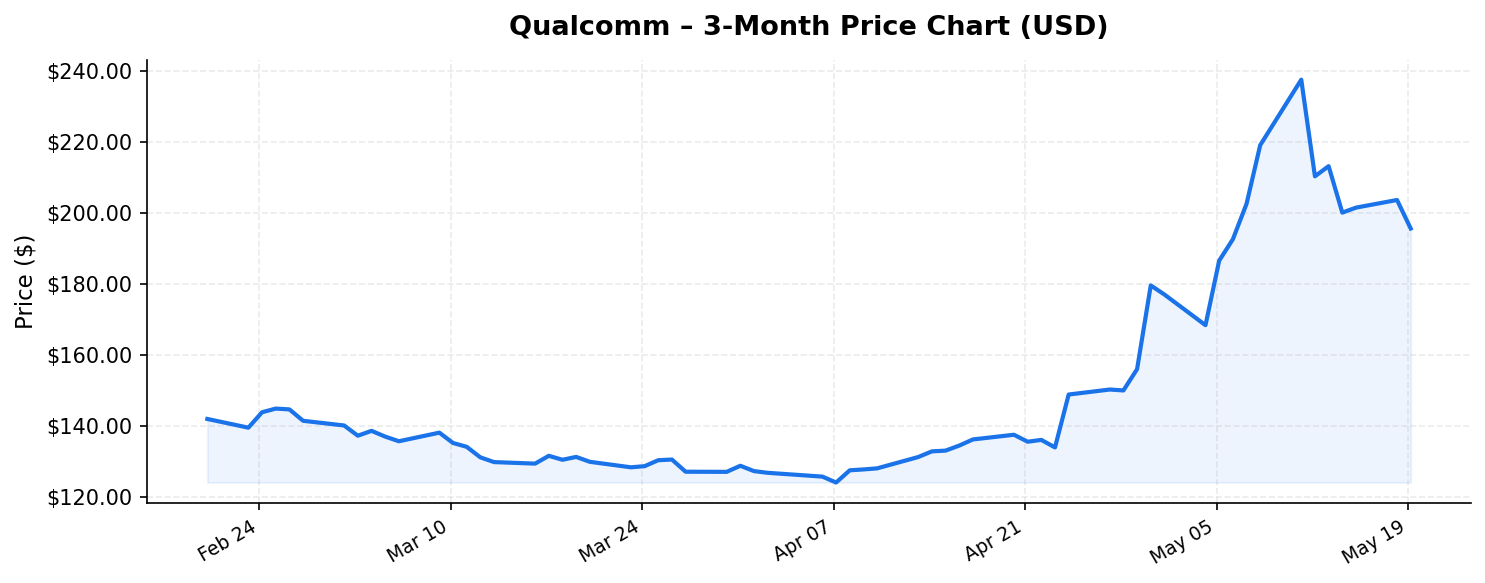

Qualcomm (QCOM) has long been synonymous with mobile connectivity. As the architect behind the wireless technologies that power billions of smartphones worldwide, the San Diego-based semiconductor titan occupies a unique position at the intersection of chip design and intellectual property licensing. Yet as of May 20, 2026, Qualcomm’s stock sits at $195.61 — a full 21.1% below its 52-week high of $247.90 — raising a critical question for international investors: does this pullback represent a compelling entry point, or a signal of deeper structural challenges ahead?

With a market capitalization of $206.2 billion, trailing twelve-month revenue of $44.5 billion, and a return on equity of 36.1%, the numbers paint a picture of a highly profitable business. But the story behind those numbers — one of diversification ambitions, geopolitical headwinds, and an evolving competitive landscape — demands closer scrutiny. Let’s break it down.

Business Overview: More Than Just a Smartphone Chip Company

Qualcomm operates through three primary segments: QCT (Qualcomm CDMA Technologies), QTL (Qualcomm Technology Licensing), and QSI (Qualcomm Strategic Initiatives). QCT is the hardware engine, designing and selling the Snapdragon system-on-chip (SoC) processors that power the majority of the world’s Android smartphones. QTL is the licensing powerhouse, monetizing Qualcomm’s vast portfolio of wireless patents — including foundational 3G, 4G, and 5G technologies — by collecting royalties from virtually every handset manufacturer on the planet.

This dual-engine model is what makes Qualcomm distinctive. While QCT competes directly with MediaTek, Samsung LSI, and increasingly Apple’s in-house silicon efforts, QTL functions as a near-monopoly toll booth on global wireless communications. The licensing segment consistently delivers operating margins above 70%, providing a cushion that few semiconductor peers can match.

In recent years, Qualcomm has aggressively pursued diversification beyond smartphones. Its automotive pipeline — fueled by the Snapdragon Digital Chassis platform — has grown into a multi-billion dollar revenue stream, with design win pipelines reportedly exceeding $45 billion. The company has also pushed into IoT (Internet of Things), industrial applications, PC processors (competing with Intel and AMD in the Windows-on-ARM space), and edge AI computing. This diversification is critical as the global smartphone market matures and Qualcomm’s largest customer, Apple, continues developing its own modem chips to replace Qualcomm’s.

Valuation and Financial Health: Attractive Metrics With Important Caveats

At a P/E ratio of 21.1x, Qualcomm trades at a meaningful discount to the broader semiconductor sector, where premium names like NVIDIA routinely command multiples north of 30-40x. This valuation reflects both the market’s concerns about smartphone cyclicality and the overhang of Apple’s eventual modem transition. However, for value-conscious international investors, 21.1x earnings for a company generating $44.5 billion in annual revenue and a 36.1% return on equity is difficult to ignore.

The P/B ratio of 7.59x is elevated relative to value benchmarks but is typical for asset-light semiconductor design companies whose primary value resides in intellectual property rather than physical plant. What truly stands out is Qualcomm’s capital efficiency: a 36.1% ROE signals that management is generating exceptional returns on shareholder capital, well above the 15-20% range that many investors consider the threshold for a high-quality business.

Now, the dividend yield figure of 188% listed in market data requires important context. This extraordinarily high yield almost certainly reflects a special dividend, significant capital return event, or a data anomaly rather than a sustainable ordinary payout. Qualcomm has historically been a reliable dividend payer, with a track record of consistent increases over two decades. Its regular quarterly dividend has typically yielded in the 1.5-2.5% range. International investors should investigate the underlying cause of this figure carefully — it could indicate a transformative capital allocation decision such as a massive special distribution funded by repatriated cash or asset sales, but it should not be extrapolated as a recurring yield without confirmation.

The stock’s current price of $195.61 sits roughly 60% above its 52-week low of $121.99, suggesting that while the shares have recovered significantly from their trough, there remains substantial ground to reclaim before retesting the $247.90 high. This positioning — solidly in the middle of the 52-week range but skewing toward the upper half — suggests the market has priced in a recovery from whatever drove the lows but remains unconvinced about a return to peak optimism.

Competitive Landscape and Key Risks for International Investors

Qualcomm faces a multi-front competitive war that international investors must carefully weigh:

- Apple’s modem ambitions: Apple has been developing its own 5G modem to replace Qualcomm’s components in iPhones. Apple represents a significant revenue stream for QCT, and every percentage of iPhone modem share that transitions in-house represents hundreds of millions in lost revenue. While Apple’s timeline has reportedly faced delays, the direction of travel is clear. Qualcomm has been preparing for this eventuality by diversifying, but the transition period creates uncertainty.

- MediaTek’s ascent: Taiwan-based MediaTek has steadily gained share in mid-range and increasingly premium smartphone SoCs, particularly in China and emerging markets. With competitive 5G offerings at lower price points, MediaTek pressures Qualcomm’s volume business and forces pricing discipline.

- Geopolitical risk: As a U.S.-headquartered company with massive exposure to Chinese OEMs (Xiaomi, Oppo, Vivo, Honor), Qualcomm is acutely vulnerable to U.S.-China trade tensions, export controls, and potential sanctions. Chinese handset makers account for a substantial portion of both QCT chip sales and QTL licensing revenue. Any escalation in technology restrictions could materially impact Qualcomm’s top line. For international investors — particularly those based in Asia or Europe — this geopolitical dimension adds a layer of macro risk that transcends company fundamentals.

- Licensing disputes: QTL’s licensing model, while enormously profitable, has historically attracted regulatory scrutiny and legal challenges from governments in China, South Korea, the EU, and the United States. While Qualcomm has successfully defended its model in most jurisdictions, ongoing or future challenges could erode licensing margins or force renegotiations.

- Cyclicality: The semiconductor industry remains inherently cyclical. Qualcomm’s revenue is tied to smartphone sell-through volumes, which are influenced by consumer spending, carrier upgrade cycles, and macroeconomic conditions. A global economic slowdown would directly impact handset sales and, consequently, Qualcomm’s earnings.

Investment Thesis: Why International Investors Should Pay Attention

For international investors seeking exposure to the global 5G rollout, the AI-at-the-edge revolution, and automotive digitization, Qualcomm presents a differentiated opportunity. Here’s the bull case:

Diversification is gaining traction. Qualcomm’s automotive, IoT, and PC businesses are no longer speculative — they are contributing meaningful and growing revenue. The automotive segment alone provides a long-duration growth vector as vehicles become increasingly software-defined. If Qualcomm can grow non-handset revenue to 50%+ of QCT sales over the next few years, the Apple modem risk becomes far more manageable and the earnings multiple could re-rate higher.

AI at the edge is a secular tailwind. While much of the AI investment narrative has centered on cloud/data center chips (benefiting NVIDIA and AMD), Qualcomm is positioning itself as the leader in on-device AI processing. Snapdragon processors with integrated neural processing units (NPUs) are enabling generative AI capabilities directly on smartphones, PCs, and automobiles — without relying on cloud connectivity. This is particularly relevant in markets with limited bandwidth infrastructure, making Qualcomm’s edge AI proposition attractive in emerging economies across Asia, Africa, and Latin America.

The valuation provides a margin of safety. At 21.1x earnings with a 36.1% ROE and $44.5 billion in revenue, Qualcomm is not priced for perfection. The 21% discount to the 52-week high gives international investors room for error — and potential upside if the diversification thesis plays out or if geopolitical tensions ease. Compared to semiconductor peers trading at significantly higher multiples, Qualcomm offers a rare combination of profitability, scale, and relative value.

Currency and market access considerations. For non-U.S. investors, Qualcomm’s global revenue base — with significant exposure to Asia and Europe — provides a natural hedge against purely domestic U.S. economic conditions. The stock trades on NASDAQ with deep liquidity, making it accessible through most international brokerage platforms and ADR structures.

The bear case, however, is equally real: Apple’s eventual modem independence, intensifying competition from MediaTek, and geopolitical disruption to the China revenue stream could collectively compress earnings and justify a lower multiple. The unusual dividend yield figure also warrants investigation, as it may signal a one-time event rather than sustainable income.

Conclusion

Qualcomm stands at a pivotal moment. The company’s legacy smartphone business faces genuine headwinds, but its diversification into automotive, AI, IoT, and computing is transforming it into a broader platform technology company. At $195.61 per share, with a market cap of $206.2 billion and robust profitability metrics, the stock offers international investors a compelling risk-reward profile — provided they are comfortable with the geopolitical and competitive risks embedded in the story.

For long-term investors willing to look beyond near-term smartphone cyclicality and focus on the secular trends powering Qualcomm’s next chapter, the current 21% discount to the 52-week high may prove to be an attractive entry point. But as always, thorough due diligence — particularly around the dividend data and Apple modem timeline — is essential before committing capital.

Disclaimer: This blog post is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or an endorsement to buy or sell any securities. Market data is as of May 20, 2026, and may change. Always conduct your own research and consult a qualified financial advisor before making investment decisions.