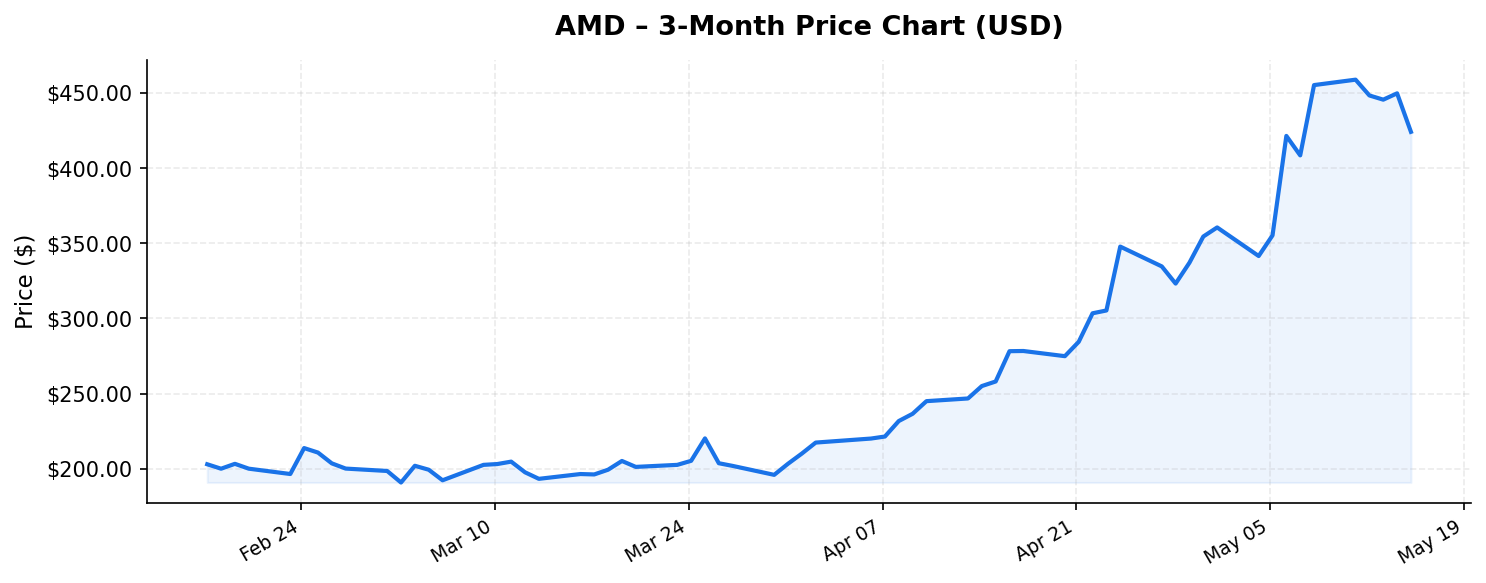

AMD (AMD) has been one of the most remarkable stories in the semiconductor industry over the past several years, transforming from a perennial underdog into a formidable challenger across data center, AI, and high-performance computing markets. Trading at $424.10 as of May 17, 2026, the stock has surged nearly 294% from its 52-week low of $107.67, commanding a market capitalization of $691.5 billion. But with a price-to-earnings ratio of 140.9x and a return on equity of just 8.1%, the critical question for international investors is whether AMD’s growth trajectory can justify its lofty valuation — or whether the market has already priced in years of optimism.

From Underdog to AI Powerhouse: AMD’s Business Overview

AMD designs and sells semiconductors across four key segments: Data Center, Client (PCs), Gaming, and Embedded. Under CEO Lisa Su’s leadership since 2014, the company has executed one of the most impressive corporate turnarounds in tech history. The acquisition of Xilinx in 2022 expanded AMD’s reach into adaptive computing and embedded markets, while organic R&D investments have produced increasingly competitive products across every segment.

The company’s trailing twelve-month revenue stands at $37.5 billion, a figure that reflects the explosive growth in its data center business driven by AI accelerator demand. AMD’s MI300 and subsequent MI400 series GPUs have carved out meaningful market share in the AI training and inference markets, positioning the company as the primary alternative to NVIDIA in a market projected to be worth hundreds of billions of dollars annually by the end of the decade.

AMD’s Zen-based EPYC server CPUs continue to gain share against Intel in the traditional data center CPU market, while its Ryzen processors maintain a strong position in the consumer and commercial PC segments. The diversification across CPUs, GPUs, FPGAs, and adaptive SoCs gives AMD multiple growth vectors — a structural advantage that few semiconductor companies can match.

Valuation Deep Dive: What the Numbers Tell International Investors

Let’s address the elephant in the room: AMD’s valuation metrics are demanding by almost any standard. At 140.9x trailing earnings, the stock is priced for exceptional future growth. The price-to-book ratio of 10.72x further underscores the premium the market assigns to AMD’s intangible assets — its IP portfolio, engineering talent, and market positioning.

For context, a P/E of 141x implies that at current earnings levels, it would take 141 years to recoup your investment through profits alone. Obviously, no investor is making that calculation literally; the bet is that earnings will grow dramatically. With TTM revenue of $37.5 billion, AMD would need to significantly expand both its top line and margins to grow into its valuation within a reasonable timeframe.

The return on equity of 8.1% is notably modest for a company commanding a $691.5 billion market cap. This figure is partly distorted by the substantial goodwill on AMD’s balance sheet from the Xilinx acquisition, which inflates the equity base. As AI-related revenues scale — typically at higher gross margins than AMD’s legacy businesses — ROE should improve meaningfully. However, international investors should monitor this metric closely as a gauge of capital efficiency.

At $424.10, AMD sits roughly 9.6% below its 52-week high of $469.22. This pullback from the peak could represent either a healthy consolidation after a massive run or the beginning of a more significant correction if growth expectations are not met. The stock’s distance from its 52-week low of $107.67 — nearly a 4x move — illustrates the extraordinary momentum that has characterized AMD shares, largely driven by AI enthusiasm.

For international investors, particularly those in markets with weaker currencies against the US dollar, the high absolute price and valuation introduce additional currency risk. A position in AMD at these levels is not just a bet on the company’s fundamentals but also on the dollar remaining stable or strengthening.

Competitive Positioning and the AI Arms Race

AMD’s competitive landscape is both its greatest opportunity and its most significant challenge. In the AI accelerator market, NVIDIA remains the dominant force with its CUDA software ecosystem creating significant switching costs. However, AMD has made meaningful progress with its ROCm software stack and has secured high-profile customers among hyperscale cloud providers eager to diversify their supply chains away from single-vendor dependence.

Several factors work in AMD’s favor in the competitive arena:

- Customer demand for alternatives: Major cloud providers including Microsoft, Google, and Meta have publicly expressed interest in multi-sourcing their AI silicon. AMD is the most credible alternative GPU supplier, and this structural tailwind is unlikely to fade.

- Advanced packaging and chiplet architecture: AMD’s pioneering use of chiplet design and advanced packaging technologies allows it to deliver competitive performance while managing manufacturing costs. Its close partnership with TSMC for leading-edge nodes gives it access to the world’s best manufacturing capabilities.

- Full-stack data center portfolio: Unlike pure-play AI chip startups, AMD offers CPUs, GPUs, FPGAs, and DPUs — enabling integrated solutions that simplify procurement and system design for enterprise customers.

- Embedded and edge AI: The Xilinx-derived product lines position AMD in the growing adaptive computing and edge AI markets, areas where custom silicon solutions command premium pricing.

However, competition is intensifying from multiple directions. NVIDIA continues to innovate at a blistering pace. Intel is investing heavily in its Gaudi AI accelerator line and foundry services. Perhaps most importantly, major customers like Google (TPUs), Amazon (Trainium/Inferentia), and Microsoft (Maia) are developing custom AI chips in-house, which could limit AMD’s addressable market over time.

Key Risks for International Investors

Investing in AMD at current levels carries several material risks that international investors must carefully evaluate:

- Valuation compression risk: At 140.9x earnings, any disappointment in revenue growth, margin expansion, or AI market development could trigger a sharp selloff. High-multiple stocks are disproportionately punished when narratives shift, and AMD’s price assumes near-flawless execution over multiple years.

- Geopolitical and export control risks: The US semiconductor export restrictions targeting China directly impact AMD’s addressable market. As an international investor, you should be aware that further tightening of these controls could materially affect AMD’s revenue, particularly in its data center segment where China represented a meaningful portion of sales.

- Cyclicality: Despite the secular AI growth narrative, the semiconductor industry remains inherently cyclical. PC and gaming markets have experienced boom-bust cycles historically, and even data center spending can fluctuate based on macroeconomic conditions and capital expenditure cycles among hyperscalers.

- Execution risk in software ecosystem: AMD’s ability to close the gap with NVIDIA’s CUDA ecosystem is critical. While ROCm has improved significantly, developer mindshare and software library breadth remain areas where AMD trails. Failure to achieve software parity could cap AMD’s AI GPU market share regardless of hardware competitiveness.

- Currency and tax considerations: For non-US investors, AMD pays no meaningful dividend, meaning returns are entirely dependent on capital appreciation — which is fully exposed to USD exchange rate fluctuations. Withholding tax considerations on any future dividends would also vary by jurisdiction and applicable tax treaties.

Investment Thesis: Where Does AMD Go From Here?

The bull case for AMD is compelling: the company is positioned at the intersection of multiple secular growth trends — AI, cloud computing, high-performance computing, and adaptive silicon. Its $37.5 billion revenue base is expected to grow substantially as AI infrastructure buildout continues globally. If AMD can capture even 20-25% of the AI accelerator market while maintaining its trajectory in server CPUs, revenue could potentially double or more within the next three to four years, with significant margin expansion as higher-margin data center revenues become a larger share of the mix.

The bear case is equally straightforward: at $424.10 and 140.9x earnings, an enormous amount of future success is already reflected in the stock price. The 9.6% decline from the 52-week high may signal that the market is beginning to question whether growth can match expectations. If AI spending moderates, competition intensifies, or macroeconomic conditions tighten, AMD’s valuation multiple could contract sharply even if the underlying business continues to perform well.

For international investors with a long-term horizon and tolerance for volatility, AMD represents exposure to one of the defining technological shifts of our era through a company with proven execution capabilities and a visionary leadership team. However, position sizing is critical at these valuations. A modest allocation that accounts for the high-beta nature of the stock and the currency exposure may be more prudent than a concentrated bet.

Investors who missed the run from $107 to $424 should resist the temptation to chase the stock. Instead, consider building a position gradually, potentially using pullbacks toward the lower end of recent trading ranges to add shares. The stock’s wide 52-week range — from $107.67 to $469.22 — demonstrates that significant volatility is normal for AMD, and patience can be rewarded.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or an endorsement of any security. Stock investing involves risk, including the potential loss of principal. International investors should consult with a qualified financial advisor in their jurisdiction before making any investment decisions. All data referenced is as of May 17, 2026, and is subject to change.