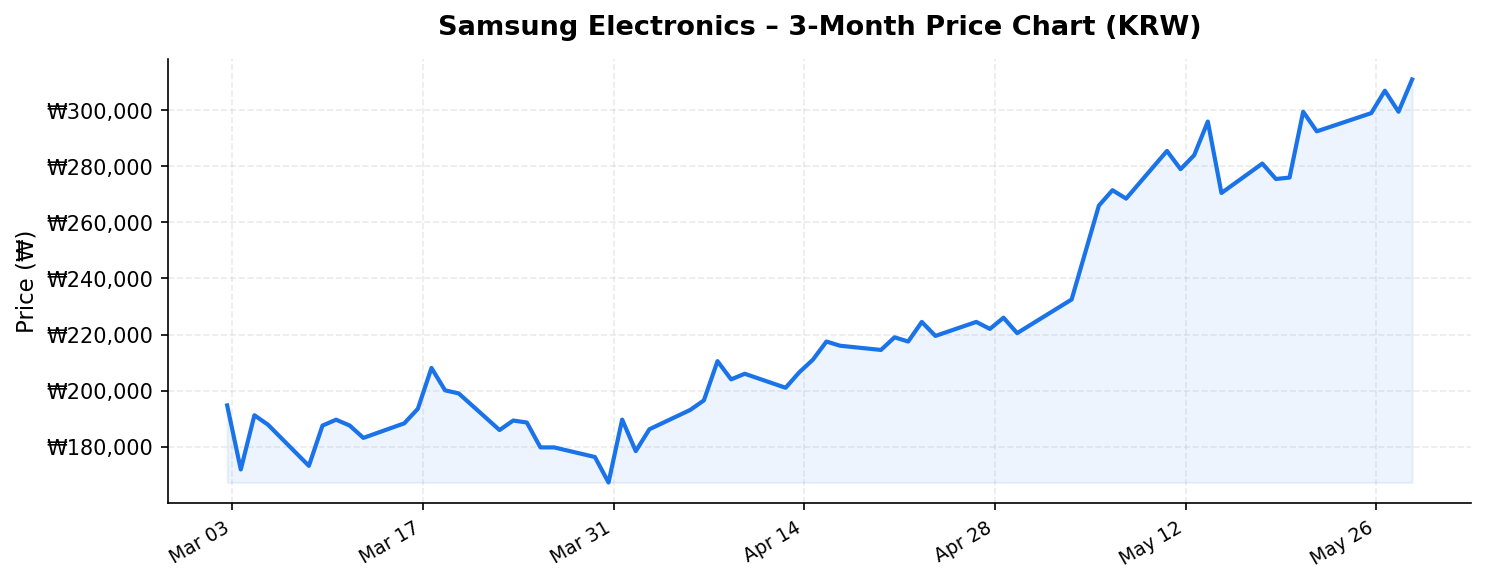

Samsung Electronics (삼성전자, 005930.KS) needs little introduction. As South Korea’s largest company and one of the world’s most dominant technology conglomerates, Samsung sits at the nexus of semiconductors, consumer electronics, and display technology. With a staggering market capitalization of ₩2,042.2 trillion (approximately $1.5 trillion USD), it ranks among the most valuable companies on the planet. But for international investors evaluating an entry point in late May 2026, the critical question remains: does the current price of ₩311,000 per share represent compelling value, or has the market already priced in the company’s formidable strengths?

Trading just 3.7% below its 52-week high of ₩323,000 — and remarkably, more than 450% above its 52-week low of ₩55,800 — Samsung Electronics presents a fascinating case study in momentum, valuation, and structural positioning in the AI-driven semiconductor supercycle. Let’s break down the numbers.

Business Overview: A Diversified Technology Empire

Samsung Electronics operates across four primary business divisions: the Device Solutions (DS) division, which encompasses its semiconductor and display panel businesses; the Device eXperience (DX) division, covering mobile devices, TVs, and home appliances; the Harman subsidiary focused on connected car and audio solutions; and its foundry services business. This diversification has historically been both a strength and a source of frustration for investors seeking a pure-play semiconductor exposure.

However, the semiconductor segment — particularly DRAM, NAND flash memory, and increasingly, high-bandwidth memory (HBM) for AI applications — has reasserted itself as the dominant earnings driver. The company’s trailing twelve-month revenue of ₩388.3 trillion reflects robust demand across its product portfolio, but it is the memory and logic chip businesses that have been the primary catalysts behind the stock’s dramatic ascent from the ₩55,800 low.

Samsung’s return on equity of 18.9% signals that management is effectively deploying shareholder capital to generate profits. This figure represents a significant recovery from the cyclical trough the company experienced during the memory downturn and positions Samsung favorably relative to many global large-cap technology peers. For context, an ROE approaching 19% in a capital-intensive semiconductor business demonstrates both pricing power and operational discipline.

Competitive Position: Navigating the AI Semiconductor Arms Race

Samsung Electronics occupies a unique competitive position in the global technology landscape. In memory semiconductors, it competes primarily with SK Hynix and Micron Technology. In foundry services, it faces the formidable challenge of competing with TSMC. In consumer electronics, it battles Apple, Xiaomi, and a constellation of Chinese manufacturers.

The AI revolution has fundamentally reshaped the competitive dynamics of the memory market. High-bandwidth memory — the specialized DRAM stacked vertically to feed the insatiable data appetites of AI accelerators — has become the most strategically important product in the semiconductor industry. Samsung initially ceded ground to SK Hynix in the HBM race but has made significant strides in qualifying its latest-generation HBM products with major customers including NVIDIA and AMD. Any acceleration in Samsung’s HBM market share gains could serve as a meaningful upside catalyst from current levels.

On the foundry side, Samsung has been investing heavily in advanced process nodes, including its gate-all-around (GAA) transistor architecture at 2nm and below. While TSMC remains the clear leader with over 60% market share in advanced logic, Samsung’s position as the only credible alternative gives it strategic importance to customers seeking supply chain diversification — a theme that has only intensified amid geopolitical tensions between the US and China.

- Memory (DRAM/NAND): Global market leader with ~40% DRAM market share; rapidly closing the HBM gap with SK Hynix

- Foundry: Distant second to TSMC but benefiting from customer diversification mandates

- Mobile: The world’s largest smartphone manufacturer by volume, with the premium Galaxy S series competing directly with Apple’s iPhone

- Displays: Dominant in OLED panels for smartphones and expanding into large-format OLED for TVs and IT applications

Dividend Yield and Valuation: Unpacking the Numbers

Perhaps the most eye-catching figure in Samsung’s current market data is the reported dividend yield of 50.00%. This extraordinary number warrants careful scrutiny from international investors. Such a yield, if taken at face value, would be virtually unprecedented for a mega-cap technology company. This figure likely reflects a special dividend, a significant capital return program, or a structural change in Samsung’s shareholder return policy that dramatically increased payouts. International investors should verify the composition of this yield — specifically, what portion represents recurring ordinary dividends versus one-time special distributions.

If Samsung has indeed committed to returning capital at this scale, it would represent a paradigm shift in Korean corporate governance. South Korean companies have historically traded at a “Korea discount” partly due to perceived poor shareholder returns. A sustained commitment to extraordinary capital returns would directly address this discount and could attract significant flows from global income-oriented and value investors. This may, in fact, explain a portion of the stock’s remarkable rise from ₩55,800 to its current level near ₩311,000.

At a market cap of ₩2,042.2 trillion against TTM revenue of ₩388.3 trillion, Samsung trades at a price-to-sales ratio of approximately 5.3x. For a diversified technology conglomerate with significant hardware businesses, this is a premium valuation that suggests the market is pricing in continued earnings growth — likely driven by the AI memory supercycle and potentially improved margins in the foundry business. The 18.9% ROE supports the argument that this premium is at least partially justified by the quality of earnings generation.

The stock’s proximity to its 52-week high — just 3.7% below ₩323,000 — indicates strong bullish momentum. However, the vast distance from the 52-week low of ₩55,800 suggests that investors entering at current levels are buying into a stock that has already experienced a massive re-rating. The risk-reward calculus is fundamentally different at ₩311,000 than it was at ₩55,800.

Key Risks for International Investors

Despite Samsung Electronics’ formidable market position, several material risks deserve consideration:

- Memory Cycle Risk: The semiconductor memory business remains inherently cyclical. While the AI-driven demand cycle appears structural, any slowdown in data center capital expenditure by hyperscalers could trigger a sharp correction in memory pricing and Samsung’s earnings.

- HBM Execution Risk: Samsung’s ability to close the gap with SK Hynix in HBM yields and customer qualifications remains uncertain. Continued HBM share losses could weigh on the stock’s premium valuation.

- Foundry Competitiveness: Persistent yield issues at advanced nodes could result in Samsung losing foundry customers to TSMC, undermining the long-term growth narrative for this division.

- Geopolitical Risk: Samsung’s global manufacturing footprint — spanning South Korea, Vietnam, the United States, and China — exposes it to trade tensions, export controls, and regulatory fragmentation. The company’s significant operations in China represent a particular vulnerability amid US-China technology restrictions.

- Currency Risk: International investors face Korean won (KRW) exposure. Fluctuations in the KRW/USD or KRW/EUR exchange rate can materially impact dollar- or euro-denominated returns, independent of the stock’s performance in local currency.

- Valuation Risk: At just 3.7% below its 52-week high, the stock offers limited margin of safety. Any earnings disappointment or negative macro development could trigger a meaningful pullback from these elevated levels.

Investment Thesis: Should International Investors Buy Samsung Electronics at ₩311,000?

Samsung Electronics presents a compelling but nuanced investment case at current levels. On the bull side, the company is a structurally advantaged participant in the AI semiconductor revolution, with leading positions in memory, displays, and mobile devices. The extraordinary dividend yield — if sustainable — would make it one of the most attractive income-generating large-cap technology stocks globally. An 18.9% ROE confirms efficient capital allocation, and the ongoing dissolution of the Korea discount through improved corporate governance could provide additional re-rating tailwinds.

On the bear side, the stock’s proximity to all-time highs, the premium price-to-sales multiple of 5.3x, and the inherent cyclicality of the memory business create meaningful downside risk. International investors should also carefully evaluate the sustainability of the 50% dividend yield before treating it as a reliable income stream.

For long-term investors with a 3-5 year horizon who believe in the structural growth of AI infrastructure, Samsung Electronics remains one of the highest-quality ways to gain exposure to the semiconductor value chain through a Korean-listed equity. However, prudent position sizing and an awareness of the cyclical risks are essential at ₩311,000. A phased entry strategy — rather than a single lump-sum investment — may be appropriate given the stock’s elevated position relative to its recent trading range.

Disclaimer: This blog post is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy or sell any securities. The data presented reflects market information as of May 29, 2026, and may not be current at the time of reading. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. Investing in foreign securities involves additional risks, including currency risk and regulatory differences.