In an era of escalating geopolitical tensions, rising global defense budgets, and a rapidly shifting world order, few companies sit more squarely at the center of these trends than Lockheed Martin (LMT). As the world’s largest defense contractor by revenue, Lockheed Martin is a cornerstone holding for many institutional portfolios — and increasingly a point of interest for international investors seeking exposure to the U.S. defense industrial base.

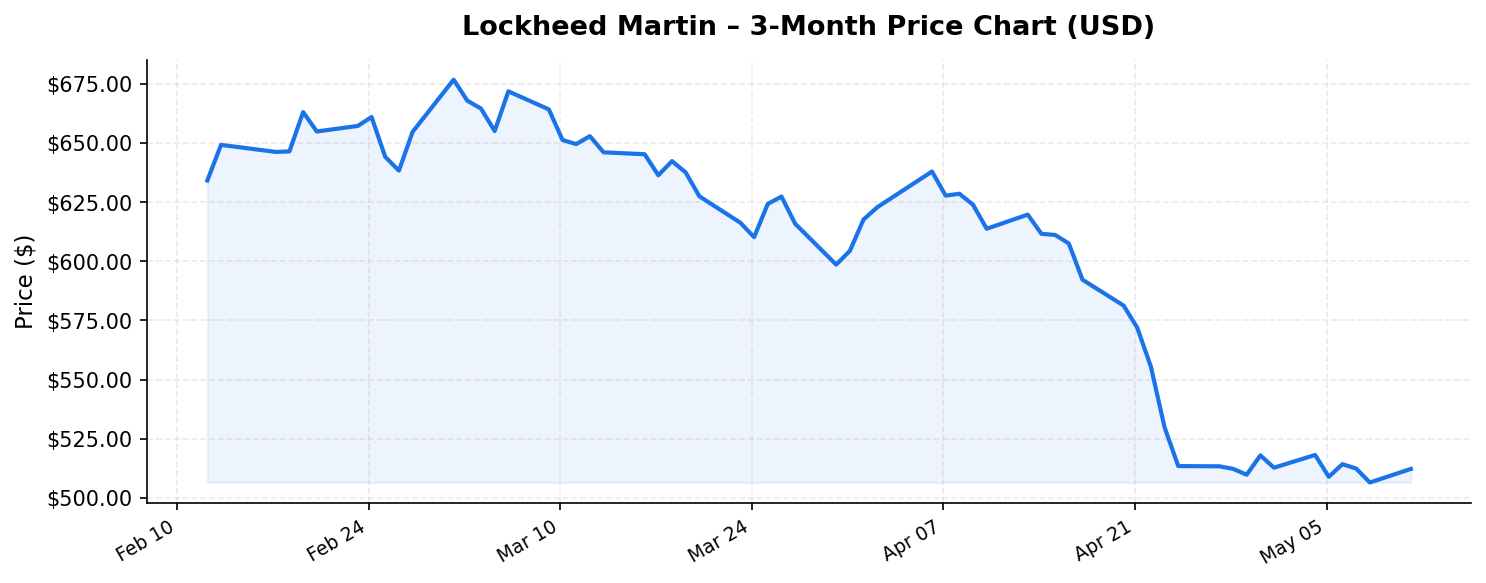

As of May 12, 2026, Lockheed Martin trades at $512.25 per share, representing a market capitalization of $118.1 billion. Notably, the stock sits approximately 26% below its 52-week high of $692.00, raising a critical question: does this pullback represent a compelling entry point, or are there structural headwinds that justify the discount? Let’s dig into the data.

Business Overview: A Defense Behemoth With Unmatched Scale

Lockheed Martin operates across four primary business segments: Aeronautics, Missiles and Fire Control, Rotary and Mission Systems, and Space. The company’s crown jewel remains the F-35 Lightning II Joint Strike Fighter program — the most expensive weapons system in history — which provides a multi-decade revenue stream through production, upgrades, and sustainment contracts with the U.S. Department of Defense and allied nations worldwide.

With trailing twelve-month (TTM) revenue of $75.1 billion, Lockheed Martin is not just the largest pure-play defense company in the world — it dwarfs many of its competitors. For context, its closest U.S. peers, RTX Corporation and Northrop Grumman, generate roughly $74 billion and $40 billion in annual revenue, respectively. This scale provides Lockheed Martin with significant advantages in program management, supply chain leverage, and the ability to invest in next-generation technologies like hypersonic weapons, directed energy systems, and advanced satellite constellations.

International sales represent a substantial and growing portion of Lockheed Martin’s revenue. NATO allies increasing their defense spending toward the 2% of GDP target — and in many cases well beyond it — directly benefits Lockheed Martin, as the F-35 program alone has customers in over 15 countries. For international investors, this means owning Lockheed Martin provides indirect exposure to a global rearmament cycle, not merely U.S. defense spending.

Valuation and Dividend: Parsing the Numbers

At a P/E ratio of 24.8x, Lockheed Martin trades at a modest premium to the broader S&P 500’s historical average but roughly in line with the defense sector’s recent valuation range. This is neither a deep value play nor an excessively priced growth stock — it reflects the market’s recognition of Lockheed Martin’s earnings stability and long-term contract visibility, tempered by concerns about margin pressures on fixed-price development programs and potential shifts in U.S. budget priorities.

The price-to-book ratio of 15.73x is eye-catching and may seem elevated at first glance. However, this metric requires context. Lockheed Martin’s capital-light business model — driven by intellectual property, engineering talent, and long-term government contracts rather than physical assets — naturally produces a high P/B ratio. More importantly, the company’s return on equity (ROE) stands at an exceptional 67.6%, which mathematically justifies a high book value multiple. An ROE of this magnitude signals that Lockheed Martin is extraordinarily efficient at generating profits from shareholders’ equity, a quality that income-focused and value-oriented investors alike should appreciate.

Perhaps the most striking data point is the reported dividend yield of 264%. This figure appears to be an anomaly — likely reflecting a special distribution, a capital return event, or a data reporting irregularity — and warrants careful verification by prospective investors. Lockheed Martin has historically maintained a dividend yield in the 2.5%–3.0% range, with a strong track record of consecutive annual increases spanning over two decades. If the company has indeed executed a massive special dividend or capital return program, it would represent a significant event for shareholders. International investors should consult their broker or Lockheed Martin’s investor relations page directly to confirm the current ordinary dividend rate and any tax withholding implications, as U.S. dividends paid to non-resident investors are typically subject to a 30% withholding tax (or a reduced rate under applicable tax treaties).

The stock’s current price of $512.25, sitting 26% below its 52-week high of $692.00 and roughly 25% above its 52-week low of $410.11, places it in a middle zone. The pullback from highs may reflect profit-taking after a strong run, broader market rotation out of defense names, or specific concerns around program execution. For patient investors, this level could represent a more attractive risk-reward entry point than chasing the stock near its peak.

Competitive Position and Growth Catalysts

Lockheed Martin’s competitive moat is among the widest in any industry. Defense contracting operates under extraordinarily high barriers to entry: security clearances, decades of institutional relationships with procurement agencies, proprietary technology, and the sheer complexity of managing multi-billion-dollar weapons programs create a near-impenetrable fortress around established primes. Switching costs for governments are enormous — once a country commits to the F-35 ecosystem, for example, it is effectively locked into Lockheed Martin for sustainment, upgrades, and training for 30+ years.

Several growth catalysts are worth highlighting for the medium to long term:

- Global rearmament cycle: NATO members, Japan, South Korea, Australia, and numerous other allies are dramatically increasing defense budgets. Lockheed Martin, as the primary supplier of advanced fighter aircraft, missile defense systems (THAAD, PAC-3), and space assets, is a prime beneficiary.

- F-35 production ramp and sustainment: With over 1,000 aircraft delivered and a total planned program of more than 3,000, the F-35 program is transitioning from peak production toward a lucrative long-term sustainment phase that should provide stable, high-margin revenue for decades.

- Next-generation programs: Lockheed Martin is competing for or leading several classified and unclassified programs, including next-generation interceptors, hypersonic strike weapons, and advanced satellite architectures under the Space Development Agency’s proliferated constellation.

- Nuclear modernization: The company’s role in the U.S. nuclear triad — through the Trident II submarine-launched ballistic missile and its involvement in the Sentinel ICBM program supply chain — provides exposure to one of the most politically durable spending categories in the U.S. budget.

No discussion of competitive position would be complete without acknowledging that Lockheed Martin faces real competition. Northrop Grumman secured the B-21 Raider next-generation bomber contract. Boeing and emerging players in the drone and autonomous systems space could challenge Lockheed Martin’s air dominance franchise over time. However, the depth and breadth of Lockheed Martin’s current program portfolio provides a diversified revenue base that few competitors can match.

Key Risks International Investors Should Monitor

Despite its formidable position, Lockheed Martin is not without risks, and international investors should weigh these carefully:

- U.S. budget and political risk: Approximately 70% of Lockheed Martin’s revenue comes from the U.S. government. Any significant shift in U.S. defense spending priorities — driven by fiscal austerity, political realignment, or a pivot away from traditional platforms — could materially impact the company’s top line.

- Fixed-price contract exposure: Several of Lockheed Martin’s development programs, including classified projects, operate under fixed-price contracts that can generate significant losses if costs overrun. The company has taken charges on such programs in recent years, and this remains an ongoing risk to margins.

- Supply chain constraints: The defense industrial base continues to face labor shortages, component availability issues, and subcontractor capacity limitations. These headwinds can delay deliveries and compress margins.

- Currency and geopolitical risk for international investors: Since Lockheed Martin reports and pays dividends in U.S. dollars, international investors bear currency translation risk. A strengthening home currency versus the dollar would reduce the value of both capital gains and dividend income. Additionally, export controls and shifting geopolitical alliances could affect international sales growth.

- Ethical and ESG considerations: Defense companies face increasing scrutiny from ESG-focused funds and certain sovereign wealth funds. Some international institutional investors may face mandates that restrict or limit defense stock holdings, which could constrain demand for shares over time.

Investment Thesis: A Durable Franchise at a Reasonable Price

For international investors seeking exposure to the global defense upcycle, Lockheed Martin offers a compelling combination of scale, profitability, and strategic relevance. The company’s $75.1 billion revenue base, exceptional 67.6% ROE, and decades-long program backlog provide a level of earnings visibility that is rare in any sector. Trading at 24.8x earnings and 26% below its 52-week high, the valuation appears reasonable for a business of this quality, though not deeply discounted.

The dividend story — historically a key attraction of Lockheed Martin stock — requires clarification given the reported 264% yield figure. If the company’s ordinary dividend remains in its historical range, it offers a solid and growing income stream, though international investors must account for U.S. withholding taxes and currency fluctuations.

The primary bull case rests on the durability and growth of global defense spending, Lockheed Martin’s irreplaceable position in critical allied defense architectures, and the long-term cash flow potential of its sustainment businesses. The bear case centers on political risk, margin pressure from fixed-price contracts, and the possibility that the current geopolitical premium fades.

On balance, Lockheed Martin remains one of the highest-quality franchises in the global defense industry. For international investors with a long-term horizon and a tolerance for the cyclical rhythms of government spending, the current pullback from highs may offer a reasonable opportunity to build or add to a position in this defense bellwether.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or an offer to buy or sell any securities. Market data referenced is as of May 12, 2026, and may have changed since publication. Investors should conduct their own due diligence and consult a qualified financial advisor before making any investment decisions. Tax treatment of U.S. dividends varies by jurisdiction; international investors should seek professional tax guidance.