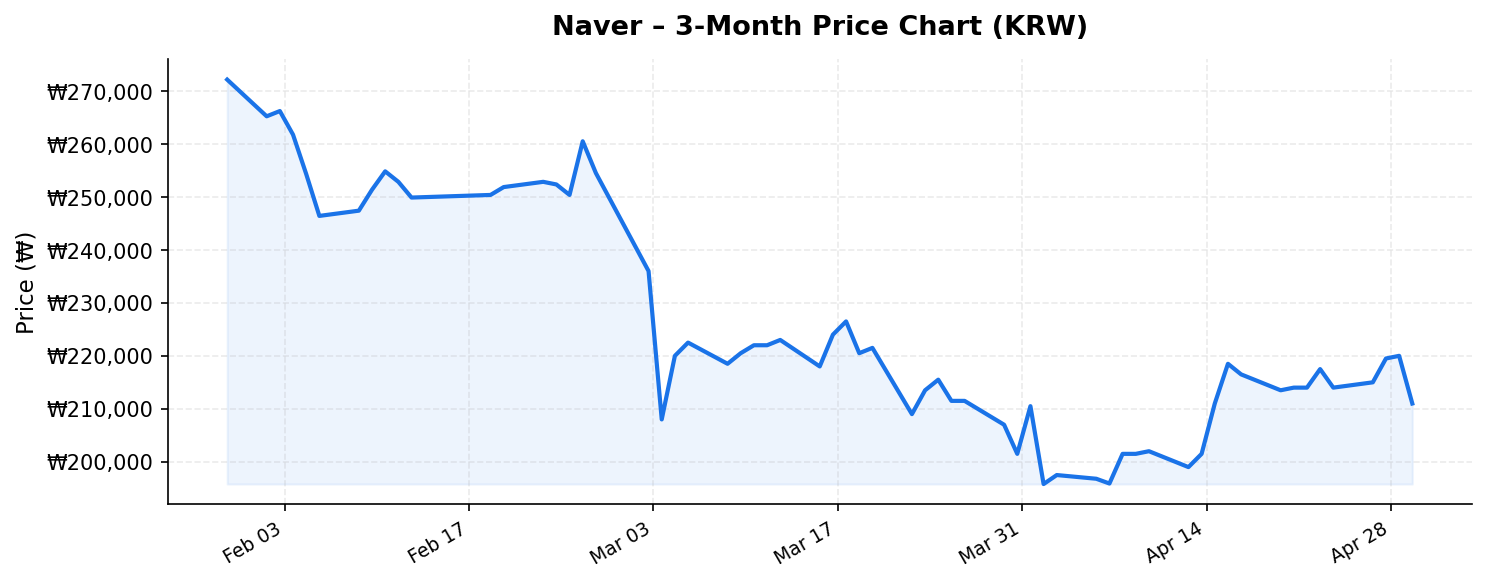

Naver (NAVER, 035420.KS), often described as the “Google of South Korea,” finds itself at a fascinating inflection point in May 2026. Trading at ₩211,000 — a steep 28.5% below its 52-week high of ₩295,000 — the company’s stock has undergone a significant correction even as its underlying business continues to generate over ₩12 trillion in trailing twelve-month revenue. For international investors looking at Korean equities, Naver presents a complex but potentially rewarding opportunity. With a market capitalization of ₩31.5 trillion (approximately $23 billion USD), a seemingly extraordinary dividend yield headline of 125%, and a modest return on equity of 6.5%, the numbers tell a story that requires careful unpacking. Let’s dive deep into what’s happening with South Korea’s most important internet company.

Business Overview: Far More Than a Search Engine

Naver is South Korea’s dominant internet platform, operating the country’s most-used search engine with a market share that consistently hovers above 55-60% for domestic web searches. But reducing Naver to a search company would be a fundamental misunderstanding of its business. The company has evolved into a sprawling digital ecosystem that touches nearly every facet of Korean online life — and increasingly, the lives of users across Asia.

The company’s revenue streams span multiple high-growth verticals. Its search and advertising platform remains the cash-generating core, but Naver has built significant businesses in e-commerce (Naver Shopping and the SmartStore platform, which supports hundreds of thousands of SME sellers), fintech (Naver Pay, which has become one of Korea’s most widely adopted digital payment solutions), content (Naver Webtoon, a global leader in digital comics with over 170 million monthly active users worldwide), and cloud computing (Naver Cloud, which serves as a key infrastructure provider in Korea and is expanding into sovereign cloud deals across Asia and the Middle East).

Additionally, Naver holds a significant equity stake in LINE Corporation, the dominant messaging app in Japan, Taiwan, and Thailand — giving it a strategic foothold in some of Asia’s most valuable digital markets. The company’s AI ambitions are also worth noting: Naver has invested heavily in its HyperCLOVA large language model series, positioning itself as one of the few non-American, non-Chinese companies with proprietary frontier AI capabilities.

With TTM revenue of ₩12.0 trillion (roughly $8.8 billion USD), Naver is not a small-cap speculation — it is a mature, diversified technology conglomerate with real revenues and real market positions.

Valuation and Market Data: What the Numbers Are Telling Us

The current share price of ₩211,000 places Naver at a price-to-sales ratio of approximately 2.6x based on its ₩12.0 trillion in TTM revenue and ₩31.5 trillion market cap. For a diversified tech platform company with dominant market positions, this is relatively modest — particularly when compared to global peers like Alphabet (which trades at roughly 5-7x sales) or even Japanese peer Z Holdings.

The stock’s position near the bottom of its 52-week range is striking. At ₩211,000, Naver sits just 16.5% above its 52-week low of ₩181,100, meaning the stock is much closer to its floor than its ceiling. This proximity to the low could indicate either a value trap or a buying opportunity — the distinction depends entirely on whether the factors that drove the decline are structural or cyclical.

The return on equity of 6.5% is arguably the most concerning metric in Naver’s data profile. For a technology company, this is low. It reflects the significant capital Naver has deployed into growth initiatives — cloud infrastructure buildouts, AI R&D, global expansion of Webtoon, and fintech investments — that have not yet generated proportional returns. International investors should watch this metric closely: if ROE begins trending upward over coming quarters, it would signal that Naver’s heavy investment cycle is beginning to bear fruit.

Now, about that 125% dividend yield. This figure almost certainly reflects a special or one-time extraordinary dividend — perhaps related to a corporate restructuring, asset sale, or return of capital event — rather than a sustainable recurring payout. A 125% yield on a ₩31.5 trillion company would imply an annual dividend payout of approximately ₩39 trillion, which would vastly exceed the company’s total revenue, let alone its profits. International investors should treat this number with extreme caution and investigate the specific nature of the distribution. It could represent a significant one-time capital return (which would be positive for shareholders) but should absolutely not be extrapolated as a recurring yield. Always check the ex-dividend date and the nature of the payout before making decisions based on this figure.

Competitive Position and Growth Catalysts

Naver’s competitive moat in South Korea remains formidable. The company benefits from deep network effects across its ecosystem: merchants use Naver Shopping because that’s where consumers search, consumers use Naver Search because that’s where the merchants are, and Naver Pay ties the entire transaction loop together. This integrated flywheel is extremely difficult for competitors — including Google, which has struggled to gain meaningful search market share in Korea — to replicate.

Several catalysts could drive Naver’s stock higher from current levels:

- AI Monetization: Naver’s HyperCLOVA AI models are being integrated across its search, shopping, and cloud platforms. AI-enhanced search advertising could significantly improve monetization rates, while AI-as-a-service offerings through Naver Cloud represent an entirely new revenue stream. Korea’s government has also been supportive of domestic AI development, creating potential tailwinds through public procurement.

- Webtoon Global Expansion: Naver Webtoon (which went public separately via Webtoon Entertainment on NASDAQ) continues to grow its global user base. Naver’s retained stake represents a significant source of embedded value that may not be fully reflected in the parent company’s stock price at current levels.

- E-commerce Market Share Gains: Naver Shopping has been steadily gaining ground against Coupang, particularly among small and medium-sized sellers who prefer Naver’s lower commission structure. As Korea’s e-commerce market continues to grow at high single-digit rates, Naver is well-positioned to capture a meaningful share.

- Cloud and Enterprise: Naver Cloud’s sovereign cloud partnerships — particularly in the Middle East and Southeast Asia, where governments are reluctant to rely solely on US-based hyperscalers — offer a differentiated growth path that few Korean companies can access.

Key Risks for International Investors

No investment thesis is complete without a rigorous assessment of risks, and Naver carries several that international investors should weigh carefully:

- Regulatory Pressure: Korean regulators have increased scrutiny of large platform companies. Naver has faced investigations related to search algorithm favoritism and competitive practices. New regulations could constrain the company’s ability to cross-leverage its ecosystem advantages.

- Currency Risk: For international investors, the KRW/USD exchange rate adds a layer of volatility. A weakening won would erode returns even if Naver’s stock price appreciates in local currency terms.

- Low ROE and Investment Returns: As noted, the 6.5% ROE suggests that Naver’s aggressive investment spending has not yet translated into superior returns on capital. If these investments fail to generate meaningful revenue growth or margin improvement, the stock could remain in value-trap territory.

- Competition from Global AI Giants: While Naver has built impressive AI capabilities, the sheer scale of investment by US-based companies (OpenAI, Google, Meta) and Chinese competitors (Baidu, ByteDance) means Naver could fall behind in the global AI race, potentially undermining its long-term competitive position even in its home market.

- LINE Corporation Complexity: Naver’s relationship with LINE (now integrated with SoftBank’s Yahoo Japan under LY Corporation) has become increasingly complex. Japanese regulatory scrutiny over data handling practices led to tensions, and any deterioration of this relationship could reduce the strategic value of Naver’s Japan exposure.

Conclusion: A Discounted Tech Champion Worth Watching

Naver at ₩211,000 is a company trading at a notable discount to its recent highs, with a diversified business model, dominant domestic market positions, and credible growth vectors in AI, cloud, and global content. The ₩31.5 trillion market cap and 2.6x price-to-sales ratio suggest the market is pricing in significant uncertainty — but also potentially offering a margin of safety for patient investors.

The apparent 125% dividend yield demands further investigation before being factored into any investment decision — it almost certainly reflects a non-recurring event rather than sustainable shareholder returns. The 6.5% ROE, while low, could improve meaningfully if Naver’s growth investments begin to scale. And the stock’s proximity to its 52-week low of ₩181,100, rather than its high of ₩295,000, means the risk/reward profile may be shifting in favor of buyers for those with a multi-year time horizon.

For international investors seeking exposure to South Korea’s digital economy through its most important internet company, Naver merits serious due diligence at these levels. The stock is not without risks — but the best opportunities rarely are.

Disclaimer: This blog post is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any securities. The market data referenced is as of May 2, 2026, and may have changed since publication. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. The author may or may not hold positions in the securities discussed.