In an era of escalating geopolitical tensions across the Indo-Pacific, rising global defense budgets, and a paradigm shift in how nations approach security, South Korea’s defense sector has emerged as one of the most compelling investment themes in Asian equities. At the center of this transformation stands LIG Nex1 (LIG넥스원, 079550.KS), the country’s premier guided weapons and defense electronics manufacturer. With a current share price of ₩840,000, a market capitalization of ₩18.4 trillion, and a headline dividend yield of 35%, LIG Nex1 demands the attention — and scrutiny — of every international investor looking at the Korean defense boom.

But behind the eye-popping numbers lies a nuanced story. Is LIG Nex1 a generational opportunity, or are there hidden complexities that foreign investors need to understand? Let’s break down the data, the business, and the investment thesis.

Business Overview: South Korea’s Precision Strike Powerhouse

LIG Nex1 is South Korea’s leading manufacturer of precision-guided munitions, missile defense systems, electronic warfare equipment, and command-and-control systems. Originally spun off from LG Group’s defense division, the company has evolved into a critical pillar of the Republic of Korea’s indigenous defense capabilities. Its product portfolio spans surface-to-air missiles (including contributions to the KM-SAM Cheongung system), anti-ship missiles, tactical communication systems, radar technologies, and unmanned platforms.

The company operates at the intersection of two powerful secular trends: South Korea’s aggressive push toward defense self-sufficiency and the global arms export boom driven by conflicts in Ukraine, the Middle East, and heightened tensions in the Taiwan Strait. South Korea’s defense exports have surged in recent years, with landmark deals in Poland, Saudi Arabia, the UAE, and across Southeast Asia. LIG Nex1, as the country’s primary guided weapons integrator, is a direct beneficiary of these export contracts.

With trailing twelve-month (TTM) revenue of ₩4.3 trillion, LIG Nex1 has scaled significantly from its historical revenue base, reflecting both domestic procurement growth and an expanding export order backlog. The company’s return on equity of 17.3% signals strong profitability and efficient capital deployment — a notable achievement in a defense sector often characterized by thin margins and long contract cycles.

Valuation and the Extraordinary Dividend Yield: Unpacking the Numbers

The single most striking data point for LIG Nex1 is its reported dividend yield of 35%. For context, this would place it among the highest-yielding stocks not just in Korea, but globally. International investors should approach this figure with both excitement and caution.

A 35% dividend yield at a share price of ₩840,000 implies an annual dividend per share in the vicinity of ₩294,000. There are several scenarios that could explain this extraordinary payout. The most likely explanation is a special dividend — potentially a large one-time capital return tied to asset sales, a restructuring within the broader LIG Group, or a distribution of accumulated retained earnings. Korean conglomerates have increasingly adopted shareholder-friendly capital return policies under pressure from activist investors and regulatory reforms promoting corporate governance. If LIG Nex1 announced a substantial special dividend in recent quarters, this would explain the anomaly.

Investors must determine whether this yield is sustainable or one-off. A recurring 35% yield would be virtually unprecedented for a defense contractor and would imply a payout ratio that could undermine future R&D investment and growth. If it’s a special dividend, then the forward yield will normalize to a much lower figure — likely in the 1-3% range typical of Korean defense names. The distinction is critical for anyone building a position based on income expectations.

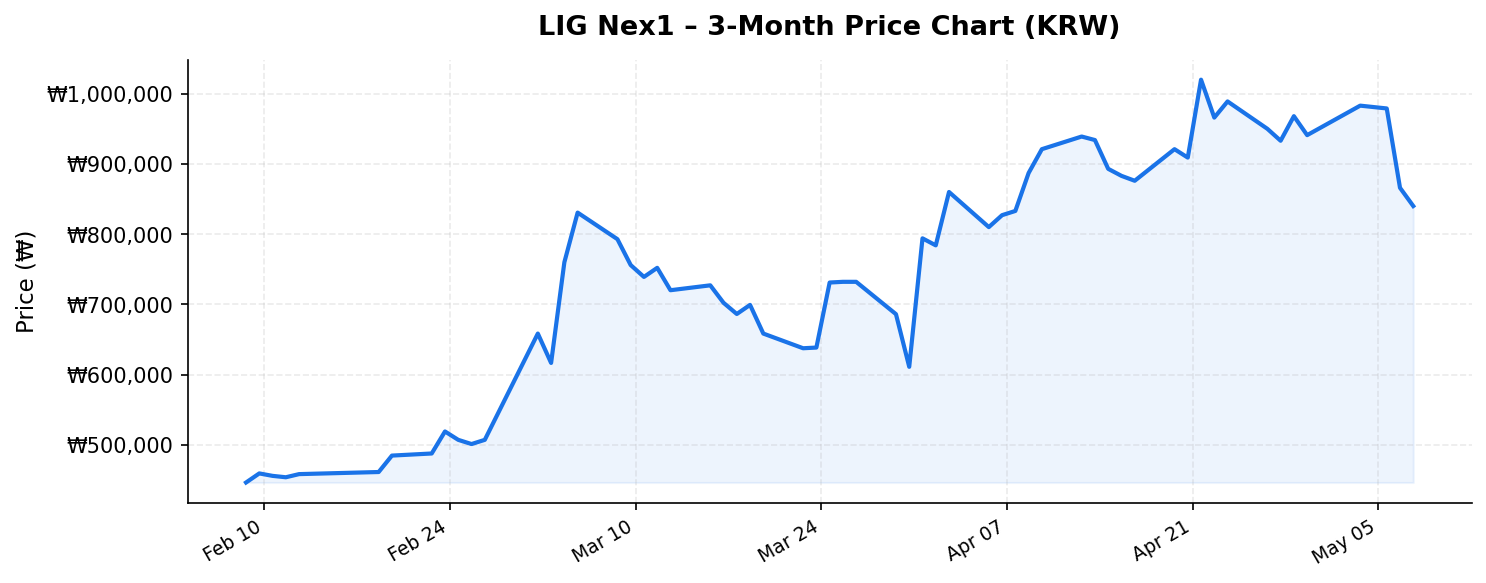

From a price perspective, LIG Nex1 currently trades at ₩840,000, which is 24.9% below its 52-week high of ₩1,118,000 but more than 134% above its 52-week low of ₩358,500. This wide 52-week range — from ₩358,500 to ₩1,118,000 — tells the story of a stock that has experienced tremendous momentum followed by a meaningful correction. The current price sitting roughly in the upper-middle of this range suggests the market has priced in substantial growth but has pulled back from peak euphoria. At a market cap of ₩18.4 trillion (approximately $13-14 billion USD), LIG Nex1 trades at roughly 4.3x TTM revenue — a premium valuation for a defense company, but one that can be justified if the export-driven growth trajectory continues.

Competitive Position and Growth Catalysts

LIG Nex1’s competitive moat rests on several pillars:

- Domestic monopoly in guided munitions: As Korea’s primary guided weapons manufacturer, LIG Nex1 benefits from a near-captive domestic customer in the Republic of Korea Armed Forces. Long development cycles and security clearance requirements create enormous barriers to entry for competitors.

- Export momentum: South Korea’s K-Defense brand has gained remarkable international traction. LIG Nex1’s missile systems, integrated with platforms from Hanwha Aerospace and Korea Aerospace Industries (KAI), form part of comprehensive package deals that have proven competitive against Western and Israeli alternatives on both price and performance.

- Technological advancement: The company is investing heavily in next-generation capabilities including hypersonic missile technology, AI-enabled autonomous systems, and advanced electronic warfare platforms. These investments position LIG Nex1 for the next cycle of defense modernization both domestically and internationally.

- Government backing: South Korea’s defense budget continues to grow at 5-7% annually, with the Yoon administration and its successors maintaining strong commitments to indigenous defense production and exports as a national strategic priority.

The ROE of 17.3% is particularly impressive when benchmarked against global defense peers. Lockheed Martin typically generates ROE in the 70-100%+ range (heavily leveraged balance sheet), while European peers like Rheinmetall and BAE Systems operate in the 15-25% range. LIG Nex1’s 17.3% ROE, achieved with what is typically a more conservative Korean balance sheet, suggests genuine operational efficiency and pricing power.

Key Risks for International Investors

Despite the compelling growth story, several risks warrant careful consideration:

- Dividend sustainability: As discussed, the 35% yield is almost certainly not recurring. Investors buying at current levels purely for income may be disappointed when the yield normalizes. Thorough due diligence on the dividend composition — ordinary vs. special — is essential.

- Valuation risk after a massive rally: The stock has more than doubled from its 52-week low. At 4.3x TTM revenue and ₩18.4 trillion market cap, any slowdown in order intake or export contract delays could trigger a sharp de-rating. Defense contracts are inherently lumpy, and quarter-to-quarter revenue volatility is common.

- Geopolitical and regulatory risk: Defense exports are subject to government approval and geopolitical considerations. A shift in diplomatic relationships — for instance, pressure from China on Korean arms sales to certain nations, or changes in U.S. technology transfer policies — could disrupt export pipelines.

- Currency risk: International investors face KRW/USD exposure. The Korean won’s volatility can meaningfully impact returns when converted to home currencies. A weakening won would erode dollar-denominated gains even if the stock price in KRW remains stable.

- Liquidity and access: While LIG Nex1 is listed on the KOSPI and accessible through most international brokerages offering Korean market access, it is not as liquid as mega-cap Korean names like Samsung or Hyundai. Bid-ask spreads may be wider, and large positions may be difficult to build or exit quickly.

- Concentration risk: Heavy reliance on Korean government procurement means any budget reprioritization or political shift could impact the domestic order pipeline significantly.

Investment Thesis: A Structural Growth Story with Near-Term Caution Warranted

For international investors, LIG Nex1 represents one of the purest plays on the global defense upcycle and South Korea’s emergence as a top-tier arms exporter. The fundamental story is strong: ₩4.3 trillion in TTM revenue, 17.3% ROE, a dominant domestic position, and a rapidly growing export backlog. The company sits at the technological frontier of guided weapons and defense electronics — capabilities that are in surging demand worldwide.

However, the entry point requires careful consideration. At ₩840,000, the stock has corrected nearly 25% from its 52-week high, which could represent either a buying opportunity or the early stages of a deeper pullback as momentum fades. The 35% dividend yield, while attention-grabbing, should not be the primary reason for investment unless confirmed as sustainable — and the overwhelming probability is that it reflects a non-recurring distribution.

The most prudent approach for international investors may be to build a position incrementally, using the pullback from the 52-week high as a starting point while keeping dry powder for potential further weakness. Investors with a 3-5 year time horizon who believe in the structural defense spending thesis — and who can tolerate the volatility inherent in Korean mid-cap defense names — will find LIG Nex1 to be one of the most strategically positioned companies in the global defense sector.

The bottom line: LIG Nex1 is not just a Korean story — it’s a global defense story with Korean characteristics. And at the right price, it could be one of the most rewarding defense investments available to international portfolios.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy or sell any securities. All data referenced is based on publicly available information as of May 9, 2026. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. Investing in foreign securities involves additional risks including currency fluctuations, political instability, and differences in accounting standards.