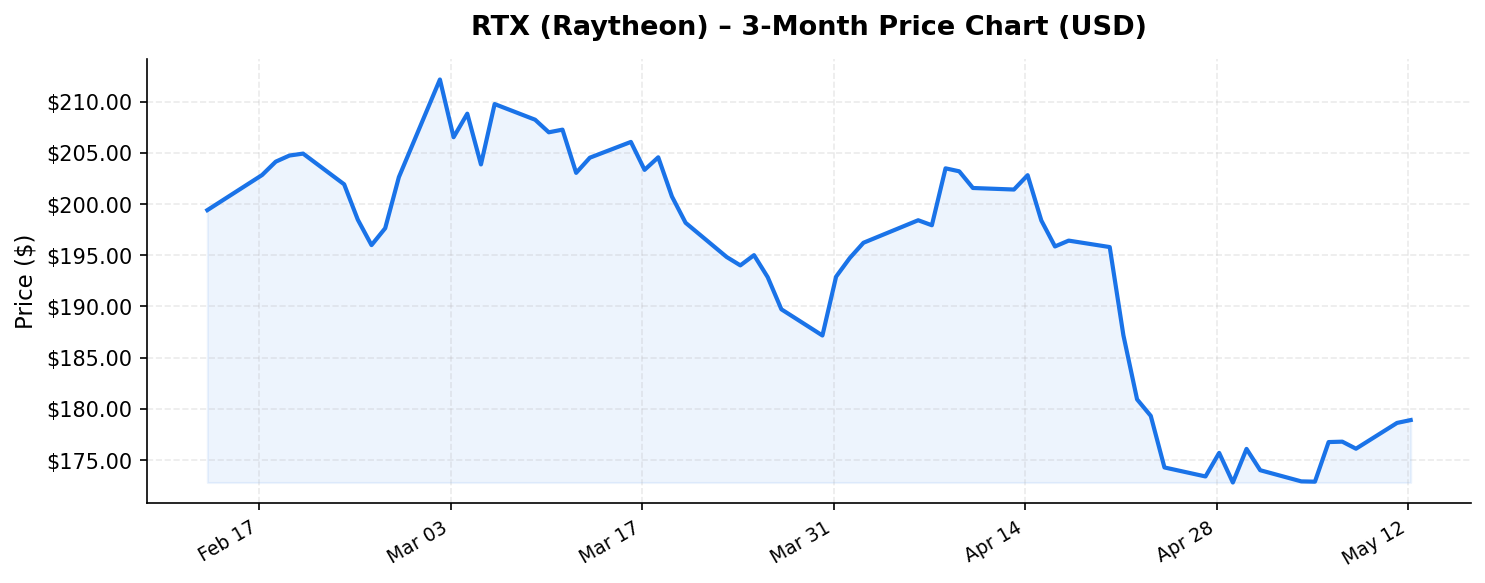

With geopolitical tensions simmering across multiple continents and global defense budgets surging to record levels, few companies are better positioned to capture this secular tailwind than RTX (Raytheon) (RTX) — the world’s largest aerospace and defense company by revenue. Trading at $178.89 as of May 13, 2026, the stock sits roughly 16.6% below its 52-week high of $214.50, raising a critical question for international investors: does this pullback represent a compelling entry point, or are there structural concerns that justify the discount?

In this analysis, we’ll dissect RTX (Raytheon)’s financial metrics, competitive moat, risk profile, and dividend story to help global investors make an informed decision about one of the most important defense stocks on the planet.

Business Overview: A $240 Billion Defense and Aerospace Powerhouse

RTX (Raytheon) is the product of the 2020 merger between Raytheon Company and United Technologies Corporation, creating a vertically integrated aerospace and defense conglomerate with unmatched scale. The company operates through three primary segments:

- Collins Aerospace: The world’s largest supplier of aerospace and defense systems, providing avionics, mechanical systems, interiors, and mission systems for both commercial and military platforms.

- Pratt & Whitney: A leading manufacturer of aircraft engines, powering everything from the F-35 Lightning II (via the F135 engine) to the fuel-efficient GTF engines found on the Airbus A320neo and A220 families.

- Raytheon: The missiles, defense, and intelligence segment that produces some of the most critical weapons systems in the Western arsenal — including Patriot air defense systems, Tomahawk cruise missiles, StingerMANPADS, and advanced radar systems.

With trailing twelve-month (TTM) revenue of $90.4 billion, RTX (Raytheon) commands a market capitalization of approximately $240.9 billion, placing it firmly among the largest defense contractors globally. This massive revenue base reflects both the defense spending boom and robust commercial aerospace recovery that have characterized the post-pandemic period.

Valuation Deep Dive: What Does a 33.6x P/E Really Mean?

At first glance, RTX (Raytheon)’s price-to-earnings ratio of 33.6x may seem elevated for a traditional defense contractor. Historically, large-cap defense stocks have traded in the 18-25x range, making this valuation a potential concern for value-oriented investors. However, context is essential.

Several factors help explain the premium valuation. First, RTX (Raytheon)’s earnings have been depressed by significant one-time charges related to the Pratt & Whitney powder metal contamination issue, which required costly fleet inspections and engine removals across the GTF fleet. As these charges roll off, normalized earnings should improve substantially, compressing the forward P/E into a more reasonable range. Second, the company’s massive backlog — which has grown to record levels driven by international Patriot system orders and GTF engine deliveries — provides exceptional earnings visibility for the next five to seven years.

The price-to-book ratio of 3.68x is broadly in line with aerospace and defense peers, reflecting the asset-heavy nature of the business combined with significant intangible value from proprietary technologies and long-term government contracts. Return on equity stands at 11.6%, which is respectable though not exceptional. Investors should expect this metric to improve as margin expansion from the high-margin Raytheon defense segment accelerates and Pratt & Whitney’s GTF aftermarket revenue begins to scale meaningfully.

Currently trading at $178.89, the stock is 38.6% above its 52-week low of $129.11, suggesting significant positive momentum over the past year despite the recent retreat from highs. For international investors considering entry, the current price represents a middle ground — not a deep-value bargain, but meaningfully cheaper than the recent peak of $214.50.

The Dividend Story: An Extraordinary 155% Yield Demands Scrutiny

Perhaps the most striking figure in RTX (Raytheon)’s current data is its reported dividend yield of 155%. This number warrants immediate and careful examination, as it almost certainly reflects a special dividend, extraordinary capital return event, or data anomaly rather than a sustainable ongoing yield.

For context, RTX (Raytheon) has historically paid a dividend yielding between 2% and 3%, with a strong track record of consistent increases. The company has been a reliable dividend payer for decades, making it a staple in income-focused portfolios. If the 155% yield reflects a one-time special distribution — perhaps related to a divestiture, asset sale, or capital restructuring — international investors should not extrapolate this forward as recurring income.

That said, even RTX (Raytheon)’s normalized dividend remains attractive for global investors, particularly those based in markets where defense sector exposure and USD-denominated income streams are scarce. International investors should be mindful of withholding tax implications: the United States typically withholds 30% on dividends paid to foreign investors, though this rate is often reduced to 15% under bilateral tax treaties with countries including the United Kingdom, Germany, Japan, Australia, and Canada. Checking your home country’s tax treaty with the U.S. is essential before investing for income.

Competitive Position and Key Risks for International Investors

RTX (Raytheon)’s competitive moat is arguably one of the widest in the industrial world. Defense contracting is characterized by enormous barriers to entry: decades-long development cycles, classified technology requirements, entrenched customer relationships with the U.S. Department of Defense and allied nations, and regulatory frameworks that effectively create oligopolistic market structures. In air defense alone, Patriot remains the gold standard for NATO and allied nations, with no Western competitor offering a comparable integrated system at scale.

The commercial aerospace side benefits similarly from Pratt & Whitney’s duopoly with CFM International (a GE Aerospace–Safran joint venture) in narrowbody aircraft engines. With the GTF engine powering the best-selling A320neo family, Pratt & Whitney has locked in decades of lucrative aftermarket revenue — a high-margin annuity stream that will grow as the installed fleet ages.

However, international investors should weigh several material risks:

- Geopolitical and regulatory risk: U.S. defense exports are subject to International Traffic in Arms Regulations (ITAR) and State Department approval. Changes in U.S. foreign policy could restrict sales to certain allied nations, directly impacting RTX (Raytheon)’s international revenue pipeline.

- Pratt & Whitney GTF issues: While the powder metal contamination problem is well-understood, the financial tail of inspections, compensations, and fleet disruptions may continue to weigh on earnings and cash flow in the near term.

- Budget and political risk: Although bipartisan support for defense spending is currently strong, any future shift toward fiscal austerity or defense budget cuts — particularly under political realignments — could impact top-line growth.

- Currency risk: For international investors, purchasing RTX (Raytheon) means taking on USD exposure. A weakening dollar would reduce returns when converted back to home currencies, while a strengthening dollar would enhance them. This cuts both ways and should be factored into portfolio allocation decisions.

- Valuation risk: At 33.6x earnings, any earnings disappointment or guidance reduction could trigger meaningful multiple compression, amplifying downside in the stock.

Investment Thesis: Why International Investors Should Pay Attention

For global investors seeking exposure to the U.S. defense sector — arguably the deepest and most technologically advanced in the world — RTX (Raytheon) represents the most diversified pure-play available. The combination of defense systems, commercial aerospace engines, and avionics creates a balanced revenue mix that provides resilience across economic cycles.

The secular growth drivers are powerful and durable. NATO nations are rapidly increasing defense spending toward the 2% of GDP target (with many now pushing toward 3%), and RTX (Raytheon) is a primary beneficiary through Patriot system sales, AMRAAM missiles, and advanced sensor technologies. Simultaneously, the commercial aerospace recovery continues to drive engine deliveries and aftermarket revenue at Pratt & Whitney and Collins Aerospace.

The current price of $178.89, sitting 16.6% below the 52-week high, offers a more attractive risk-reward entry point than was available just months ago. With TTM revenue of $90.4 billion and a backlog that extends years into the future, the revenue trajectory is well-supported. If normalized earnings recover as expected — driving the effective P/E into the mid-20s — there is meaningful upside potential from current levels.

For international investors building a diversified global portfolio, RTX (Raytheon) offers a rare combination: exposure to secular defense spending growth, a reliable (normalized) dividend stream in U.S. dollars, and a competitive position that is virtually unassailable in key product categories. The stock merits serious consideration as a core holding within an international investor’s U.S. allocation, with particular attention paid to entry timing and currency hedging strategies.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or an offer to buy or sell securities. All investors should conduct their own due diligence and consult with a qualified financial advisor before making investment decisions. Past performance is not indicative of future results. Market data referenced is as of May 13, 2026, and may have changed since publication.