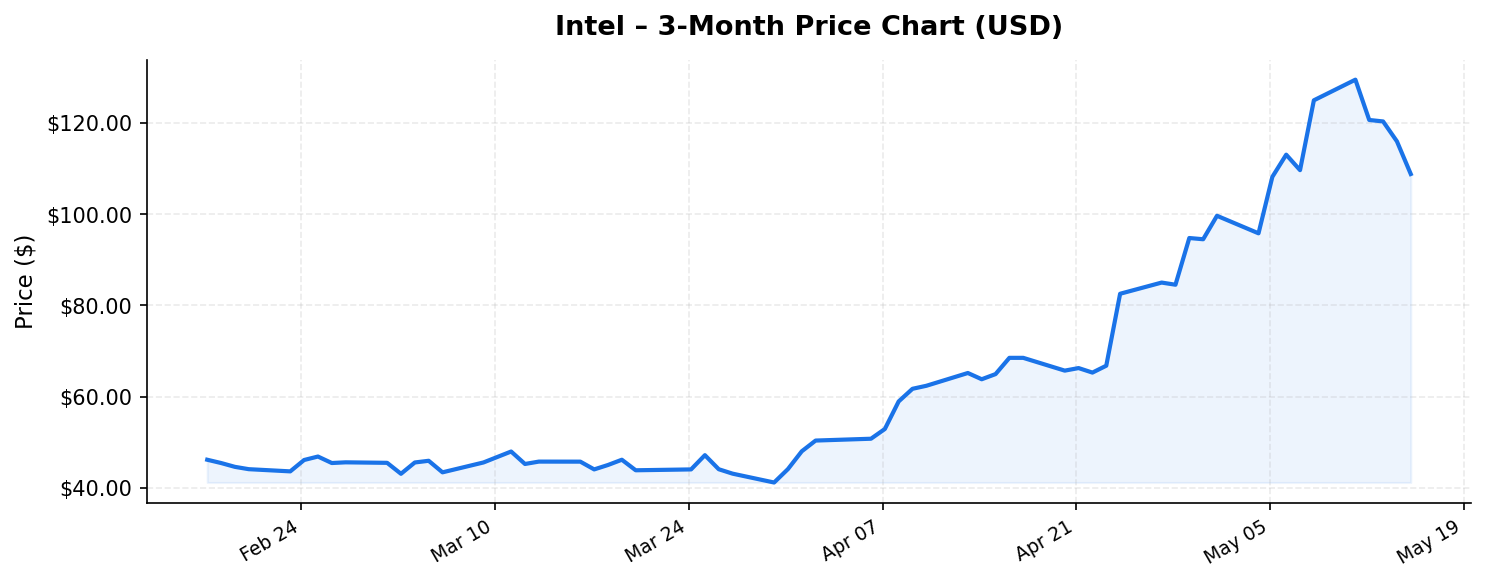

Few companies on Wall Street have staged a more dramatic turnaround than Intel (INTC). Just over a year ago, shares traded near historic lows under $19, as investors questioned whether the once-dominant chipmaker could survive the AI revolution it appeared to be missing. Fast forward to May 18, 2026, and Intel trades at $108.77 — a breathtaking surge of more than 470% from its 52-week low of $18.97. Yet with a market capitalization of $546.7 billion and a negative return on equity of -2.9%, international investors face a critical question: is Intel’s renaissance fully priced in, or is there more upside ahead?

This analysis unpacks Intel’s business transformation, its competitive positioning in the global semiconductor landscape, the key risks investors must weigh, and whether the stock offers a compelling opportunity for those investing from outside the United States.

The Intel Turnaround: From Crisis to $546 Billion

Intel’s story over the past two years reads like a corporate thriller. The company that once defined the semiconductor industry had fallen behind Taiwan Semiconductor Manufacturing Company (TSMC) in fabrication technology, lost market share to AMD in data center and PC processors, and watched NVIDIA capture virtually the entire AI accelerator market. By late 2024 and early 2025, Intel’s stock had cratered below $19, and serious questions arose about whether the company could remain independent.

What changed? Several catalysts converged to spark one of the most aggressive re-ratings in recent memory. Intel’s foundry business — Intel Foundry Services (IFS) — began securing meaningful external customers, validating CEO Pat Gelsinger’s successor leadership team’s aggressive IDM 2.0 strategy. The company’s 18A process node achieved production readiness ahead of revised timelines, and early yield data suggested competitive performance against TSMC’s N2 node. Crucially, significant U.S. government subsidies under the CHIPS and Science Act began flowing, with Intel receiving the largest allocation of any single company — over $15 billion in direct grants and loans.

The results are visible in Intel’s trailing twelve-month revenue of $53.8 billion, which reflects stabilization and early growth inflection across its product and foundry segments. However, the negative return on equity of -2.9% reveals an important truth: Intel is still not generating positive returns on shareholder capital. The massive capital expenditures required to build leading-edge fabs in Arizona, Ohio, and Germany are weighing heavily on profitability. Investors are buying a future earnings story, not current fundamentals.

Competitive Position: Foundry Ambitions Meet AI Reality

Intel’s competitive landscape is both its greatest opportunity and its most significant challenge. The company now operates across three major battlefronts: client and data center CPUs, AI accelerators, and contract chip manufacturing (foundry services).

CPUs: Intel has clawed back some market share from AMD in both PC and server processors with its latest architectures. The PC market has shown cyclical recovery, and Intel’s continued dominance in unit volume — if not always in performance benchmarks — provides a stable revenue foundation. However, the rise of ARM-based processors from Qualcomm and Apple in PCs, and AMD’s continued gains in data centers, mean this legacy stronghold faces persistent pressure.

AI Accelerators: Intel’s Gaudi line of AI training and inference chips has gained traction, particularly among cloud providers seeking alternatives to NVIDIA’s dominant but supply-constrained GPUs. While Intel remains a distant third behind NVIDIA and AMD in this category, even single-digit market share in a market projected to exceed $200 billion annually represents a meaningful revenue opportunity.

Foundry Services: This is the segment that has captured Wall Street’s imagination and arguably justifies much of the stock’s premium. Intel is the only Western company with leading-edge fabrication capabilities, positioning it as a strategic national asset for the United States and its allies. The geopolitical risk surrounding Taiwan — and by extension TSMC — has made Intel’s foundry ambitions a matter of national security. International investors should pay close attention to this dynamic: if geopolitical tensions in the Taiwan Strait escalate, Intel’s strategic value as an alternative manufacturer increases dramatically.

At a price-to-book ratio of 4.75x, the market is clearly assigning significant value to Intel’s tangible and intangible assets, including its fab infrastructure and intellectual property portfolio. For context, this P/B multiple would have been unthinkable 18 months ago when the stock traded below book value. It signals that investors believe Intel’s massive capital investments will generate substantial future returns — a bet that remains unproven by current profitability metrics.

Key Risks: What Could Derail the Rally?

International investors considering Intel at $108.77 — still 18.1% below its 52-week high of $132.75 — must carefully weigh several risks:

- Execution Risk in Foundry: Intel’s entire re-rating thesis depends on successfully ramping 18A and subsequent nodes for external customers. Any delays, yield issues, or customer defections would undermine the foundry narrative. Manufacturing semiconductors at the leading edge is arguably the most technically challenging industrial process on Earth, and Intel has a recent history of missed timelines.

- Profitability Timeline: The negative ROE of -2.9% underscores that Intel is burning through capital. The company’s free cash flow remains under pressure due to capex spending exceeding $25 billion annually. If the path to profitability takes longer than expected, or if foundry revenue ramps more slowly, the stock’s valuation could face a sharp correction.

- Competitive Threats: TSMC continues to advance its own roadmap and remains the world’s most trusted contract manufacturer. Samsung is also investing heavily. Intel must prove that its technology is not just competitive but reliable enough for risk-averse chip designers to commit their most important products to Intel’s fabs.

- Geopolitical Double-Edged Sword: While U.S.-China tensions boost Intel’s strategic narrative, they also create risks. Export restrictions could limit Intel’s ability to sell into the Chinese market, which has historically been a significant revenue contributor. Additionally, Intel’s planned fab in Magdeburg, Germany adds European subsidy benefits but also introduces regulatory and construction execution risks.

- Currency Considerations for International Investors: Intel is priced in U.S. dollars, and the stock’s performance for non-U.S. investors will be influenced by exchange rate movements. A strengthening dollar could dampen returns when converted back to local currencies, while a weakening dollar would provide a tailwind.

Investment Thesis: Opportunity or Overvaluation?

The bull case for Intel at current levels rests on the foundry transformation thesis. If Intel successfully establishes itself as a viable alternative to TSMC for leading-edge manufacturing, the addressable market is enormous. The global semiconductor foundry market is projected to surpass $150 billion by 2028, and Intel needs to capture only a fraction of this to justify its current $546.7 billion market cap. Add in continued government subsidies, a recovering PC market, and growing AI chip revenue, and the bull case envisions Intel as a $200+ stock within two to three years.

The bear case is equally compelling. A company with negative return on equity, massive ongoing capital requirements, and a foundry business that has yet to generate meaningful external revenue is trading at 4.75x book value and over 10x trailing revenue. If the foundry strategy stumbles — or even just takes longer than expected — the stock could revisit levels far below today’s price. The 52-week range of $18.97 to $132.75 tells its own story: this is an extraordinarily volatile stock, and the path from $19 to $109 does not guarantee the path from $109 to $200.

For international investors specifically, Intel offers something relatively unique in the semiconductor space: direct exposure to U.S. onshoring of chip manufacturing, backed by federal subsidies. This is a structural theme that transcends typical business cycle analysis. However, investors should size positions appropriately given the binary nature of the foundry bet and the current lack of profitability.

The absence of a meaningful dividend — Intel slashed its dividend during its crisis period and has only partially restored it — means this is primarily a capital appreciation story. Income-focused international investors may find better yield elsewhere in the semiconductor sector.

Conclusion

Intel’s transformation from a struggling legacy chipmaker to a $546.7 billion strategic semiconductor powerhouse is one of the most remarkable corporate pivots in recent memory. The stock’s surge from under $19 to $108.77 reflects genuine progress in foundry technology, AI chip development, and geopolitical positioning. Yet the negative ROE, elevated P/B ratio, and unproven foundry revenue trajectory suggest that much of this optimism is already baked into the current price.

For international investors, Intel represents a high-conviction bet on American semiconductor manufacturing resurgence. Those who believe in the foundry thesis and can tolerate significant volatility may find the current 18.1% discount from the 52-week high an attractive entry point. Those who prioritize current profitability and proven cash generation may prefer to wait for clearer evidence that Intel’s massive investments are translating into sustainable returns.

Either way, Intel is no longer a stock that can be ignored. It has earned its place back at the center of the global semiconductor conversation.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any securities. All investors should conduct their own due diligence and consult with a qualified financial advisor before making investment decisions. Past performance is not indicative of future results.