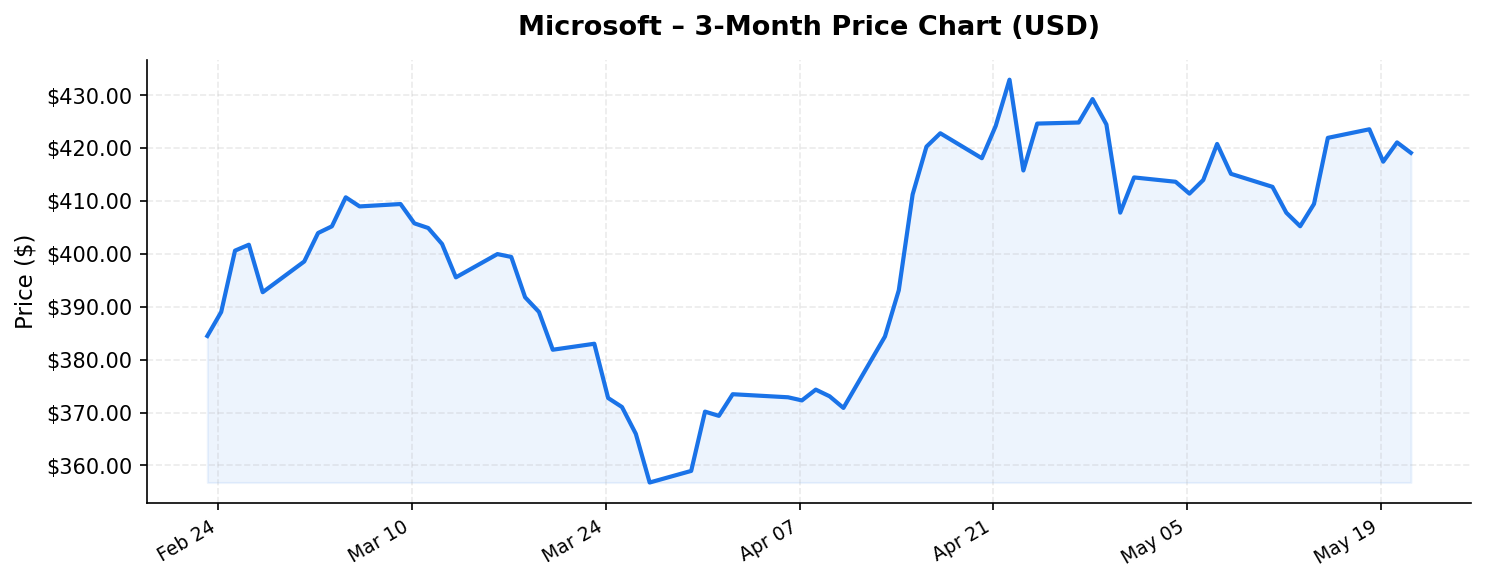

Microsoft (MSFT) finds itself in a curious position in May 2026. The company remains one of the most valuable enterprises on the planet, commanding a market capitalization of $3.1 trillion, yet its stock is trading at $419.09 — a full 24.5% below its 52-week high of $555.45. For international investors scanning the U.S. equity landscape for opportunity, this gap between fundamental strength and price weakness demands a closer look. Is this a compelling entry point into one of technology’s most dominant franchises, or are there structural risks that justify the discount?

In this analysis, we’ll dissect Microsoft’s business fundamentals, competitive positioning, valuation metrics, and key risks to help global investors form a well-informed view.

Business Overview: A $318 Billion Revenue Machine Powered by Cloud and AI

Microsoft has successfully transformed itself over the past decade from a legacy software company into a diversified technology powerhouse. Its trailing twelve-month revenue of $318.3 billion reflects the sheer scale and breadth of its operations, which span three core segments: Intelligent Cloud (anchored by Azure), Productivity and Business Processes (Office 365, LinkedIn, Dynamics), and More Personal Computing (Windows, Xbox, Surface, and search advertising).

The Intelligent Cloud segment, and Azure in particular, remains the primary growth engine. Microsoft has leveraged its early and aggressive partnership with OpenAI to embed generative AI capabilities across its entire product stack — from Copilot integrations in Office 365 and GitHub to Azure AI services that compete head-to-head with Amazon Web Services (AWS) and Google Cloud Platform. This AI-first strategy has driven enterprise adoption at an accelerated pace, contributing meaningfully to the company’s ability to sustain revenue growth even at its enormous scale.

Beyond cloud, Microsoft’s business model benefits from extraordinary recurring revenue characteristics. The shift to subscription-based licensing for Office 365 and Dynamics 365 has created a predictable, high-margin revenue base. LinkedIn continues to grow as a monetization platform for recruitment, advertising, and professional services. And the gaming division, bolstered by the Activision Blizzard acquisition, has expanded Microsoft’s reach into a massive and growing consumer entertainment market.

What makes Microsoft particularly attractive from a financial quality standpoint is its return on equity (ROE) of 34.0%. This figure signals that management is generating substantial profits relative to shareholder capital — a hallmark of companies with durable competitive advantages and disciplined capital allocation.

Valuation Check: What the Numbers Tell International Investors

At a price-to-earnings (P/E) ratio of 24.9x, Microsoft trades at a notable discount to its own historical averages over the past five years, when the stock frequently commanded P/E multiples in the 30x–35x range. For a company generating $318.3 billion in annual revenue with a 34% ROE and a dominant position in secular growth markets like cloud computing and AI, a sub-25x earnings multiple is worth serious attention.

The price-to-book (P/B) ratio of 7.51x may appear elevated at first glance, but it must be contextualized. Microsoft is an asset-light business whose value resides primarily in intellectual property, brand equity, customer relationships, and recurring software subscriptions — none of which are fully captured on the balance sheet. For capital-light, high-ROE businesses, elevated P/B ratios are the norm rather than an anomaly.

The 52-week range of $356.28 to $555.45 tells a story of significant volatility. At $419.09, the stock sits roughly 18% above its 52-week low and 24.5% below its high. This positioning in the lower half of its range suggests the market has repriced Microsoft meaningfully — whether due to broader macroeconomic concerns, sector rotation away from large-cap tech, or company-specific uncertainties around AI monetization timelines and capital expenditure levels.

Perhaps the most striking data point is the reported dividend yield of 87.00%. This figure warrants careful interpretation. If accurate, it would likely reflect a special dividend distribution, a significant capital return event, or a data anomaly. Microsoft has historically maintained a modest but steadily growing ordinary dividend, typically yielding under 1%. International investors should investigate whether this extraordinary yield represents a one-time capital return — such as a large special dividend funded by repatriated overseas cash or balance sheet optimization — or a reporting irregularity. If a genuine special distribution has occurred or is forthcoming, it could represent a highly attractive income event, though investors in many jurisdictions should be aware that U.S. dividends are subject to a 30% withholding tax (often reduced to 15% under tax treaties).

Competitive Position and Strategic Moat

Microsoft’s competitive advantages are multi-layered and deeply entrenched, making it one of the most defensible business franchises in global technology:

- Enterprise ecosystem lock-in: The combination of Windows, Office 365, Azure, Teams, Dynamics 365, and GitHub creates a tightly integrated ecosystem that is extraordinarily difficult for competitors to displace. Migration costs — both financial and operational — are prohibitive for most large organizations.

- AI leadership: Microsoft’s partnership with OpenAI and its integration of large language models across its product suite give it a meaningful first-mover advantage in enterprise AI. Copilot products are generating incremental revenue and increasing customer stickiness.

- Cloud scale: Azure is the second-largest cloud infrastructure platform globally, and its growth rate has consistently outpaced AWS in recent quarters. The hyperscale cloud market remains in a secular growth phase, with enterprises worldwide still in the early-to-middle innings of cloud migration.

- Financial fortress: Microsoft’s balance sheet is among the strongest in corporate America, with substantial cash reserves and investment-grade credit ratings. This financial strength enables aggressive investment in AI infrastructure, strategic acquisitions, and consistent capital returns to shareholders.

- Global diversification: With operations spanning over 190 countries, Microsoft offers international investors natural exposure to global enterprise IT spending — not just the U.S. market.

The combination of these factors creates what Warren Buffett would call a “wide moat” — a sustainable competitive advantage that protects long-term profitability. Few companies in the world can match this breadth and depth of strategic positioning.

Key Risks: What Could Go Wrong

No investment thesis is complete without a clear-eyed assessment of risks. For Microsoft, several bear-case scenarios deserve consideration:

- AI monetization uncertainty: Microsoft has invested tens of billions of dollars in AI infrastructure and its OpenAI partnership. While early Copilot adoption metrics are encouraging, the long-term revenue and margin contribution of generative AI remains uncertain. If AI fails to generate returns commensurate with the capital deployed, it could weigh on profitability and investor sentiment.

- Regulatory and antitrust pressure: As one of the world’s largest companies, Microsoft faces increasing regulatory scrutiny globally — from the European Union’s Digital Markets Act to U.S. antitrust investigations into tech consolidation. Regulatory actions could limit bundling strategies, force structural changes, or impose significant fines.

- Cloud competition intensifying: AWS, Google Cloud, and emerging players are competing aggressively on pricing, capabilities, and AI services. Any deceleration in Azure’s growth rate could disproportionately impact the stock, given how much of the bull narrative rests on cloud momentum.

- Macroeconomic headwinds: A global economic slowdown could lead to reduced enterprise IT spending, delayed cloud migration projects, and lower advertising revenue across LinkedIn and Bing. The stock’s 24.5% decline from its 52-week high may already partially reflect these concerns.

- Currency risk for international investors: Microsoft’s stock is denominated in U.S. dollars. For investors whose home currency is the euro, yen, pound, or any other non-dollar currency, fluctuations in exchange rates can meaningfully amplify or erode returns. A weakening dollar would reduce the value of both capital gains and dividend income when converted back to local currency.

Investment Thesis: Is Microsoft a Buy for International Investors?

The investment case for Microsoft at $419.09 rests on a straightforward premise: this is a world-class business trading at a valuation that is uncharacteristically modest by its own historical standards. A P/E of 24.9x for a company with a 34% ROE, $318.3 billion in revenue, dominant positions in cloud and AI, and a recurring revenue business model represents a potentially attractive risk-reward profile.

The 24.5% drawdown from the 52-week high creates a more favorable entry point than investors have seen in some time, provided you believe the long-term secular trends driving Microsoft’s business — cloud adoption, digital transformation, and enterprise AI — remain intact. The fundamentals strongly suggest they do.

For international investors specifically, Microsoft offers exposure to the beating heart of the global technology economy, denominated in the world’s reserve currency. The company’s global revenue diversification provides a natural hedge against purely domestic U.S. economic risks. However, currency exposure, withholding tax implications on dividends, and the need to verify the extraordinary reported dividend yield should all factor into portfolio decisions.

The bottom line: Microsoft remains one of the highest-quality businesses available in public markets. At current levels, the stock appears to offer a rare combination of quality and relative value. Patient, long-term investors may find this an opportune moment to build or add to a position — while remaining mindful of the risks that accompany any equity investment at this scale.

Disclaimer: This blog post is for informational and educational purposes only. It does not constitute financial advice, investment advice, or a recommendation to buy or sell any securities. All investors should conduct their own due diligence and consult with a qualified financial advisor before making investment decisions. Market data referenced is as of May 22, 2026, and may have changed since publication.