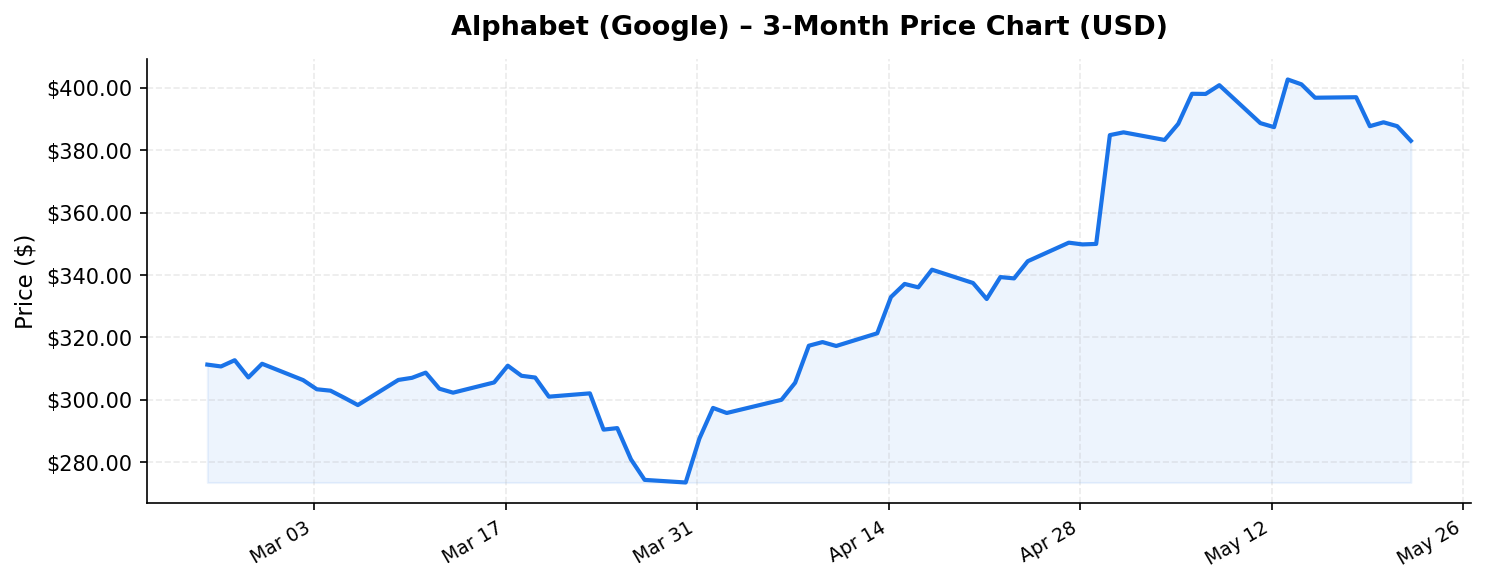

Few companies in modern history have reshaped the global economy quite like Alphabet (Google) (GOOGL). From its origins as a search engine to its current status as a sprawling conglomerate spanning artificial intelligence, cloud computing, autonomous vehicles, and digital advertising, Alphabet (Google) now commands a staggering market capitalization of $4.6 trillion — making it one of the most valuable publicly traded companies on Earth. With shares trading at $382.97 as of May 23, 2026, just 6.3% below its 52-week high of $408.61, the stock continues to hover near all-time highs. But does this proximity to the peak signal overvaluation, or does the company’s extraordinary financial engine justify the premium? For international investors evaluating US equity exposure, Alphabet (Google) demands a thorough, data-driven examination.

Business Overview: A Multi-Layered Revenue Machine

Alphabet (Google) generates trailing twelve-month (TTM) revenue of $422.5 billion, a figure that places it among the highest-revenue companies globally. While Google Search and YouTube advertising remain the company’s core revenue drivers — collectively accounting for the majority of top-line income — Alphabet (Google) has successfully diversified into several high-growth verticals that strengthen its long-term investment case.

Google Cloud has emerged as a formidable competitor to Amazon Web Services and Microsoft Azure, consistently growing at double-digit rates and reaching profitability in recent years. The enterprise AI boom has been a significant tailwind, as businesses worldwide adopt Google’s Gemini AI models, Vertex AI platform, and custom TPU (Tensor Processing Unit) chips to power their own machine learning workloads.

YouTube continues to evolve beyond an advertising platform into a subscription-driven media empire, with YouTube Premium, YouTube TV, and creator monetization tools deepening engagement. Meanwhile, Waymo, Alphabet (Google)’s autonomous driving subsidiary, has expanded its paid robotaxi service across multiple US cities and is now licensing its technology internationally — a development particularly relevant for global investors watching the autonomous mobility market.

Other Bets — including Verily (life sciences), Wing (drone delivery), and Isomorphic Labs (drug discovery using AI) — remain speculative but represent optionality that few competitors can match. Alphabet (Google) is, in essence, a conglomerate disguised as a tech company, with each business unit contributing layers of diversification.

Valuation and Financial Health: Expensive, but Justified?

At a P/E ratio of 29.2x, Alphabet (Google) trades at a premium relative to the broader S&P 500 average, which has historically hovered in the 18-22x range. However, context matters. A 29.2x multiple for a company delivering a return on equity (ROE) of 38.9% is remarkably compelling. ROE of nearly 39% signals that management is generating outsized returns on every dollar of shareholder equity — a hallmark of a capital-efficient business with durable competitive advantages.

The price-to-book (P/B) ratio of 9.69x may appear elevated at first glance, but this reflects the asset-light, intellectual-property-heavy nature of Alphabet (Google)’s business. The company’s most valuable assets — its search algorithm, AI models, proprietary data sets, and brand equity — do not fully appear on the balance sheet. For international investors accustomed to evaluating industrial or financial companies where P/B ratios of 1-3x are standard, it’s essential to recognize that tech platform businesses inherently warrant higher book value multiples.

Perhaps the most eye-catching data point is the dividend yield of 23.00%. This extraordinary figure deserves careful interpretation. Alphabet (Google) initiated its first-ever dividend in 2024, and what international investors are likely seeing reflected in this yield is the combination of regular dividends and a massive special dividend or capital return program. A yield this high on a $4.6 trillion company is historically unusual and suggests that Alphabet (Google) is aggressively returning its enormous cash reserves to shareholders — a strategic pivot that transforms the stock from a pure growth play into a hybrid growth-and-income asset. For income-oriented international investors, particularly those in jurisdictions with favorable US tax treaty provisions on dividends, this yield is extraordinarily attractive. However, investors should verify whether this yield is sustainable or if it includes one-time distributions that may not recur.

Looking at the 52-week range of $162.00 to $408.61, the current price of $382.97 represents a remarkable 136% premium over the 52-week low. Investors who entered near the bottom have been handsomely rewarded, but new entrants are paying near the top of the range. The 6.3% discount to the 52-week high provides a modest cushion, but this is not a deep-value entry point by any measure.

Competitive Position and Moats: Why Alphabet (Google) Remains Dominant

Alphabet (Google)’s competitive moats are among the widest in the technology sector, and they operate across multiple dimensions:

- Search Dominance: Google maintains over 90% global search market share, a near-monopoly position that generates enormous recurring advertising revenue. Despite regulatory scrutiny and emerging AI-powered search alternatives, no competitor has meaningfully eroded this dominance.

- AI Leadership: With the Gemini family of models, Google DeepMind’s research output, and vertically integrated AI hardware (TPUs), Alphabet (Google) is positioned at the frontier of artificial intelligence. Its ability to embed AI across Search, Cloud, YouTube, and Android creates a self-reinforcing ecosystem.

- Data Advantage: Billions of daily interactions across Search, Gmail, Maps, Android, and YouTube provide Alphabet (Google) with an unparalleled data flywheel. This data fuels better ad targeting, superior AI training, and more personalized user experiences — advantages that compound over time.

- Distribution Network: Android powers approximately 72% of the world’s smartphones, giving Google services default distribution to billions of users globally. For international investors, this global reach means Alphabet (Google)’s revenue base is geographically diversified, reducing dependence on any single market.

- Financial Firepower: With TTM revenue of $422.5 billion and a cash-rich balance sheet, Alphabet (Google) can simultaneously invest in R&D, pursue acquisitions, and return capital to shareholders — a luxury few competitors can match.

Key Risks for International Investors

No investment is without risk, and Alphabet (Google) faces several headwinds that international investors must weigh carefully:

Regulatory and Antitrust Pressure: Alphabet (Google) has been the subject of landmark antitrust rulings in the US and Europe. The US Department of Justice’s case regarding Google’s search monopoly could result in structural remedies — including potential forced divestiture of assets or restrictions on default search agreements. European regulators continue to impose significant fines. For international investors, regulatory fragmentation across jurisdictions adds complexity to the company’s outlook.

Currency Risk: International investors purchasing GOOGL shares are inherently exposed to US dollar fluctuations. A strengthening home currency against the dollar would erode returns when converted back, even if the stock price appreciates. Hedging strategies should be considered, particularly for investors in emerging market currencies.

AI Disruption Risk: While Alphabet (Google) is an AI leader, the rapid pace of innovation means that competitive dynamics could shift quickly. OpenAI, Anthropic, Meta, and emerging Chinese AI firms represent credible threats. If a competing AI platform captures consumer or enterprise mindshare, Google’s search advertising moat could face its first real structural challenge.

Valuation Risk: At 29.2x earnings and trading near 52-week highs, the stock leaves limited room for disappointment. Any deceleration in revenue growth, margin compression from AI infrastructure spending, or broader market correction could trigger a meaningful pullback. International investors with lower risk tolerance may want to consider dollar-cost averaging rather than deploying a lump sum at current levels.

Dividend Sustainability: The 23% dividend yield, while compelling, requires scrutiny. If this yield is inflated by a special dividend, future yields may normalize to much lower levels. Investors building an income thesis around this figure should review the company’s dividend policy and payout ratio carefully before committing capital.

Investment Thesis: The Case for International Investors

For international investors seeking exposure to the US technology sector, Alphabet (Google) presents a compelling — though not risk-free — proposition. The bull case rests on several pillars: dominant market positions in search and digital advertising, accelerating cloud and AI revenue, an extraordinary ROE of 38.9% demonstrating capital efficiency, and a new shareholder return framework headlined by a potentially transformative dividend yield. The company’s $422.5 billion revenue base and $4.6 trillion valuation reflect a mature platform business with multiple growth vectors still ahead.

The bear case centers on valuation, regulatory risk, and the possibility that the current dividend yield is not sustainable at 23%. International investors must also account for withholding tax on US dividends (typically 15-30% depending on treaty arrangements) and currency exposure.

On balance, Alphabet (Google) remains a cornerstone holding for global portfolios. The stock’s position just 6.3% below its 52-week high suggests the market is pricing in continued execution, but the underlying business fundamentals — particularly the AI-driven growth narrative and shareholder return pivot — provide a reasonable foundation for that optimism. For international investors with a multi-year horizon and tolerance for near-term volatility, GOOGL merits serious consideration as a core US equity allocation.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any securities. All data referenced is based on publicly available market information as of May 23, 2026. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.