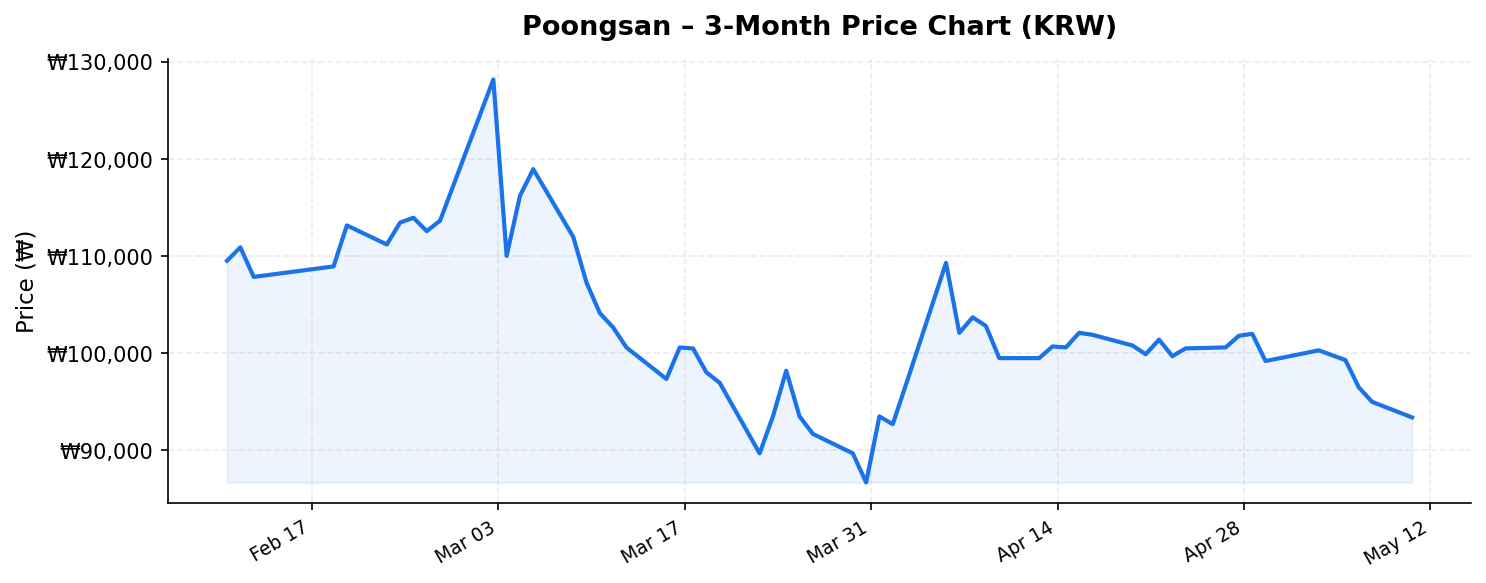

When a stock trades nearly 46% below its 52-week high while boasting what appears to be an extraordinary dividend yield and sitting at the intersection of two powerful global themes — defense spending and copper demand — international investors should take notice. Poongsan (풍산, 103140.KS), South Korea’s leading ammunition manufacturer and a major non-ferrous metals processor, finds itself in exactly this position as of May 11, 2026. With a current price of ₩93,400 and a market capitalization of approximately ₩2.6 trillion (roughly $1.9 billion USD), the company presents a complex investment case that warrants careful analysis.

Having surged to a 52-week high of ₩172,200 before retreating sharply, Poongsan now trades closer to its 52-week low of ₩57,000 than its peak. The question for international investors is straightforward: does this pullback represent a value opportunity, or is the market signaling fundamental concerns?

Business Overview: Where Defense Meets Industrial Metals

Poongsan occupies a distinctive niche in the Korean corporate landscape. Founded in 1968, the company operates across two major business segments that, while seemingly disparate, share deep metallurgical roots.

The defense division is Poongsan’s crown jewel. The company is South Korea’s sole domestic manufacturer of ammunition, producing everything from small-caliber rounds to large-caliber artillery shells, naval ammunition, and precision-guided munitions. This monopolistic position within South Korea’s defense procurement ecosystem gives Poongsan a durable competitive moat that few companies in any market can match. With geopolitical tensions remaining elevated globally — from the Korean Peninsula to Eastern Europe and beyond — demand for conventional ammunition has surged, and order backlogs across the global ammunition industry have stretched to multi-year timelines.

The copper and non-ferrous metals division processes copper into sheets, strips, tubes, and coins. Poongsan is one of the largest copper fabricators in Asia, supplying materials to electronics, automotive, construction, and even minting operations (the company produces South Korean coins). This segment is inherently more cyclical than defense, with profitability closely tied to copper prices and downstream industrial demand.

Trailing twelve-month revenue of ₩5.0 trillion (approximately $3.6 billion USD) reflects the combined scale of these two businesses. The revenue base provides meaningful diversification, though it also means that Poongsan’s financial performance is subject to both defense budget cycles and commodity price fluctuations.

Decoding the Numbers: Valuation, Dividend, and Profitability

The headline numbers for Poongsan require careful interpretation, particularly the reported dividend yield of 179%. This figure is almost certainly anomalous and likely reflects a special dividend distribution — potentially a return of capital, an extraordinary payout from asset sales, or a one-time distribution related to corporate restructuring. A sustainable 179% yield would imply the company is paying out nearly twice its entire market capitalization in dividends annually, which is economically impossible on a recurring basis. International investors should investigate the underlying dividend composition before making yield-driven investment decisions. Poongsan’s historical ordinary dividend yield has typically ranged between 2% and 4%, which remains respectable by Korean market standards.

The return on equity of 6.5% tells a more grounded story. While not exceptional, this ROE is consistent with a capital-intensive industrial manufacturer operating through a mixed commodity environment. For context, Korean industrial conglomerates frequently deliver ROEs in the 5-10% range during mid-cycle periods. However, 6.5% suggests Poongsan is not currently operating at peak profitability — which could mean either that margins are compressed by rising input costs or that the defense order ramp-up has not yet fully translated into bottom-line performance.

At a market cap of ₩2.6 trillion against ₩5.0 trillion in TTM revenue, Poongsan trades at a price-to-sales ratio of roughly 0.52x. This is remarkably cheap by global defense industry standards — major Western defense contractors like Rheinmetall, BAE Systems, and General Dynamics trade at 1.5x-3.0x sales. Even accounting for Poongsan’s lower-margin copper segment dragging down the blended multiple, this valuation gap is striking and suggests either a significant Korea discount or market skepticism about earnings sustainability.

Competitive Positioning and Growth Catalysts

Poongsan’s competitive advantages are multi-layered:

- Domestic monopoly in ammunition: As South Korea’s sole ammunition producer, Poongsan benefits from guaranteed procurement volumes and pricing power within the domestic defense budget. This is a structural advantage that cannot be easily replicated.

- Export growth potential: South Korea has emerged as a top-10 global arms exporter, with landmark deals in Poland, Australia, and the Middle East. While Poongsan is best known for ammunition rather than platforms like K2 tanks or K9 howitzers, every weapons system sold abroad creates derivative demand for ammunition supply contracts.

- Global ammunition shortage: The post-2022 geopolitical environment has exposed critical ammunition shortages across NATO and allied nations. Western production capacity remains insufficient to meet demand, creating a structural opening for Korean manufacturers to fill the gap. Poongsan has been actively expanding production capacity to capture this opportunity.

- Copper exposure as an asymmetric bet: With the global energy transition driving long-term copper demand (EVs, renewable energy infrastructure, grid modernization), Poongsan’s copper division provides indirect exposure to the electrification megatrend. If copper prices sustain elevated levels, this division could become a significant earnings contributor.

The stock’s decline from ₩172,200 to ₩93,400 — a 45.8% drawdown — likely reflects a combination of profit-taking after a defense-sector rally, potential copper price weakness, and broader Korean market softness. The current price of ₩93,400 sits approximately 64% above the 52-week low of ₩57,000, suggesting the market still assigns meaningful value to the business even after the correction.

Key Risks for International Investors

No investment case is complete without an honest assessment of risks, and Poongsan carries several that international investors must weigh:

- Commodity price sensitivity: Copper price declines directly impact the profitability and revenue of the metals division. Given that this segment accounts for a significant portion of total revenue, a sustained copper downturn could materially impair earnings even if defense orders remain robust.

- Geopolitical de-escalation risk: Paradoxically, peace can be a headwind for defense stocks. Any meaningful reduction in Korean Peninsula tensions or a resolution to major global conflicts could reduce defense procurement urgency and compress order backlogs.

- Korean corporate governance discount: Korean equities broadly trade at a discount to global peers — the so-called “Korea discount” — driven by concerns about chaebol governance, minority shareholder rights, and complex cross-shareholding structures. While Poongsan is not a chaebol in the Samsung or Hyundai mold, the family-controlled ownership structure may concern governance-focused investors.

- Currency risk: International investors are exposed to KRW/USD fluctuations. A weakening Korean won would reduce dollar-denominated returns, while a strengthening won would provide a tailwind.

- Dividend sustainability uncertainty: The 179% reported yield requires immediate clarification. If this reflects a non-recurring event, investors buying on yield alone could face significant disappointment in subsequent periods when dividends normalize.

- Capacity expansion execution risk: Poongsan is investing heavily in expanding ammunition production capacity. Delays, cost overruns, or shifts in government procurement timelines could impact returns on these investments.

Investment Thesis: Value Trap or Value Opportunity?

The bull case for Poongsan is compelling on paper. A monopoly defense manufacturer with growing export potential, trading at 0.52x sales and 45.8% below its 52-week high, in an industry experiencing secular demand growth — this profile checks many boxes for value-oriented investors. The copper division adds optionality tied to the electrification theme, and normalized dividends, while far below the reported 179%, should still offer reasonable income.

The bear case centers on cyclicality, governance concerns, and the possibility that the defense spending surge has already peaked. The 6.5% ROE suggests the business is not converting its revenue scale into exceptional shareholder returns, and international investors may find better risk-adjusted opportunities in Western defense contractors with stronger governance and more transparent capital allocation.

For international investors with a 2-3 year horizon and comfort with Korean market dynamics, Poongsan at ₩93,400 appears to offer an attractive risk-reward profile. The downside appears bounded by the asset-heavy balance sheet and monopoly position, while upside catalysts — continued defense export growth, copper price recovery, and potential re-rating toward global defense peers — could drive meaningful appreciation. Position sizing should reflect the commodity sensitivity and governance risks inherent in the name.

The most prudent approach may be to treat this as a value position with defense and commodity optionality, while conducting further due diligence on the extraordinary dividend figure and any related corporate actions that may explain it.

Disclaimer: This blog post is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or an offer to buy or sell securities. All data is based on publicly available information as of May 11, 2026, and may not reflect the most current developments. Investors should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions. Investing in foreign equities involves additional risks including currency fluctuation, political instability, and differing regulatory environments.