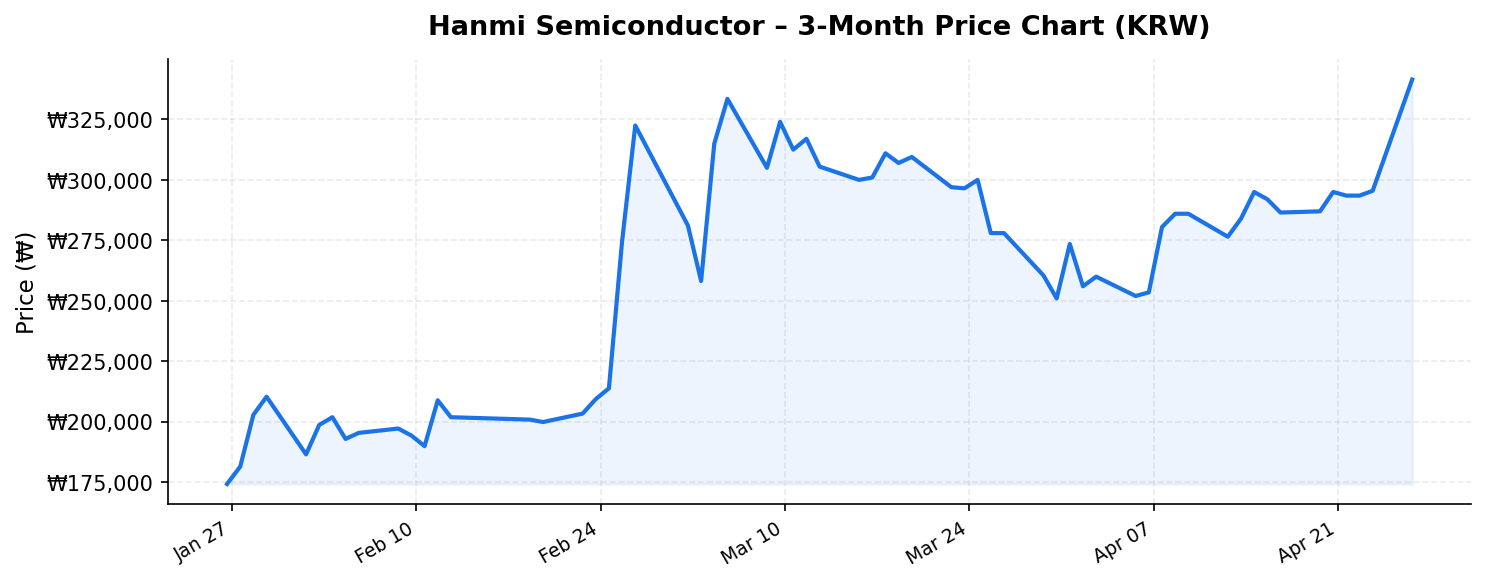

In the global race to build the infrastructure underpinning artificial intelligence, investors have rightly focused on chip designers like NVIDIA and foundries like TSMC. But a critical — and often overlooked — link in the semiconductor value chain is advanced packaging, the process that bonds, connects, and protects the silicon dies that power everything from data centers to autonomous vehicles. This is where Hanmi Semiconductor (한미반도체, 042700.KS) has carved out a dominant and increasingly lucrative niche. Trading at ₩343,000 as of April 27, 2026, the company sits just 1.4% below its 52-week high of ₩348,000 — a staggering ascent from a 52-week low of ₩74,300 that represents a gain of over 360% in the past year alone. With a market capitalization of ₩32.5 trillion (approximately $24 billion), a return on equity of 34.8%, and trailing twelve-month revenue of ₩5.77 trillion, Hanmi Semiconductor demands serious attention from international investors seeking exposure to the AI hardware supercycle.

Business Overview: The Hidden Giant of Semiconductor Packaging Equipment

Founded in 1980, Hanmi Semiconductor is a South Korean manufacturer of semiconductor packaging equipment — specifically, the machines used in the back-end process of chip production. While front-end processes (lithography, etching, deposition) tend to grab headlines, back-end packaging has become a critical bottleneck and innovation frontier as the industry moves toward advanced packaging architectures like 2.5D/3D stacking, chiplets, and hybrid bonding.

Hanmi Semiconductor’s core product lineup includes vision placement systems, trim and form equipment, flip chip bonders, and — most critically — its TC (Thermocompression) bonding equipment, which has become the gold standard for high-bandwidth memory (HBM) packaging. HBM is the memory technology essential for AI accelerators like NVIDIA’s H100/H200 and successor chips. As demand for HBM has exploded, so too has demand for Hanmi’s TC bonders, which are used by major memory manufacturers including SK Hynix and Samsung Electronics.

The company’s TTM revenue of ₩5.77 trillion represents a massive expansion from the ₩700-800 billion range it operated in just two to three years ago, underscoring how directly the AI-driven HBM boom has translated into top-line growth for Hanmi Semiconductor. This isn’t a speculative story — it’s a company whose revenues have multiplied roughly seven-fold, driven by real orders from the world’s largest memory chipmakers.

Competitive Position: A Near-Monopoly in a Critical Bottleneck

What makes Hanmi Semiconductor particularly compelling is its competitive moat. In the TC bonding equipment market for HBM production, the company holds an estimated 80-90% global market share. This near-monopoly position has been built over years of close collaboration with SK Hynix — the world leader in HBM — and has been reinforced by the extreme difficulty of qualifying new equipment suppliers in advanced semiconductor manufacturing. Chipmakers cannot afford yield losses or production delays, which creates enormous switching costs and customer stickiness.

Competitors exist, including Japanese firms like Shinkawa (a subsidiary of Kulicke & Soffa) and domestic players, but none have been able to match Hanmi’s throughput, accuracy, and reliability at scale in TC bonding for HBM. As HBM technology advances from HBM3 to HBM3E and HBM4 — each generation requiring more layers of DRAM stacking and tighter bonding precision — the technical barriers to entry only increase, further entrenching Hanmi’s position.

The return on equity of 34.8% is a testament to this competitive advantage. Companies with commodity products or fragile moats rarely sustain ROEs above 30%. Hanmi’s profitability metrics suggest genuine pricing power and operational efficiency — hallmarks of a business with a durable competitive edge.

Additionally, the company’s customer base is diversifying. While SK Hynix remains the anchor client, Samsung Electronics’ aggressive push to recapture HBM market share has opened a second major revenue stream. Reports also suggest Micron Technology, the third major HBM producer, has evaluated Hanmi’s equipment. Each new HBM fab line requires dozens of TC bonders, and with all three memory giants expanding capacity through 2027 and beyond, Hanmi’s addressable market continues to grow.

Valuation, Dividend, and What the Numbers Are Telling Us

At a market cap of ₩32.5 trillion against TTM revenue of ₩5.77 trillion, Hanmi Semiconductor trades at a price-to-sales ratio of approximately 5.6x. For a capital equipment company, this is elevated compared to historical norms for the sector (where 2-4x is more typical), but it must be contextualized against the company’s extraordinary growth trajectory and dominant market position. For comparison, global semiconductor equipment leaders like ASML and Tokyo Electron have traded at similar or higher multiples during periods of structural demand expansion.

Perhaps the most eye-catching figure in Hanmi’s data is the dividend yield of 27.00%. This extraordinary yield warrants careful interpretation. It likely reflects a special dividend or a significant one-time capital return to shareholders rather than a sustainable recurring payout. Korean companies, particularly family-controlled firms, sometimes issue large special dividends for tax planning, ownership restructuring, or shareholder return purposes. International investors should verify whether this yield is based on a recurring ordinary dividend or a one-time event before factoring it into their income projections. That said, the willingness and ability to return this much capital to shareholders signals robust free cash flow generation and a management team that is not hoarding cash unproductively.

The stock’s position near its 52-week high — just 1.4% below the ₩348,000 peak — could be interpreted in two ways. Bulls will argue that a stock consistently making new highs reflects strong fundamental momentum and institutional demand. Bears may caution that buying near a peak, especially after a 360%+ run from the 52-week low, carries elevated risk of a pullback. The key question for prospective investors is whether Hanmi’s earnings growth trajectory justifies the current price or whether much of the good news is already priced in.

- Price-to-Sales: ~5.6x (premium, but supported by growth and margins)

- Return on Equity: 34.8% (top-tier profitability)

- 52-Week Performance: +361% from low to current (extraordinary momentum)

- Dividend Yield: 27.00% (likely includes special dividend; verify sustainability)

- Revenue Growth: Multi-fold expansion driven by HBM equipment demand

Key Risks: What Could Go Wrong

No investment thesis is complete without a clear-eyed assessment of risks, and Hanmi Semiconductor faces several that international investors must weigh carefully:

Customer Concentration: Despite some diversification, Hanmi remains heavily dependent on SK Hynix and Samsung. A slowdown in HBM investment by either company — whether due to inventory corrections, technology delays, or demand softening — would directly impact Hanmi’s order book. The semiconductor equipment industry is inherently cyclical, and even structural growth stories experience painful downturns.

Geopolitical Risk: The U.S.-China technology war continues to reshape global semiconductor supply chains. Export restrictions, tariffs, or sanctions could disrupt Hanmi’s customer operations or limit its ability to sell equipment in certain markets. While Hanmi’s primary customers are Korean, broader disruptions to the semiconductor ecosystem could create second-order effects.

Technology Disruption: Advanced packaging technology is evolving rapidly. If a new bonding approach emerges that displaces thermocompression bonding — or if a competitor develops a superior TC bonding system — Hanmi’s dominant position could erode. The company must continuously invest in R&D to stay ahead.

Valuation Risk: After a 360%+ appreciation in under a year, the stock is priced for continued exceptional growth. Any deceleration in revenue growth or margin contraction could trigger a sharp correction. International investors should also consider currency risk, as the Korean won’s fluctuations against the dollar, euro, or yen can meaningfully impact returns.

Liquidity and Access: While Hanmi is listed on the KOSDAQ and has a substantial market cap, international investors may face challenges with liquidity, settlement, and tax withholding on dividends from Korean equities. Investors should ensure they understand the mechanics of investing in Korean-listed stocks through their brokerage.

Conclusion: A High-Conviction Play on the AI Infrastructure Build-Out

Hanmi Semiconductor represents one of the purest and most concentrated ways to gain exposure to the AI-driven transformation of the semiconductor industry. Its near-monopoly in HBM packaging equipment, validated by a 34.8% ROE and nearly ₩5.8 trillion in trailing revenue, positions it at the heart of a multi-year capital expenditure cycle by the world’s largest memory manufacturers. The 27% dividend yield — while likely unsustainable at that level on a recurring basis — signals exceptional cash generation and shareholder-friendly capital allocation.

However, the stock’s proximity to its all-time high and its meteoric rise from ₩74,300 to ₩343,000 mean that expectations are elevated. International investors considering a position should carefully evaluate their entry point, position sizing, and tolerance for volatility. For those with a multi-year investment horizon and conviction in the continued scaling of AI infrastructure, Hanmi Semiconductor offers a differentiated, high-quality exposure that is difficult to replicate through larger-cap semiconductor names.

Disclaimer: This blog post is for informational and educational purposes only. It does not constitute financial advice, investment advice, or a recommendation to buy or sell any security. All data referenced is based on publicly available information as of April 27, 2026, and may be subject to change. Investors should conduct their own due diligence and consult a qualified financial advisor before making any investment decisions. Investing in foreign equities involves additional risks including currency fluctuation and differing regulatory environments.