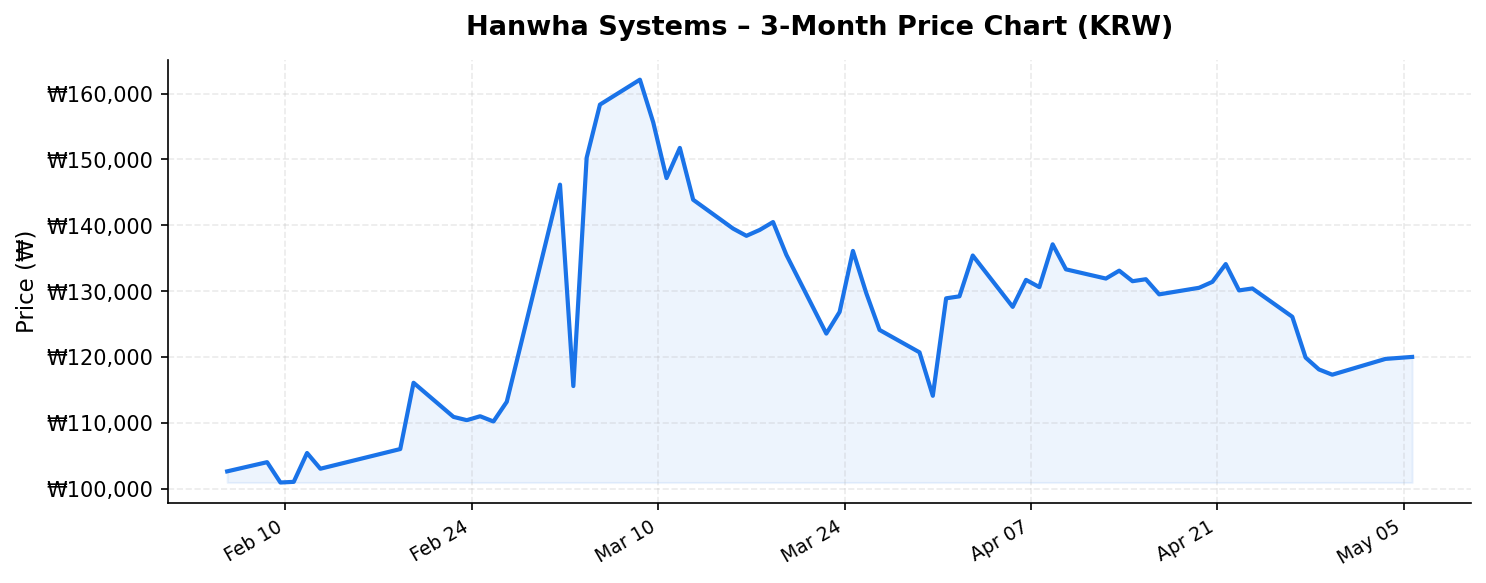

South Korea’s defense and aerospace sector has been one of the most compelling investment stories in Asia over the past several years, driven by geopolitical tensions, surging global defense budgets, and a new wave of technology-driven warfare. At the center of this narrative sits Hanwha Systems (한화시스템, 272210.KS), a subsidiary of the Hanwha Group conglomerate that specializes in defense electronics, ICT solutions, and space systems. As of May 6, 2026, the stock trades at ₩120,100 — roughly 34.7% below its 52-week high of ₩184,000 — raising a critical question for international investors: is this a compelling entry point into one of Korea’s most strategically important defense contractors, or are there fundamental reasons for the pullback?

With a market capitalization of approximately ₩22.5 trillion (roughly $16.5 billion USD), Hanwha Systems is no small player. Its trailing twelve-month revenue stands at ₩3.7 trillion, and the stock currently offers an extraordinary headline dividend yield of 42%. Let’s unpack what’s really going on beneath the surface.

Business Overview: Defense Electronics, Space, and Beyond

Hanwha Systems operates at the intersection of defense technology and next-generation infrastructure. The company’s core business is organized around several key pillars:

- Defense Electronics: This is the company’s bread and butter. Hanwha Systems develops radar systems, electronic warfare (EW) suites, command and control (C4I) systems, naval combat management systems, and avionics. It is a primary supplier to the South Korean military and has been expanding its export footprint aggressively, particularly in the Middle East, Southeast Asia, and Eastern Europe.

- ICT Solutions: The company provides enterprise IT services, cloud computing infrastructure, and smart city solutions, primarily serving the domestic Korean market. While this segment generates steady cash flow, it is the defense and space verticals that drive most investor excitement.

- Space and Satellite Systems: Hanwha Systems has made bold moves into the low-Earth orbit (LEO) satellite constellation business, notably through its investment in OneWeb (now Eutelsat OneWeb) and its own indigenous satellite development programs. The company envisions becoming a key player in satellite-based communications and surveillance.

- Urban Air Mobility (UAM): Through its investment in Overair (formerly known as part of Karem Aircraft), Hanwha Systems has been developing electric vertical takeoff and landing (eVTOL) aircraft, positioning itself for the future of urban transportation.

This diversified portfolio — spanning proven defense platforms and high-growth frontier technologies — gives Hanwha Systems a unique risk-reward profile among Korean defense stocks. The company benefits from the Hanwha Group ecosystem, which includes Hanwha Aerospace (engines and propulsion) and Hanwha Ocean (shipbuilding), creating a vertically integrated defense powerhouse.

Valuation and Market Position: Parsing the Numbers

At ₩120,100 per share with ₩3.7 trillion in TTM revenue and a ₩22.5 trillion market cap, Hanwha Systems trades at a price-to-sales ratio of approximately 6.1x. For a defense electronics company, this is a premium multiple — but it reflects the market’s pricing of the company’s high-growth space and UAM optionality. Comparable global defense electronics firms like L3Harris or Thales typically trade at 2x–3x sales, though they lack the same exposure to satellite and eVTOL megatrends.

The return on equity of 5.4% is modest and signals that profitability has not yet caught up with the company’s ambitious expansion plans. Heavy investment in R&D, satellite infrastructure, and UAM development has compressed margins. International investors should view this as a growth-stage metric rather than a sign of structural inefficiency — but it does mean that the stock is priced more on future expectations than current earnings power.

Now, the elephant in the room: the 42% dividend yield. This figure demands scrutiny. A yield this high on a growth-oriented defense technology company is highly unusual and almost certainly reflects a special dividend or extraordinary capital return event rather than a sustainable recurring payout. Possibilities include a one-time distribution related to asset sales, restructuring within the Hanwha Group, or proceeds from a subsidiary monetization. International investors should not model this yield as recurring. Instead, they should examine the company’s ordinary dividend policy, which historically has been modest (typically yielding well under 1%). Relying on the headline 42% figure without understanding its composition would be a significant analytical error.

The stock’s position within its 52-week range is also telling. Trading at ₩120,100 against a range of ₩40,850 to ₩184,000, the shares are nearly triple their 52-week low but sit a substantial 34.7% below their peak. This suggests the stock experienced a massive rally — likely driven by defense sector enthusiasm and specific catalysts — followed by a meaningful correction. The current price level could represent either a healthy consolidation or the beginning of a longer-term de-rating, depending on whether the company can deliver on its growth promises.

Competitive Position and Growth Catalysts

Hanwha Systems operates in an increasingly favorable macro environment for defense contractors. Global defense spending surpassed $2.4 trillion in 2025, and South Korea has emerged as a top-10 global arms exporter. Several structural tailwinds support the company’s growth trajectory:

- Korean defense export boom: South Korea’s defense exports have exploded in recent years, with major contracts for K2 tanks, K9 howitzers, FA-50 fighter jets, and naval vessels. Hanwha Systems benefits as the electronics and systems integrator behind many of these platforms. Every export contract for a Hanwha Aerospace engine or Hanwha Ocean vessel often includes Hanwha Systems components.

- Geopolitical demand: Heightened tensions on the Korean Peninsula, the ongoing war in Ukraine, and broader NATO rearmament have created a structural increase in demand for radar, electronic warfare, and C4I systems — all core competencies of Hanwha Systems.

- Space economy participation: The global space economy is projected to exceed $1 trillion by 2030. Hanwha Systems’ investments in satellite constellations and ground systems position it to capture a share of this rapidly expanding market, though meaningful revenue contributions likely remain several years away.

- Domestic policy support: The South Korean government has designated defense and aerospace as strategic industries, providing favorable procurement policies, R&D subsidies, and diplomatic support for export campaigns.

Competitively, Hanwha Systems faces limited domestic rivalry in its core defense electronics niche — LIG Nex1 is the primary competitor — but internationally, it competes against well-established players like Raytheon, Northrop Grumman, Thales, and Israel’s Elbit Systems. The company’s competitive advantage lies in its price-to-performance ratio and its integration within the broader Hanwha defense ecosystem, which allows it to offer turnkey solutions.

Key Risks for International Investors

Despite the compelling narrative, several risks warrant careful consideration:

- Profitability lag: With an ROE of just 5.4%, the company is not yet generating returns commensurate with its premium valuation. If the space and UAM bets take longer to materialize — or fail to achieve commercial viability — the stock could face a significant multiple compression.

- Dividend yield misinterpretation: As discussed, the 42% yield is almost certainly non-recurring. Investors who buy the stock for income may be deeply disappointed in subsequent years.

- Geopolitical double-edged sword: While geopolitical tensions drive demand, they also create risks. An unexpected détente on the Korean Peninsula or shifts in U.S. alliance dynamics could reduce defense procurement urgency. Conversely, actual conflict would create enormous uncertainty.

- Currency risk: International investors are exposed to KRW/USD fluctuations. A weakening Korean won would erode returns when converted back to dollars or euros, even if the stock price appreciates in local currency terms.

- Conglomerate governance: As part of the Hanwha Group chaebol structure, minority shareholders face perennial concerns about related-party transactions, capital allocation decisions that favor the group over individual subsidiaries, and limited board independence.

- Execution risk in new verticals: The space and UAM businesses are capital-intensive and technologically demanding. Competition is fierce globally, and the path from investment to profitability is uncertain.

Investment Thesis: Opportunity in the Pullback?

For international investors with a medium-to-long-term horizon and a tolerance for growth-stage volatility, Hanwha Systems presents an intriguing proposition. The 34.7% decline from its 52-week high offers a more attractive entry point than existed at peak euphoria, while the stock’s position nearly 3x above its 52-week low of ₩40,850 confirms sustained investor interest and a meaningful re-rating from previous levels.

The bull case rests on: (1) continued Korean defense export momentum translating into higher revenue and improving margins; (2) successful commercialization of space and satellite capabilities; (3) the strategic value of the Hanwha Group’s integrated defense ecosystem; and (4) a global defense spending super-cycle that shows no signs of abating.

The bear case centers on: (1) a premium valuation not yet supported by profitability; (2) execution risks in capital-intensive new ventures; (3) the misleading headline dividend yield; and (4) governance concerns inherent to Korea’s chaebol structure.

On balance, Hanwha Systems is best understood as a defense-technology growth stock with optionality in space and urban air mobility. The ₩22.5 trillion market cap prices in meaningful future growth, so investors need conviction that the company can execute on its ambitious roadmap. For those who believe in the structural rise of Korean defense exports and the long-term space economy, the current pullback may represent a window worth exploring — but position sizing should reflect the inherent uncertainty embedded in the growth assumptions.

Disclaimer: This blog post is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy or sell any securities. All data referenced is based on publicly available market information as of May 6, 2026. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.