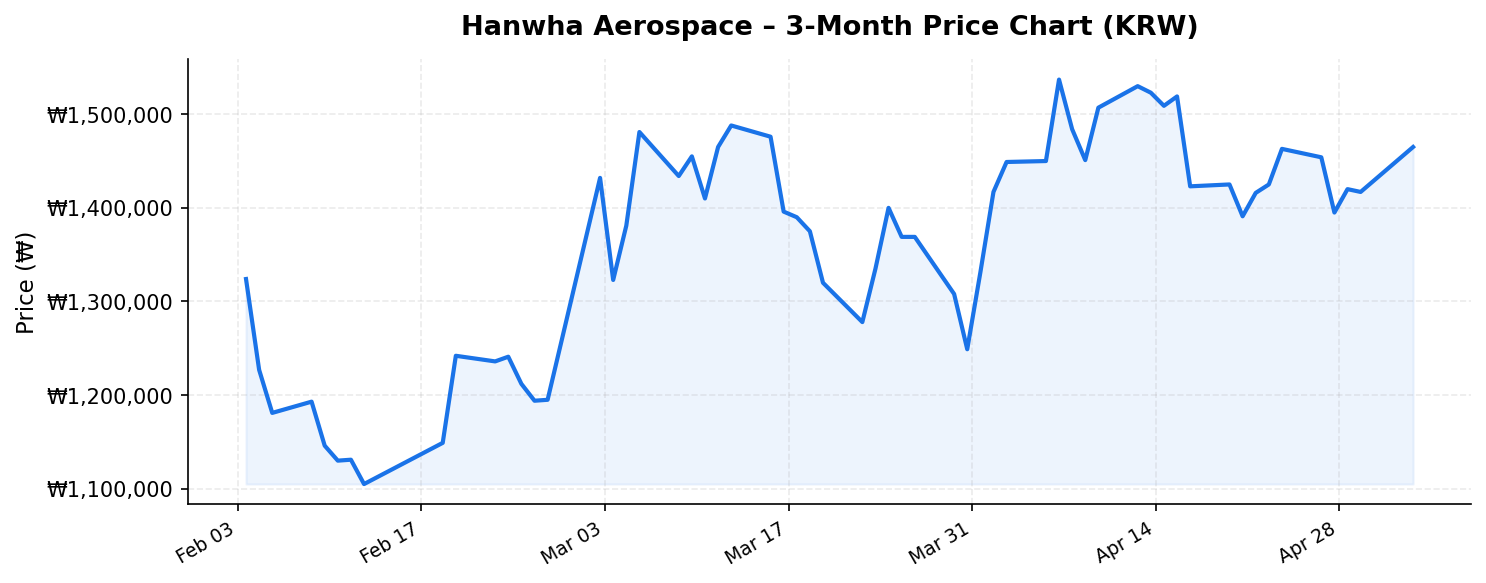

South Korea’s defense and aerospace sector has undergone a remarkable transformation over the past several years, evolving from a domestically focused industry into a globally competitive force. At the center of this evolution stands Hanwha Aerospace (한화에어로스페이스, 012450.KS), a company that has become one of the most closely watched names on the Korea Exchange. Trading at ₩1,465,000 per share with a market capitalization of ₩75.4 trillion (approximately $55 billion USD), Hanwha Aerospace has firmly established itself as one of Korea’s most valuable companies. But with the stock sitting 11.5% below its 52-week high of ₩1,655,000 and sporting a headline dividend yield that demands scrutiny, international investors are right to ask: is this a compelling entry point, or is the easy money already made?

Business Overview: More Than Just Engines and Missiles

Hanwha Aerospace is the flagship defense and aerospace subsidiary of the Hanwha Group, one of South Korea’s largest conglomerates. The company’s operations span four core segments: aircraft engines, defense systems, space and satellite technology, and industrial equipment. Its product portfolio includes gas turbine engines for military and civilian aircraft, self-propelled howitzers (most notably the K9 Thunder, which has become a global export sensation), missile and munitions systems, and satellite components.

The company’s trailing twelve-month revenue of ₩26.7 trillion underscores the sheer scale of its operations. This revenue base has expanded dramatically in recent years, driven by a surge in global defense spending, major export contracts, and the consolidation of Hanwha Group’s defense assets under one roof. Hanwha Aerospace has also aggressively expanded into the space economy, investing in satellite manufacturing, launch vehicle components, and urban air mobility (UAM) platforms — positioning itself at the intersection of traditional defense and next-generation aerospace technologies.

A critical part of the Hanwha Aerospace story is its subsidiary structure. The company holds significant stakes in Hanwha Ocean (formerly DSME), the shipbuilder that has become a strategic asset amid rising global demand for naval vessels and submarines. This conglomerate structure adds complexity to valuation but also provides diversified exposure to multiple facets of the defense-industrial ecosystem.

Competitive Position and Global Export Momentum

Hanwha Aerospace’s competitive moat is built on several pillars. First, the K9 self-propelled howitzer has become the world’s most exported artillery platform, with contracts spanning Poland, Australia, Egypt, Norway, Finland, Estonia, and India, among others. Poland’s landmark order alone — one of the largest defense deals in European history — has provided multi-year revenue visibility and cemented Hanwha’s reputation as a reliable partner for NATO-aligned nations seeking to rebuild their defense capabilities in the wake of the Russia-Ukraine conflict.

Second, the company’s engine division has deepened its partnership with global OEMs, including collaborations on next-generation fighter jet engines and civilian aerospace propulsion systems. This positions Hanwha Aerospace to capture a growing share of the global aeroengine aftermarket, one of the most profitable segments in the aerospace value chain.

Third, Hanwha’s space ambitions are not speculative — they are backed by real contracts and government partnerships. South Korea’s national space program has accelerated, and Hanwha Aerospace is a primary contractor for satellite systems and launch vehicle propulsion. The global space economy, projected to exceed $1 trillion by the early 2030s, represents a long-duration growth vector that few traditional defense companies can credibly claim.

With a return on equity of 15.6%, Hanwha Aerospace demonstrates solid capital efficiency for a heavy-industry defense company. This ROE compares favorably with many global defense peers and suggests that management is deploying capital effectively even as it invests heavily in growth initiatives. The TTM revenue of ₩26.7 trillion, when measured against the ₩75.4 trillion market cap, implies a price-to-sales ratio of roughly 2.8x — a premium to some traditional defense names but arguably justified given the company’s growth trajectory and diversified business mix.

Valuation, Dividend, and Share Price Analysis

The current share price of ₩1,465,000 places Hanwha Aerospace 11.5% below its 52-week high of ₩1,655,000 and roughly 93% above its 52-week low of ₩760,000. This range tells a compelling story: the stock has nearly doubled from its lows as the global defense upcycle accelerated, but the recent pullback from highs suggests that either profit-taking or broader market caution has created a potential re-entry window for patient investors.

The most striking figure in the live data is the reported dividend yield of 49.00%. This extraordinary number warrants careful interpretation. Such a yield is almost certainly the result of a special or one-time dividend distribution rather than a sustainable ongoing payout. Hanwha Group has been actively restructuring its corporate holdings, and special dividends — often used to facilitate intra-group transactions, return proceeds from asset sales, or reward shareholders during corporate restructuring events — can produce headline yields that dramatically overstate the recurring income an investor should expect. International investors should look past this figure and examine the company’s ordinary dividend history and payout ratio to set realistic income expectations. Historically, Hanwha Aerospace’s regular dividend yield has been modest, typically in the low single digits. The 49% yield is a data anomaly that, while potentially rewarding for shareholders who held through the distribution, should not be extrapolated forward.

From a valuation perspective, the ₩75.4 trillion market cap makes Hanwha Aerospace one of the largest pure-play defense names globally, rivaling European giants like BAE Systems and Rheinmetall. Whether this valuation is sustainable depends largely on the company’s ability to convert its massive order backlog into delivered revenue and earnings growth over the next three to five years. The current P/S ratio of approximately 2.8x is not cheap by historical Korean market standards, but it reflects the market’s expectation that defense spending tailwinds will persist and that Hanwha Aerospace’s export franchise will continue to scale.

Key Risks for International Investors

No investment thesis is complete without a thorough assessment of risks, and Hanwha Aerospace presents several that international investors must consider:

- Geopolitical Execution Risk: While rising global tensions have fueled the defense spending boom, the same geopolitical dynamics can create supply chain disruptions, contract delays, or diplomatic complications. South Korea’s complex relationships with North Korea, China, Japan, and the United States add layers of political risk that don’t affect Western defense contractors to the same degree.

- Conglomerate Discount and Governance: Hanwha Aerospace is part of the broader Hanwha chaebol structure, which can lead to related-party transactions, complex cross-shareholdings, and governance concerns that are common across Korean conglomerates. International investors accustomed to Western corporate governance standards should scrutinize related-party dealings carefully.

- Currency Risk: The stock is denominated in Korean won, and many of its export contracts are priced in USD or EUR. Fluctuations in the KRW can amplify or dampen returns for foreign investors. A strengthening won could compress export margins, while a weakening won could boost translated earnings but erode returns for dollar-based investors.

- Valuation Stretch: Having nearly doubled from its 52-week low, Hanwha Aerospace’s stock price already reflects significant optimism. Any disappointment in order intake, contract execution, or margin performance could trigger sharp corrections. The stock’s 11.5% discount to its 52-week high may not represent sufficient margin of safety for risk-averse investors.

- Special Dividend Misinterpretation: As noted above, the 49% dividend yield is almost certainly a non-recurring event. Investors buying the stock for income based on this figure will likely be disappointed by future payouts.

Investment Thesis: A Structural Winner in the Global Defense Upcycle

For international investors seeking exposure to the global defense spending supercycle, Hanwha Aerospace offers a differentiated value proposition. Unlike Western defense primes that are largely mature, slow-growing businesses, Hanwha Aerospace is in a high-growth phase — aggressively scaling exports, expanding into space and UAM, and consolidating its position as the Korean defense champion. The TTM revenue of ₩26.7 trillion and a 15.6% ROE demonstrate that this growth is being achieved with reasonable capital discipline.

The 11.5% pullback from the 52-week high could represent an attractive tactical entry point for investors with a multi-year horizon, particularly if the global defense spending environment remains supportive — which consensus estimates suggest it will. The company’s diversified business across land systems, aeroengines, space, and naval (via Hanwha Ocean) provides resilience against any single program’s underperformance.

However, position sizing is key. The stock is not cheap on traditional metrics, governance risks are real, and the special dividend yield should not be mistaken for sustainable income. International investors should consider Hanwha Aerospace as a growth-oriented defense allocation rather than a yield play, and should be prepared for volatility commensurate with its Korean market listing and geopolitical exposure.

In summary, Hanwha Aerospace represents one of the most compelling defense growth stories in the global equity market today. Its combination of proven export success, next-generation technology investments, and scale in a market where barriers to entry are extraordinarily high makes it a name that serious international investors cannot afford to ignore — even if prudence demands careful entry timing and risk management.

Disclaimer: This blog post is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy or sell any securities. All data is sourced from publicly available market information as of May 5, 2026, and may be subject to change. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions.