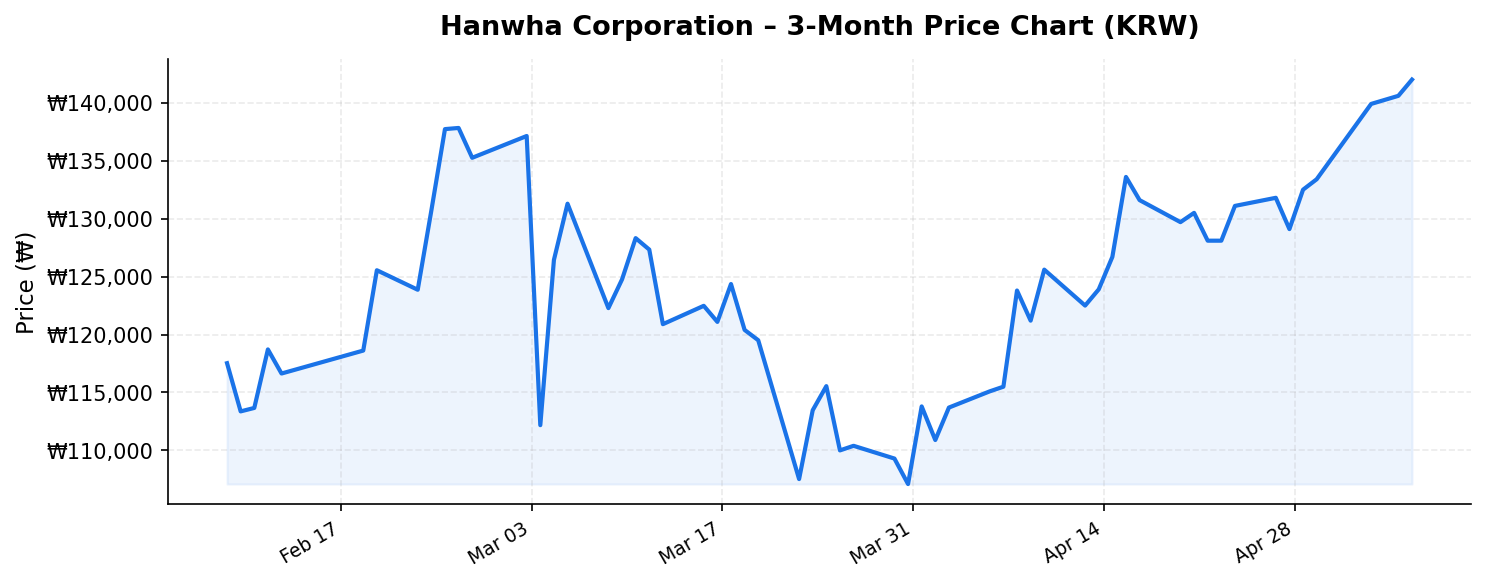

Hanwha Corporation (한화, 000880.KS), the holding company at the apex of one of South Korea’s most diversified conglomerates, has been on a remarkable run. As of May 7, 2026, the stock trades at ₩142,200 — just 5.1% below its 52-week high of ₩149,800, and a staggering 200% above its 52-week low of ₩47,450. With a market capitalization of approximately ₩12.7 trillion (roughly $9.3 billion USD), Hanwha Corporation sits at the intersection of several powerful global investment themes: defense spending, energy transition, and Korean industrial expansion. But with a reported dividend yield of 78% that demands closer scrutiny and a return on equity of just 4.5%, is this stock a compelling opportunity for international investors or a value trap wrapped in momentum? Let’s break it down.

Business Overview: More Than Just a Holding Company

Hanwha Corporation is the flagship holding entity of the Hanwha Group, one of South Korea’s top-ten chaebols (family-controlled conglomerates). Originally founded in 1952 as Korea Explosives, the company has evolved dramatically over seven decades. Today, its operations span three core pillars: defense and aerospace, energy and chemicals, and financial services — with tentacles extending into solar energy, construction, hospitality, and beyond.

The company’s direct operations include its Machinery and Defense divisions, which manufacture everything from ammunition and propellants to precision-guided munitions and rocket propulsion systems. Hanwha Corporation also serves as a strategic investor and management hub for its subsidiaries, most notably Hanwha Aerospace (the K9 self-propelled howitzer maker that has become a global defense export darling), Hanwha Solutions (a leader in solar photovoltaics through its Q CELLS brand), and Hanwha Ocean (formerly DSME, one of the world’s largest shipbuilders).

With trailing twelve-month (TTM) revenue of ₩74.8 trillion — a figure that reflects consolidated group revenue including major subsidiaries — Hanwha Corporation operates at an enormous scale. For context, that revenue figure translates to approximately $55 billion USD, placing it in the same league as major global industrial conglomerates. However, investors should note that much of this revenue flows through subsidiaries in which Hanwha Corporation holds partial stakes, meaning the holding company’s economic interest is a fraction of the consolidated top line.

The Explosive Rally: What’s Driving the Stock Price?

The numbers tell a dramatic story. Moving from a 52-week low of ₩47,450 to its current price of ₩142,200 represents roughly a threefold increase in under a year. Several converging catalysts explain this extraordinary performance.

Global Defense Spending Boom: The post-2022 geopolitical landscape — marked by the Russia-Ukraine conflict, rising tensions in the Taiwan Strait, and NATO members scrambling to meet defense spending commitments — has been a massive tailwind for Korean defense exporters. Hanwha Aerospace’s K9 howitzer, Chunmoo multiple rocket launcher, and Redback infantry fighting vehicle have secured landmark export contracts with Poland, Australia, Romania, and others. As the parent holding company, Hanwha Corporation benefits directly from the rising valuations and dividend flows of its defense subsidiaries.

Energy Transition Exposure: Through Hanwha Solutions’ Q CELLS division, Hanwha is one of the world’s largest solar cell and module manufacturers. With the U.S. Inflation Reduction Act incentivizing domestic solar manufacturing and Q CELLS building a major manufacturing complex in Georgia, the company is positioned to capture substantial value from the global clean energy buildout.

Shipbuilding Renaissance: Hanwha Ocean, acquired through the takeover of Daewoo Shipbuilding & Marine Engineering, is benefiting from a historic upcycle in global shipbuilding orders, particularly for LNG carriers and naval vessels. Order backlogs are at multi-year highs across the Korean shipbuilding industry.

Conglomerate Restructuring and Value Unlocking: Hanwha Group has been actively streamlining its corporate structure, spinning off and listing subsidiaries, and engaging in strategic acquisitions. These moves have helped narrow the traditional “holding company discount” that Korean conglomerates typically suffer in public markets.

Valuation, Dividends, and the 78% Yield Question

The most eye-catching data point in Hanwha Corporation’s profile is its reported dividend yield of 78%. International investors should approach this figure with significant caution. A yield this high almost certainly reflects a one-time special dividend or extraordinary distribution — possibly related to asset sales, subsidiary restructurings, or a return of capital event — rather than a sustainable recurring payout. At the current share price of ₩142,200 and market cap of ₩12.7 trillion, a genuine 78% annual yield would imply a dividend payment of approximately ₩110,916 per share, or nearly ₩10 trillion in total distributions. This would be financially unsustainable for any industrial conglomerate.

Investors should verify the nature of this distribution before making any investment decisions based on yield alone. If it reflects a special dividend tied to a one-off event — such as the proceeds from a major subsidiary IPO or asset disposition — the forward-looking yield would be materially lower. Historically, Hanwha Corporation’s regular dividend yield has been in the 1-3% range, consistent with other Korean holding companies.

On valuation, the return on equity of 4.5% is relatively modest, reflecting both the capital-intensive nature of Hanwha’s underlying businesses and the typical dilution effect of a holding company structure. International investors should compare this to the company’s cost of equity, which for a Korean industrial conglomerate likely sits in the 8-12% range. An ROE below the cost of equity suggests the company is not yet creating economic value on a per-share basis, though the trajectory of earnings improvement from defense and energy subsidiaries could change this calculus.

At a market cap of ₩12.7 trillion relative to ₩74.8 trillion in consolidated revenue, the price-to-sales ratio appears remarkably low at approximately 0.17x. However, this is somewhat misleading due to the holding company structure — Hanwha Corporation’s proportional claim on subsidiary earnings is significantly less than the consolidated revenue figure suggests. A sum-of-the-parts (SOTP) analysis valuing each subsidiary stake independently is the more appropriate valuation methodology for this type of investment.

Key Risks for International Investors

Despite the compelling thematic tailwinds, international investors should carefully weigh several material risks:

- Holding Company Discount: Korean holding companies historically trade at significant discounts to the sum of their subsidiary values. While governance reforms and Korea’s “Corporate Value-Up” program are working to narrow this gap, the discount can widen sharply during market downturns or periods of governance concern.

- Currency Risk: The stock is denominated in Korean won. For USD, EUR, or GBP-based investors, fluctuations in the KRW exchange rate can meaningfully impact total returns. The won has exhibited significant volatility in recent years amid shifting interest rate differentials and geopolitical tensions.

- Geopolitical Concentration: While Hanwha benefits from global security concerns, it is also exposed to them. Any escalation on the Korean Peninsula could paradoxically harm the stock despite boosting demand for defense products, as investors flee Korean assets broadly during security crises.

- Governance and Chaebol Risk: Hanwha Group, like other Korean conglomerates, has faced scrutiny over governance practices, related-party transactions, and controlling family dynamics. The chairman, Kim Seung-youn, has a controversial personal history that periodically resurfaces as a governance concern.

- Mean Reversion Risk: After a nearly 200% rally from its 52-week low, the stock is priced for continued execution on multiple fronts. Any disappointment in defense export orders, solar manufacturing margins, or shipbuilding profitability could trigger a sharp correction.

- Sustainability of Dividend: As discussed, the 78% yield figure almost certainly overstates the go-forward income potential of this stock. Income-focused investors may be disappointed by the normalized payout.

Investment Thesis: A Compelling but Complex Opportunity

For international investors seeking exposure to the global defense spending upcycle, the energy transition, and Korean industrial resurgence, Hanwha Corporation offers a unique one-stop vehicle. The stock’s position near its 52-week high — at ₩142,200 versus the ₩149,800 peak — suggests the market is pricing in strong momentum, but the proximity to the ceiling also means the easy gains may have already been captured.

The bull case rests on continued defense export momentum, successful execution of Q CELLS’ U.S. manufacturing expansion, a prolonged shipbuilding upcycle, and further narrowing of the holding company discount as Korean capital market reforms take hold. If Hanwha’s subsidiaries continue to win landmark international contracts and improve profitability, the holding company’s ROE should climb from its current 4.5%, potentially driving further re-rating.

The bear case centers on the stock’s stretched valuation relative to its historical range, the misleading nature of the headline dividend yield, governance risks inherent in the chaebol structure, and the possibility that the defense and energy cycles are closer to their peaks than their beginnings.

For international investors, the most prudent approach may be to consider Hanwha Corporation as a portfolio diversifier rather than a core holding — one that offers thematic exposure to powerful global trends through a Korean lens. Position sizing should reflect the elevated volatility, currency risk, and structural complexity inherent in investing in a Korean holding company. Those who prefer a more direct and transparent exposure might also consider the listed subsidiaries — Hanwha Aerospace, Hanwha Solutions, or Hanwha Ocean — individually, though this approach sacrifices the diversification benefit of the parent company structure.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy or sell any securities. The data presented reflects market information as of May 7, 2026, and may not be current at the time of reading. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. Investing in foreign securities involves additional risks including currency fluctuation, political instability, and differing accounting standards.