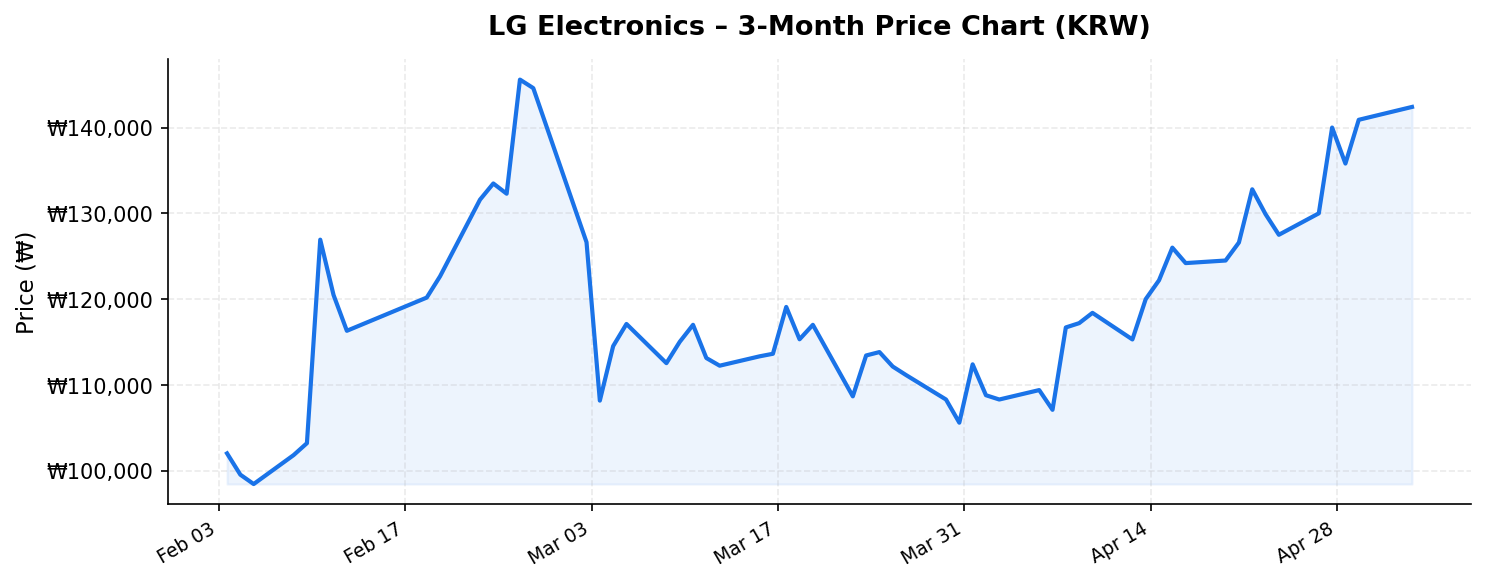

LG Electronics (LG전자, 066570.KS) has undergone one of the most remarkable transformations in the global consumer electronics and appliance industry over the past several years. Once known primarily for its smartphones — a business it exited in 2021 — the company has repositioned itself as a premium home appliance, vehicle components, and B2B solutions powerhouse. Trading at ₩142,500 as of May 4, 2026, with a market capitalization of ₩25.7 trillion (approximately $19 billion USD), LG Electronics sits just 6.2% below its 52-week high of ₩151,900 and has more than doubled from its 52-week low of ₩68,300. For international investors scanning the Korean market for value and income, LG Electronics demands serious attention — particularly given its eye-popping reported dividend yield of 96%. Let’s unpack what’s really going on.

Business Overview: A Post-Smartphone Renaissance

LG Electronics generates trailing twelve-month (TTM) revenue of approximately ₩90.2 trillion (roughly $66 billion USD), making it one of the largest consumer-facing companies listed on the Korea Exchange. The company operates through four primary business divisions:

- Home Appliance & Air Solution (H&A): The crown jewel of LG’s portfolio. This division encompasses refrigerators, washing machines, air conditioners, and air purifiers. LG consistently ranks as the world’s #1 or #2 home appliance brand globally, competing head-to-head with Whirlpool, Samsung Electronics, and Haier. The H&A division typically contributes over 35% of total revenue and an outsized share of operating profit, powered by premium product positioning and the strength of the LG brand in North America, Europe, and Southeast Asia.

- Home Entertainment (HE): LG remains a dominant force in the global television market, particularly in OLED technology where it benefits from the captive supply relationship with LG Display. The OLED TV segment commands premium pricing and strong margins relative to commodity LCD panels.

- Vehicle Component Solutions (VS): This rapidly growing division supplies infotainment systems, telematics, and electric vehicle (EV) powertrain components to global automakers. As the automotive industry accelerates its electrification and digitalization, the VS division has become LG’s most important long-term growth vector, with its order backlog repeatedly hitting record highs.

- Business Solutions (BS): Encompassing commercial displays, digital signage, robotics, and IT solutions, this division serves enterprise clients and is a quieter but steady contributor to the overall revenue mix.

The strategic exit from mobile phones in 2021 was initially met with skepticism, but it has proven to be a pivotal and prescient decision. By shedding a perennially loss-making business, LG freed up resources and management bandwidth to invest in higher-margin segments — a move that has clearly paid off given the stock’s powerful rally from its 52-week low of ₩68,300 to current levels near ₩142,500, representing a gain of over 108% from the trough.

Valuation, Dividends, and the 96% Yield Question

The most striking figure in LG Electronics’ current market data is the reported dividend yield of 96%. International investors should approach this number with important context. A yield this extreme almost certainly reflects a special or extraordinary dividend — likely a large one-time capital return event, possibly linked to asset restructuring, the monetization of cross-holdings, or a distribution of proceeds from a subsidiary transaction. Korean conglomerates (chaebols) have been under sustained pressure from both domestic regulators and activist investors to improve shareholder returns, and LG Group has been no exception.

If we take the reported yield at face value, it implies an annualized dividend of roughly ₩136,800 per share. For a company with a market cap of ₩25.7 trillion and approximately 180 million shares outstanding, that would represent a total payout of roughly ₩24.6 trillion — an extraordinary figure relative to the company’s typical annual net income of ₩2-3 trillion. This strongly suggests a non-recurring special dividend rather than a sustainable annual payout.

For income-focused international investors, the key question becomes: what is the normalized recurring dividend? LG Electronics has historically paid an ordinary dividend yielding between 1.5% and 3%, which is respectable by Korean standards and competitive with global peers. Any special dividend is certainly welcome as a bonus return of capital, but it should not be extrapolated as an ongoing income stream.

From a valuation perspective, at ₩142,500 per share with TTM revenue of ₩90.2 trillion, LG Electronics trades at a price-to-sales ratio of roughly 0.29x. This is remarkably low by global standards — Whirlpool, for instance, typically trades at 0.5-0.7x sales, and even Samsung Electronics commands a higher revenue multiple. LG’s low P/S ratio reflects the market’s traditional discount on Korean conglomerates due to complex cross-shareholding structures and perceived governance issues, but it also suggests meaningful upside if the company continues to execute and the “Korea discount” narrows.

Competitive Position and Growth Catalysts

LG Electronics occupies a differentiated competitive position across several dimensions:

- Premium appliance dominance: In North America — the world’s most profitable home appliance market — LG has built a formidable brand presence. Its market share in key categories like front-load washing machines and French-door refrigerators places it among the top two players. The premiumization trend in home appliances, where consumers trade up to smart, connected, and energy-efficient products, plays directly to LG’s strengths.

- OLED technology moat: The vertical integration with LG Display gives LG Electronics a structural advantage in OLED TVs. While competitors like Samsung Electronics have pivoted to QD-OLED and microLED, LG’s WOLED technology remains the standard-bearer in large-format OLED panels, and the company has expanded OLED into gaming monitors and commercial applications.

- Vehicle components inflection: The VS division has been the most exciting growth story. With global automakers investing hundreds of billions into EVs and software-defined vehicles, demand for LG’s infotainment platforms, advanced driver-assistance system (ADAS) components, and EV powertrain modules has surged. The division has reportedly secured an order backlog exceeding $70 billion, providing multi-year revenue visibility.

- Subscription and service revenue: LG has been building out recurring revenue models through its ThinQ smart home platform, extended warranty programs, and appliance rental services (particularly popular in Korea). These higher-margin, recurring revenue streams are beginning to move the needle on profitability.

The company’s proximity to its 52-week high — just 6.2% below ₩151,900 — reflects the market’s growing recognition of these catalysts. However, the gap also suggests there may still be room for further upside if key growth drivers continue to accelerate.

Key Risks for International Investors

Despite the compelling narrative, several risks warrant careful consideration:

- Currency risk: LG Electronics reports in Korean won, and international investors face KRW/USD (or KRW/EUR) exchange rate fluctuations. A strengthening won benefits returns for foreign holders, while depreciation erodes them. Given geopolitical volatility in Northeast Asia, currency risk is non-trivial.

- Korea discount and governance: Despite reforms, the Korean chaebol system still raises governance concerns for minority shareholders. Cross-shareholdings between LG Group affiliates, related-party transactions, and controlling family dynamics can dilute minority shareholder value. The extraordinary 96% dividend yield, while generous, could also signal complex corporate restructuring whose long-term implications are unclear.

- Vehicle components profitability: While the VS division’s revenue growth is impressive, it has historically operated at thin or negative operating margins. Scaling a hardware-intensive automotive supply business is capital-intensive, and any slowdown in EV adoption or pricing pressure from automakers could weigh on the division’s path to profitability.

- Macroeconomic sensitivity: Home appliances and consumer electronics are cyclical. A global recession or sustained weakness in the housing market — a key driver of appliance replacement demand — could pressure LG’s largest revenue segment.

- Competition from Chinese manufacturers: Haier, Midea, and other Chinese players are aggressively expanding internationally with competitive pricing. While LG’s premium positioning provides some insulation, the mid-range segment is increasingly contested.

Investment Thesis: Why International Investors Should Watch LG Electronics

LG Electronics presents a compelling case for international investors seeking exposure to multiple secular growth themes — premiumization of home living, automotive electrification, and the connected home — through a single, diversified platform trading at a discount valuation.

At a P/S ratio of just 0.29x on ₩90.2 trillion in TTM revenue, the stock appears undervalued relative to global peers. The stock’s surge from ₩68,300 to ₩142,500 over the past year demonstrates that the market is beginning to reprice the company’s improved fundamentals, but the persistent Korea discount suggests further re-rating potential. The extraordinary dividend payout, while likely non-recurring, underscores a management team and board that are increasingly committed to returning capital to shareholders — a positive governance signal.

The most attractive aspect of the LG Electronics thesis is optionality. If the vehicle components division achieves sustained profitability, it could drive a meaningful multiple expansion. If the Korea discount narrows — as has been a policy priority for Korean regulators through the “Corporate Value-Up” program — the stock could re-rate significantly. And if the premium appliance business continues to compound steadily, it provides a solid earnings floor.

For international investors with a medium- to long-term horizon, LG Electronics offers a rare combination of value, income, and growth optionality in the world’s fifth-largest equity market. The stock warrants a place on the watchlist — and potentially in the portfolio — of any globally diversified investor.

Disclaimer: This blog post is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any securities. Market data is as of May 4, 2026, and may have changed since publication. Investors should conduct their own due diligence and consult a qualified financial advisor before making any investment decisions. Investing in foreign securities involves additional risks including currency fluctuations, political risk, and differences in accounting standards.