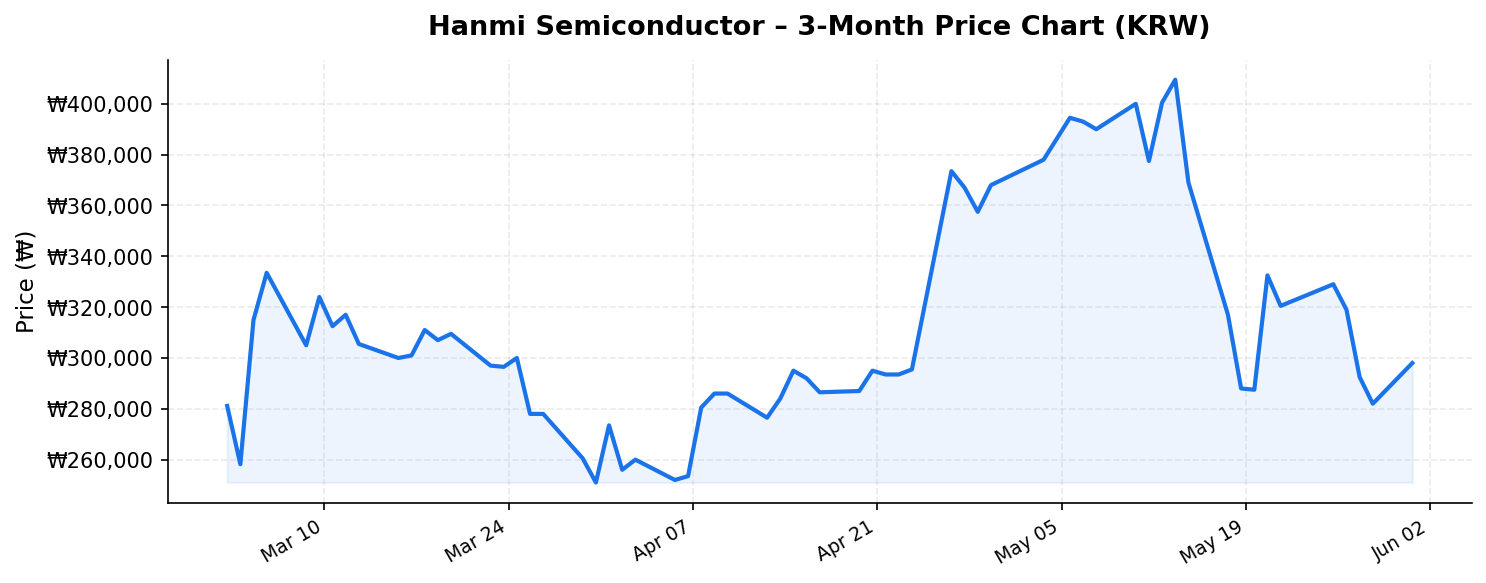

In the global race to build the infrastructure powering artificial intelligence, much of the investor spotlight has fallen on chip designers like NVIDIA and foundries like TSMC. But behind every advanced AI chip lies a critical and often overlooked step: semiconductor packaging. This is where Hanmi Semiconductor (한미반도체, 042700.KS) has carved out a dominant niche. Trading at ₩298,500 as of June 1, 2026, with a market capitalization of ₩28.3 trillion (approximately $21 billion), Hanmi Semiconductor has transformed from a mid-cap Korean industrial player into a global beneficiary of the AI megatrend. Yet with the stock sitting nearly 30% below its 52-week high, international investors are asking: is this a compelling entry point, or a sign of fading momentum?

Business Overview: The Backbone of Advanced Chip Packaging

Hanmi Semiconductor is the world’s leading manufacturer of semiconductor packaging equipment, specializing in vision placement systems, trim and form machines, and — most critically — thermocompression bonding (TCB) equipment used in high-bandwidth memory (HBM) production. HBM chips are the essential memory components stacked vertically and bonded to AI processors, enabling the massive data throughput required by large language models and generative AI workloads.

The company’s dominance in TCB equipment has made it an indispensable supplier to memory giants SK hynix and Samsung Electronics, both of which are locked in fierce competition to supply HBM chips to NVIDIA, AMD, and other AI accelerator makers. As HBM generations advance — from HBM3E to HBM4 and beyond — the number of stacked layers increases, and each additional layer requires more bonding passes, directly translating into higher equipment demand for Hanmi Semiconductor’s core products.

The financial results reflect this structural tailwind. Trailing twelve-month (TTM) revenue stands at ₩4,802 billion (approximately $3.6 billion), a figure that would have seemed inconceivable just a few years ago when the company was generating a fraction of that amount. Return on equity of 30.8% signals exceptional capital efficiency, indicating that management is converting shareholder capital into profits at a rate that rivals many best-in-class technology companies globally.

Valuation and Market Position: Opportunity in the Pullback?

Hanmi Semiconductor’s current price of ₩298,500 places it 29.9% below its 52-week high of ₩426,000 — a meaningful correction that warrants examination. At the same time, the stock has appreciated dramatically from its 52-week low of ₩79,800, meaning investors who entered near the bottom have seen roughly a 274% return. This wide 52-week range (₩79,800 to ₩426,000) speaks to the stock’s volatility, which is characteristic of equipment companies with cyclical order patterns superimposed on a secular growth trend.

The pullback from highs likely reflects a combination of factors: profit-taking after an extraordinary run, concerns about the sustainability of HBM investment cycles, and broader market rotation away from AI-adjacent names in early 2026. For international investors, however, the critical question is whether the underlying demand thesis remains intact — and by most measures, it does. Capital expenditure plans from SK hynix and Samsung for HBM expansion remain robust, and NVIDIA’s next-generation Rubin platform is expected to require even more HBM capacity.

Perhaps the most eye-catching figure in Hanmi Semiconductor’s profile is its dividend yield of 28.00%. This extraordinary yield demands careful interpretation. A yield this high could indicate a special dividend or a significant payout increase reflecting management’s confidence in cash flow sustainability. It could also result from a one-time extraordinary distribution. International investors should verify the composition of this dividend — whether it is recurring or includes special components — before treating it as a reliable income stream. That said, even if partially normalized, a yield of this magnitude suggests the company is generating far more cash than it needs to reinvest, which is a hallmark of a capex-light equipment business operating at peak demand.

At a market cap of ₩28.3 trillion relative to TTM revenue of ₩4,802 billion, Hanmi Semiconductor trades at a price-to-sales ratio of approximately 5.9x. For a high-growth equipment company with 30%+ ROE and exposure to the fastest-growing segment of the semiconductor industry, this valuation is not stretched by global standards — particularly when compared to peers like Disco Corporation in Japan or Applied Materials in the United States.

Competitive Advantages and Moats

Hanmi Semiconductor’s competitive position rests on several reinforcing advantages:

- Technological leadership in TCB: The company’s thermocompression bonding equipment is considered best-in-class for HBM production. Switching costs are high because memory manufacturers must qualify equipment through rigorous testing before deploying it in production lines. Once qualified, customers are reluctant to change suppliers mid-cycle.

- Customer concentration as a double-edged sword: SK hynix, which holds the dominant share of HBM supply to NVIDIA, is Hanmi Semiconductor’s largest customer. This relationship provides revenue visibility but also creates dependency risk. However, Samsung’s aggressive push into HBM provides a diversification path.

- Secular demand trajectory: Unlike many equipment companies that face boom-bust cycles, Hanmi Semiconductor benefits from a structural increase in bonding steps per chip generation. HBM4, expected to feature 16 or more stacked layers, requires significantly more TCB passes than HBM3E’s 8-12 layers. This means equipment demand grows even if the number of chips produced remains flat.

- Operational efficiency: An ROE of 30.8% places Hanmi Semiconductor in elite territory. The company operates with relatively low capital intensity compared to the chipmakers it serves, enabling strong free cash flow generation and the ability to return capital to shareholders — as evidenced by the remarkable dividend yield.

It’s also worth noting that Hanmi Semiconductor has been expanding its product portfolio beyond traditional packaging into areas like panel-level packaging and advanced hybrid bonding, positioning itself for the next wave of packaging innovation beyond TCB.

Key Risks for International Investors

No investment thesis is without risks, and Hanmi Semiconductor presents several that international investors should carefully weigh:

- Customer concentration: Heavy reliance on a small number of memory manufacturers means that a slowdown in orders from SK hynix or Samsung — whether due to inventory corrections, demand normalization, or competitive dynamics — could materially impact revenue.

- Cyclicality: Despite the secular growth narrative, semiconductor equipment demand is inherently cyclical. If AI infrastructure spending decelerates or if hyperscalers reduce capex plans, Hanmi Semiconductor’s order book could contract rapidly. The stock’s wide 52-week range (from ₩79,800 to ₩426,000) is a vivid reminder of this volatility.

- Emerging competition: While Hanmi Semiconductor currently dominates TCB equipment, competitors in Japan (such as Shinkawa) and domestically in Korea are investing in rival technologies. Additionally, as hybrid bonding emerges as a potential successor to TCB for certain applications, the company must continue to innovate or risk disruption.

- Currency and geopolitical risks: As a Korean-listed company earning revenue primarily in Korean won and U.S. dollars, international investors face currency translation risk. Additionally, U.S.-China tensions and potential export restrictions on advanced semiconductor equipment could create regulatory uncertainties.

- Dividend sustainability: A 28% dividend yield is extraordinary and may not be sustainable at this level. Investors should model scenarios where the payout reverts to more normalized levels to avoid overestimating total return potential.

Investment Thesis: Why International Investors Should Pay Attention

Hanmi Semiconductor represents a rare combination in global equity markets: a dominant player in a critical technology niche, generating exceptional returns on equity, trading at a meaningful discount to its recent highs, and offering an outsized — if potentially unsustainable — dividend yield. The company sits at the intersection of two powerful forces: the insatiable demand for AI compute and the increasing complexity of advanced semiconductor packaging.

For international investors with a medium- to long-term horizon, the 30% pullback from the 52-week high could represent an attractive risk-reward entry point, provided one accepts the inherent volatility of a concentrated equipment play. The TTM revenue of ₩4,802 billion and ROE of 30.8% demonstrate that this is not a speculative story — it is a profitable, growing business with tangible financial results.

However, position sizing matters. Given the stock’s demonstrated ability to swing from ₩79,800 to ₩426,000 within a single year, risk management is essential. International investors should also consider the liquidity profile of the Korean market, potential withholding taxes on dividends for foreign holders, and the mechanics of accessing the KRX through international brokerages or ETFs with exposure to Korean semiconductor equipment names.

In the architecture of the AI revolution, Hanmi Semiconductor is a foundational pillar. Whether the current price represents fair value, a bargain, or still a premium depends on your assumptions about the duration and intensity of the AI infrastructure buildout. What is less debatable is that the company has earned its place on any serious international investor’s watchlist.

Disclaimer: This blog post is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or an offer to buy or sell securities. All data referenced is based on publicly available information as of June 1, 2026, and may be subject to change. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions.