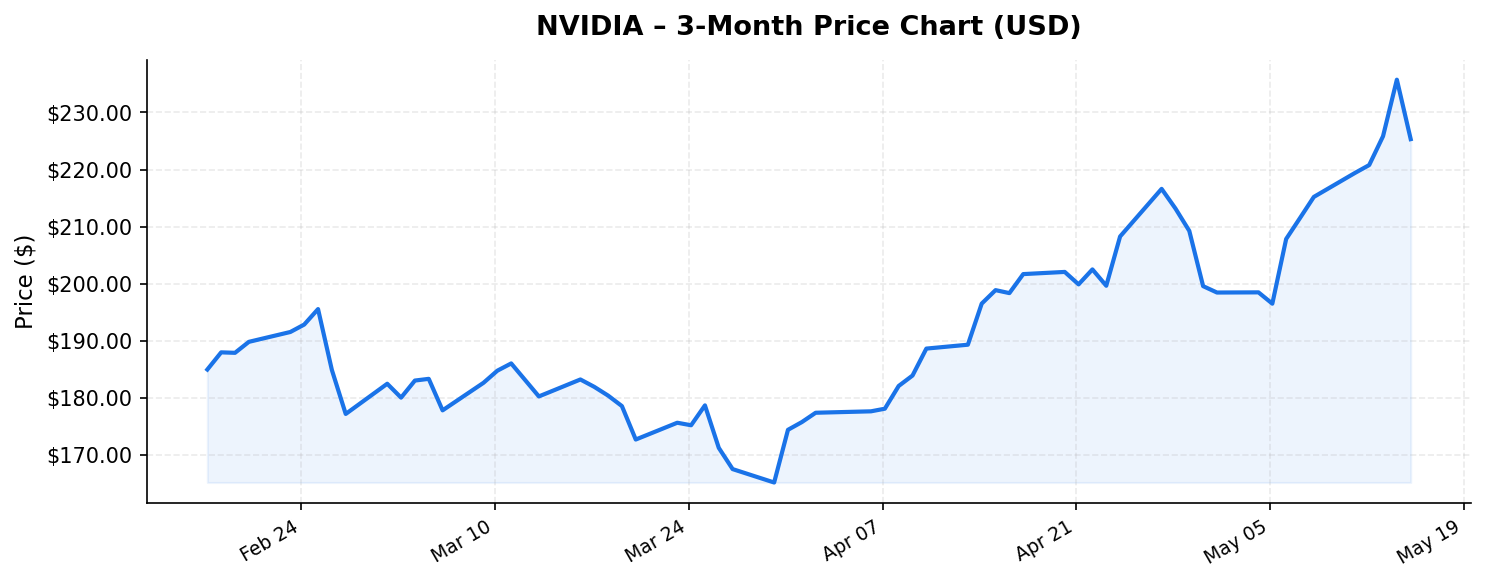

Few companies have defined the artificial intelligence era as decisively as NVIDIA (NVDA). As of May 16, 2026, the chipmaker commands a staggering market capitalization of $5.5 trillion, making it one of the most valuable publicly traded companies on earth. With a current share price of $225.32 — sitting just 4.7% below its 52-week high of $236.54 — NVIDIA continues to trade near record territory. But for international investors evaluating whether to enter, add to, or trim a position, the critical question remains: does the data support the valuation, or has the market priced in perfection?

In this analysis, we’ll break down NVIDIA’s business fundamentals, competitive moat, valuation metrics, and key risks to help global investors make an informed decision.

The AI Infrastructure Giant: Business Overview and Revenue Engine

NVIDIA’s transformation from a gaming GPU company to the backbone of global AI infrastructure is one of the most remarkable corporate pivots in modern history. The company designs and sells graphics processing units (GPUs), data center accelerators, networking hardware, and the software ecosystem that ties it all together. Its CUDA platform has become the de facto standard for AI development, creating deep lock-in across enterprise, cloud, and research customers.

The numbers tell the story with blinding clarity. NVIDIA’s trailing twelve-month (TTM) revenue stands at $215.9 billion — a figure that would have been almost unimaginable just three years ago when the company was generating roughly $27 billion annually. This eightfold revenue expansion has been driven almost entirely by explosive demand for AI training and inference chips, particularly the H100, H200, and the newer Blackwell architecture GPUs.

What makes NVIDIA’s financial profile truly exceptional is its profitability. The company’s return on equity (ROE) of 101.5% signals an extraordinarily efficient deployment of shareholder capital. For context, an ROE above 20% is typically considered excellent; NVIDIA’s figure is more than five times that benchmark. This level of profitability reflects both premium pricing power and a scalable fabless manufacturing model where NVIDIA designs chips but outsources fabrication to partners like TSMC.

For international investors, NVIDIA also offers a modest but growing dividend yield of 2.00%. While this is not a traditional income stock, the fact that NVIDIA can sustain a meaningful dividend while reinvesting aggressively in R&D signals financial health and management confidence. It’s worth noting, however, that non-US investors should account for the standard 30% US withholding tax on dividends (reducible under tax treaties in many jurisdictions).

Competitive Position: A Moat Built on Hardware, Software, and Ecosystem

NVIDIA’s dominance in AI accelerators is not simply a matter of having the fastest chip — it’s an ecosystem advantage that competitors have struggled to replicate. The company’s moat rests on three interlocking pillars:

- Hardware leadership: NVIDIA’s Blackwell and next-generation Rubin architectures continue to set performance benchmarks in AI training and inference workloads. Hyperscalers like Microsoft, Google, Amazon, and Meta remain among the company’s largest customers, and their capital expenditure plans for AI infrastructure show no signs of decelerating.

- Software ecosystem (CUDA): With over 5 million developers building on CUDA, switching costs are enormous. Competing hardware from AMD, Intel, and custom silicon (Google’s TPUs, Amazon’s Trainium) must not only match NVIDIA’s hardware performance but also overcome a software ecosystem built over nearly two decades.

- Networking and full-stack integration: NVIDIA’s acquisition of Mellanox (now NVIDIA Networking) has given it control over high-speed interconnects critical for scaling AI clusters. The ability to sell complete data center solutions — GPUs, networking, and software — provides both a revenue multiplier and a competitive barrier.

That said, competition is intensifying. AMD’s MI300 series has gained traction in select deployments, and custom AI chips from hyperscalers threaten to chip away at NVIDIA’s data center share over the medium term. The price-to-book ratio of 34.81x reflects a market that is pricing in sustained dominance, leaving little room for competitive erosion.

Valuation Deep Dive: What the Numbers Say About the Price

Valuation is where the NVIDIA thesis becomes most contentious. At a P/E ratio of 46.1x, the stock is trading at a significant premium to the broader S&P 500 (which historically trades between 18-22x earnings) and to most semiconductor peers. However, context matters. A P/E of 46x is actually a notable compression from the 60-70x multiples NVIDIA commanded during the peak of AI euphoria in 2024, suggesting that earnings growth has been catching up to the stock price.

Let’s put the valuation in perspective with a simple calculation. At a market cap of $5.5 trillion and TTM revenue of $215.9 billion, NVIDIA trades at roughly 25.5x trailing sales. This is an elevated multiple by any traditional standard, but NVIDIA’s net margins — which have expanded to well above 50% — partially justify this premium. The company is converting revenue to profit at a rate that few large-cap companies in any sector can match.

The stock’s position within its 52-week range of $129.16 to $236.54 is also instructive. At $225.32, NVIDIA is trading in the upper quartile of its annual range, just 4.7% below the high. This proximity to the peak suggests strong momentum and sustained institutional demand, but it also means that international investors entering now have limited technical cushion. A pullback to even the midpoint of the 52-week range would represent a decline of approximately 23% — a meaningful drawdown for any portfolio.

For value-oriented international investors, the current entry point demands high conviction in NVIDIA’s forward growth trajectory. Consensus estimates suggest revenue could exceed $280-300 billion in the next fiscal year, which would bring the forward P/E closer to 30-35x — a more palatable level for a high-growth technology leader, but still far from “cheap.”

Key Risks International Investors Must Consider

No investment thesis is complete without a candid assessment of risks, and NVIDIA carries several that are particularly relevant for non-US investors:

- Geopolitical and export control risk: The US government has imposed increasingly restrictive export controls on advanced AI chips to China and other nations. China once represented a significant revenue stream for NVIDIA, and further restrictions — or retaliatory measures — could materially impact sales. International investors should monitor US-China technology tensions as an ongoing variable.

- Customer concentration and capex cycles: A significant portion of NVIDIA’s revenue comes from a handful of hyperscale cloud providers. If these companies slow their AI infrastructure spending — whether due to macroeconomic pressure, overcapacity concerns, or a shift toward custom silicon — NVIDIA’s growth rate could decelerate sharply.

- Currency risk: For investors outside the United States, purchasing NVDA shares means taking on US dollar exposure. A strengthening local currency against the dollar would erode returns when converting back, regardless of NVIDIA’s stock performance. This is a structural consideration for any international position in US equities.

- Valuation compression risk: At 46.1x earnings and nearly 35x book value, NVIDIA is priced for execution perfection. Any earnings miss, margin compression, or guidance disappointment could trigger a sharp rerating. The stock’s high beta means it tends to amplify broader market moves — both up and down.

- Supply chain dependency: NVIDIA relies heavily on TSMC for chip fabrication. Geopolitical risks surrounding Taiwan, production disruptions, or capacity constraints could impact NVIDIA’s ability to meet demand.

Investment Thesis: The Bull and Bear Case for International Investors

The bull case for NVIDIA remains compelling. The company sits at the center of a generational technology shift. AI infrastructure spending globally is projected to exceed $1 trillion cumulatively over the next several years, and NVIDIA is capturing a dominant share of that investment. Its 101.5% ROE, rapid revenue growth, and pricing power suggest a business operating in rarefied air. The introduction of a 2% dividend yield also makes the stock incrementally more attractive for investors who appreciate even modest income alongside capital appreciation.

The bear case centers on valuation and sustainability. At $5.5 trillion in market capitalization, NVIDIA must continue growing at exceptional rates simply to justify its current price. History shows that maintaining 50%+ growth rates becomes exponentially harder as the revenue base expands. The competitive landscape, while still favorable, is not static — and the risk of customer defection to custom silicon is real.

For international investors, NVIDIA represents a high-conviction play on the continuation of the global AI buildout. It is not a stock for those seeking deep value or defensive characteristics. However, for growth-oriented portfolios with a multi-year time horizon and tolerance for volatility, NVIDIA’s market position, financial metrics, and technological leadership make it one of the most consequential holdings available in US public markets today.

Those considering an initial position may benefit from a dollar-cost averaging approach — building exposure gradually rather than committing a full allocation near all-time highs. This strategy can help mitigate timing risk and smooth out the impact of NVIDIA’s inherent price volatility.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or an offer to buy or sell any securities. All data referenced is as of May 16, 2026, and may change. International investors should consult with a qualified financial advisor in their jurisdiction before making any investment decisions. Past performance is not indicative of future results.