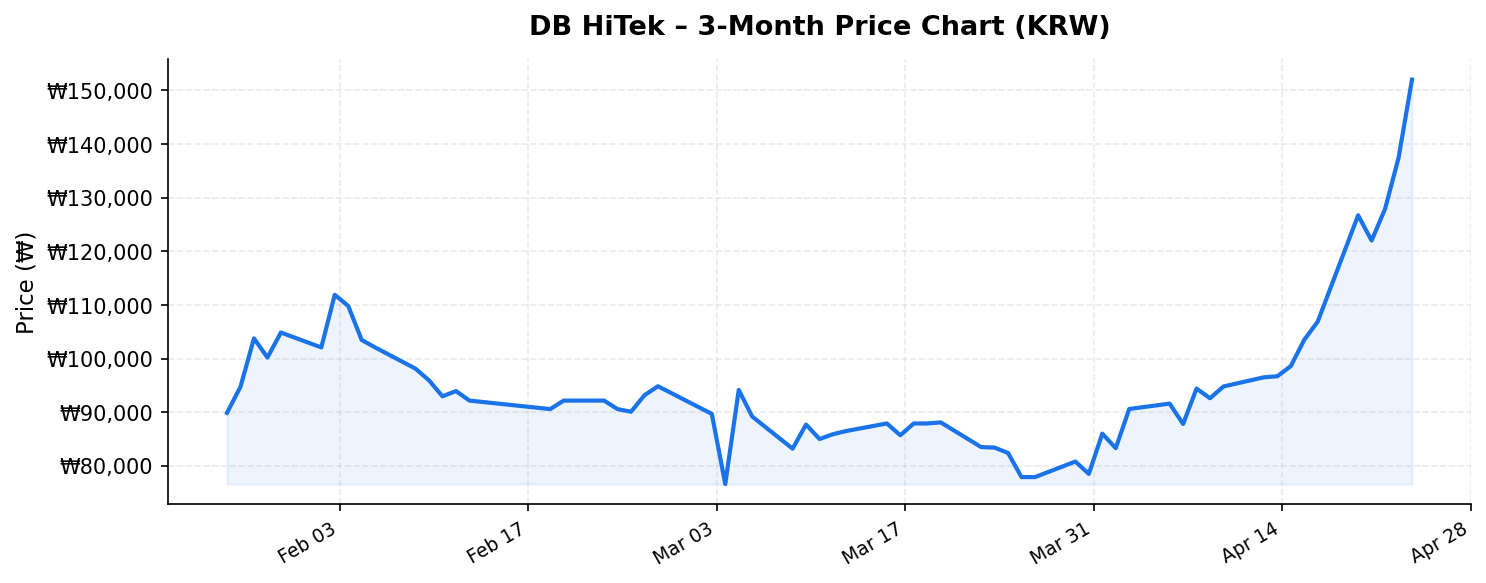

In a global semiconductor landscape increasingly dominated by conversations about cutting-edge nodes and AI chips, one Korean specialty foundry has quietly delivered a performance that demands attention from international investors. DB HiTek (DB하이텍, 000990.KS), a mid-sized pure-play foundry specializing in analog and mixed-signal semiconductors, is currently trading at ₩152,000 per share — just 4.5% below its 52-week high of ₩159,200 — and sports what appears to be an eye-popping dividend yield of 53%. With a market capitalization of approximately ₩6.1 trillion (roughly $4.5 billion USD) and trailing twelve-month revenue of ₩1.4 trillion, this company sits at a fascinating intersection of value, income, and structural semiconductor demand. But the headline numbers tell only part of the story. Let’s unpack what’s really going on.

Business Overview: The Power of Analog in a Digital World

DB HiTek operates as a specialty semiconductor foundry, meaning it manufactures chips designed by other companies (fabless firms) rather than designing its own. What distinguishes DB HiTek from giants like TSMC or Samsung Foundry is its deliberate focus on mature process nodes — typically 90nm and above — serving the analog, mixed-signal, power management, and display driver IC (DDIC) markets. These are the unglamorous but indispensable chips found in automobiles, industrial equipment, consumer electronics, IoT devices, and power systems.

Unlike the relentless race to sub-3nm nodes that consumes tens of billions in capital expenditure, DB HiTek’s mature-node strategy requires far less investment while generating stable, high-margin revenue. The company operates two fabrication facilities (fabs) in Bucheon, South Korea, with combined capacity that has been running at high utilization rates as demand for analog and power semiconductors remains robust, driven by secular trends in electrification, automotive electronics, and industrial automation.

The company’s customer base is diversified across geographies and end markets, with significant exposure to display drivers (serving the LCD and OLED panel supply chain), automotive power management ICs, and sensor chips. This positioning makes DB HiTek a beneficiary of multiple long-term megatrends without the binary risk associated with bleeding-edge technology bets.

Valuation, Price Action, and That Extraordinary Dividend Yield

The most arresting figure in DB HiTek’s current market data is undoubtedly the 53% dividend yield. Before investors rush to buy, this number warrants careful scrutiny. A yield of this magnitude on a stock trading near its 52-week high almost certainly reflects a special or extraordinary dividend rather than a sustainable recurring payout. Given the company’s TTM revenue of ₩1.4 trillion and market cap of ₩6.1 trillion, a 53% yield would imply total dividend payments exceeding ₩3.2 trillion — a figure that would far surpass normal earnings capacity and suggests a major capital return event.

There are several plausible explanations. DB HiTek has been the subject of ongoing corporate restructuring discussions within the DB Group conglomerate. In recent years, there has been significant speculation — and at times concrete proposals — around the potential sale or delisting of DB HiTek, with its parent company DB Inc. holding a controlling stake. A massive special dividend could be part of a process to return accumulated cash reserves to shareholders prior to a corporate action, or it may reflect the distribution of proceeds from asset sales or restructuring. International investors should investigate the specific composition of this dividend (ordinary vs. special) before building a yield-based thesis.

Looking at the broader valuation picture, the stock’s remarkable journey from its 52-week low of ₩37,550 to its current price of ₩152,000 represents a roughly 305% gain — a move that likely reflects a combination of improved semiconductor cycle dynamics, the anticipated special dividend, and potential corporate event premiums. At ₩152,000, the stock trades at a price-to-sales ratio of approximately 4.4x on TTM revenue, which is not cheap for a mature-node foundry but may be justified if profitability is strong. The return on equity of 11.9% is solid, though not spectacular, suggesting the company generates reasonable returns on its asset base without excessive leverage.

The proximity to the 52-week high (only 4.5% below ₩159,200) indicates strong positive momentum, but it also means investors buying today have limited margin of safety from a technical perspective. The distance from the 52-week low is so vast that any retracement could be severe if the catalyst driving the rally — likely the special dividend or corporate event — fails to materialize as expected.

Competitive Position and Structural Tailwinds

DB HiTek occupies a defensible niche in the global foundry hierarchy. While TSMC, Samsung, and Intel battle for supremacy in advanced nodes, the mature-node foundry market has its own competitive dynamics. Key competitors include Taiwan’s Vanguard International Semiconductor (VIS), China’s Hua Hong Semiconductor, and to some extent, GlobalFoundries and UMC. DB HiTek’s advantages include:

- Specialized process platforms: The company has developed proprietary process technologies for BCD (Bipolar-CMOS-DMOS) power management, high-voltage display drivers, and MEMS sensors that create meaningful switching costs for customers.

- Geopolitical positioning: As a Korean-based foundry, DB HiTek benefits from relative geopolitical neutrality compared to Chinese competitors facing potential sanctions or Taiwanese fabs exposed to cross-strait risks. For customers seeking supply chain diversification, Korean foundries represent an attractive middle ground.

- Capacity discipline: Unlike some Chinese competitors who have aggressively expanded mature-node capacity (often with government subsidies), DB HiTek has maintained capacity discipline, supporting pricing power and utilization rates.

- Automotive and industrial exposure: The secular shift toward vehicle electrification and advanced driver-assistance systems (ADAS) is driving sustained demand for analog and power semiconductors, areas where DB HiTek has deep expertise.

The structural undersupply in certain mature-node categories — a phenomenon that became globally visible during the 2021-2022 chip shortage — has led to longer-term supply agreements and more rational pricing in the industry. DB HiTek has been a direct beneficiary of this trend, and with limited new mature-node capacity coming online globally (new fabs overwhelmingly target advanced nodes), the supply-demand balance should remain favorable.

Key Risks for International Investors

Despite the compelling narrative, DB HiTek presents several risks that international investors must weigh carefully:

- Special dividend dependency: If the 53% dividend yield is indeed driven by a one-time event, investors buying at current levels for income may be disappointed by future ordinary dividends. The stock could reprice significantly lower once the special dividend is paid and the ex-dividend date passes.

- Corporate governance and controlling shareholder risk: The DB Group’s controlling stake means minority shareholders have limited influence over major corporate decisions, including potential delistings, mergers, or asset transfers that may not maximize minority shareholder value. Korea’s historically mixed track record on minority shareholder protection — though improving under recent “Corporate Value-Up” initiatives — remains a concern.

- Cyclicality: While analog semiconductors are less cyclical than memory chips, they are not immune to downturns. A global economic slowdown affecting automotive production, industrial capital expenditure, or consumer electronics demand would pressure DB HiTek’s utilization rates and margins.

- Chinese competition: Government-subsidized expansion of mature-node capacity in China remains a medium-term threat. If Chinese foundries succeed in capturing market share through aggressive pricing, DB HiTek’s pricing power could erode.

- Currency risk: For international investors, the KRW/USD exchange rate adds a layer of volatility. A strengthening won enhances dollar-denominated returns, while depreciation erodes them — independent of the company’s operational performance.

- Liquidity: With a ₩6.1 trillion market cap, DB HiTek is a mid-cap stock by Korean standards. Trading volumes may be insufficient for large institutional investors to build or exit positions efficiently, and the free float may be limited given the controlling shareholder’s stake.

Investment Thesis: Opportunity or Trap?

For international investors, DB HiTek presents a nuanced opportunity. The bull case rests on several pillars: a structurally advantaged position in the mature-node foundry market, exposure to durable secular growth themes (EVs, industrial automation, IoT), reasonable profitability (11.9% ROE), and the potential for significant near-term capital returns via the extraordinary dividend. If the special dividend materializes as implied by the 53% yield, investors who time their entry before the record date could capture a substantial cash return.

The bear case centers on the post-dividend repricing risk, the possibility that current prices already fully reflect the special dividend, and the ongoing corporate governance uncertainties surrounding the DB Group’s strategic intentions. A stock that has rallied 305% from its 52-week low carries significant momentum-reversal risk.

The most prudent approach for international investors may be to view DB HiTek through a dual lens: as a fundamentally sound specialty foundry with long-term secular tailwinds, and as a near-term event-driven situation requiring careful analysis of dividend mechanics, ex-dividend dates, and Korean tax withholding implications (Korea typically withholds 22% on dividends paid to foreign investors, though treaty rates may apply). Those comfortable with the complexity may find a genuinely differentiated semiconductor investment that offers something rare in today’s market — a specialty foundry with real income potential trading near the top of its range on the back of concrete catalysts.

With the stock at ₩152,000 and the 52-week high at ₩159,200, the technical picture suggests the market is pricing in a positive outcome. Whether that outcome has already been fully discounted is the critical question every investor must answer for themselves.

Disclaimer: This blog post is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy or sell any security. The data presented reflects market conditions as of April 26, 2026, and may not be current at the time of reading. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. Investing in foreign securities involves additional risks, including currency fluctuation, political instability, and differing regulatory environments.