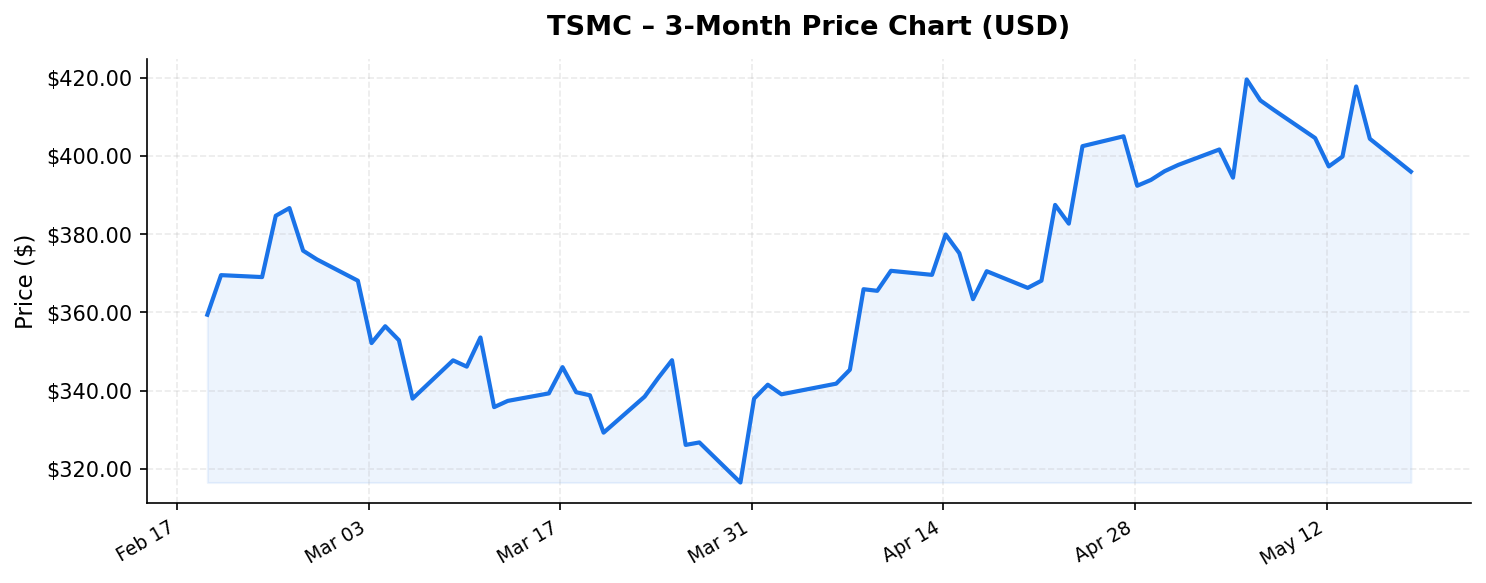

Taiwan Semiconductor Manufacturing Company, or TSMC (TSM), has cemented its position as the undisputed backbone of the global semiconductor industry. As of May 19, 2026, the stock trades at $395.95 — just 6.2% below its 52-week high of $421.97 — with a staggering market capitalization of $2.1 trillion. For international investors looking to gain exposure to the AI revolution and advanced chip manufacturing, TSMC remains one of the most consequential stocks on the planet. But with a P/E ratio of 34.0x and a price-to-book ratio that demands serious scrutiny at 60.57x, the question is whether the valuation still leaves room for upside. Let’s break down the numbers.

Business Overview: The Foundry That Powers the Digital World

TSMC is the world’s largest dedicated semiconductor foundry, manufacturing chips designed by other companies rather than selling its own branded products. Its client roster reads like a who’s-who of global technology: Apple, NVIDIA, AMD, Qualcomm, Broadcom, and dozens of other firms depend on TSMC’s advanced manufacturing nodes to produce their most critical silicon. The company commands an estimated 60%+ share of the global foundry market and an even more dominant position — north of 90% — in the most advanced process nodes (sub-5nm), where the highest-margin, highest-performance chips are fabricated.

With trailing twelve-month revenue of approximately $4.1 trillion (in New Taiwan Dollar terms, roughly $125-130 billion USD), TSMC’s top line reflects explosive growth fueled by insatiable demand for AI accelerators, high-performance computing (HPC) chips, and advanced smartphone processors. The company’s return on equity of 36.2% underscores its exceptional profitability and capital efficiency — a remarkable achievement for a business that requires tens of billions of dollars in annual capital expenditure to stay at the technological frontier.

TSMC’s competitive moat is arguably the deepest in the entire technology sector. Building a leading-edge semiconductor fab costs upward of $20 billion, takes years to construct, and requires decades of accumulated process engineering know-how. Intel and Samsung are the only credible competitors at the cutting edge, and both have struggled to match TSMC’s yields, reliability, and pace of innovation. This structural advantage translates directly into pricing power and margin durability.

Valuation Deep Dive: What the Numbers Tell Us

At $395.95 per share, TSMC trades at a P/E ratio of 34.0x trailing earnings. For a company growing revenue at a pace that has consistently exceeded 20% year-over-year in recent quarters — driven by AI infrastructure buildout — this multiple is not unreasonable relative to mega-cap tech peers. For context, NVIDIA has frequently traded at significantly higher multiples during similar growth phases. However, 34x earnings does price in substantial forward growth expectations, and any deceleration in AI-related spending could pressure the stock.

The price-to-book ratio of 60.57x is eye-catching and warrants careful interpretation. This extraordinarily high figure reflects two realities: first, TSMC’s physical assets (fabs, equipment) are carried on the balance sheet at historical cost and depreciated aggressively, significantly understating their replacement value and economic worth. Second, the market is assigning enormous value to TSMC’s intangible competitive advantages — its process technology leadership, customer relationships, and institutional knowledge — none of which appear on the balance sheet. While a 60x P/B ratio might signal overvaluation in a capital-light software business, for a capital-intensive foundry with TSMC’s moat, it primarily reflects the market’s recognition that these assets are irreplaceable.

The stock’s current price sits just 6.2% below its 52-week high of $421.97 and more than double its 52-week low of $190.03. This wide 52-week range — a spread of over 120% — speaks to the volatility that characterized TSMC shares over the past year, likely driven by geopolitical tensions, AI demand fluctuations, and broader market cycles. Investors who bought near the lows have been handsomely rewarded, but the proximity to all-time highs means new entrants are paying a premium for stability.

One data point that requires clarification is the listed dividend yield of 96.00%. This figure appears to reflect a data anomaly — potentially a special dividend, a stock split adjustment, or a currency conversion issue in the data feed. TSMC has historically paid a modest but growing dividend, typically yielding between 1% and 2% on the ADR. International investors should verify the actual dividend yield through their brokerage platform before making income-based investment decisions. Historically, TSMC has been more of a growth-and-reinvestment story than a high-yield income play, with the company plowing the majority of its cash flow back into next-generation fab construction.

Key Risks: Geopolitics, Concentration, and Cyclicality

No analysis of TSMC is complete without addressing the elephant in the room: geopolitical risk. TSMC’s most advanced manufacturing is concentrated in Taiwan, an island over which China claims sovereignty. Any military conflict or even heightened tensions across the Taiwan Strait could disrupt the global chip supply chain in ways that would make the 2020-2021 semiconductor shortage look mild by comparison. While TSMC has begun diversifying with fabs in Arizona, Japan, and Germany, the vast majority of its cutting-edge production capacity will remain in Taiwan for the foreseeable future.

For international investors, this geopolitical dimension adds a layer of risk that is difficult to hedge. The stock has historically experienced sharp selloffs during periods of elevated cross-strait tension, even without any actual disruption to operations. This risk premium is arguably already partially reflected in TSMC’s valuation — the company might trade at even higher multiples if it were headquartered in a geopolitically neutral location.

Additional risks include:

- Customer concentration: Apple and NVIDIA together represent a substantial portion of TSMC’s revenue. Any shift in these relationships — whether due to in-house chip development by customers or demand slowdowns — could materially impact results.

- AI spending sustainability: Much of TSMC’s recent growth has been driven by the massive buildout of AI data center infrastructure. If AI capital expenditure cycles prove more volatile or shorter-lived than expected, growth rates could moderate sharply.

- Capital expenditure burden: TSMC must invest $30-40+ billion annually to maintain its technological lead. Any misstep in technology development — such as lower-than-expected yields on next-generation nodes — could temporarily compress margins.

- Currency risk: International investors buying the ADR (TSM) are exposed to fluctuations in the USD/TWD exchange rate, which can amplify or dampen returns relative to the underlying Taiwanese-listed shares.

- Regulatory risk: Export controls, particularly U.S. restrictions on advanced chip sales to China, can limit TSMC’s addressable market. Evolving regulations require constant monitoring.

Investment Thesis: Why International Investors Should Pay Attention

Despite the risks, the bull case for TSMC remains compelling. The company sits at the intersection of virtually every major technology trend: artificial intelligence, cloud computing, autonomous vehicles, 5G/6G connectivity, and the Internet of Things. As long as the world needs more advanced semiconductors — and every indication suggests demand will only accelerate — TSMC is positioned to capture a disproportionate share of that value.

The 36.2% return on equity demonstrates that TSMC is not merely growing for growth’s sake — it is generating exceptional returns on the capital it deploys. This combination of high growth and high returns on capital is rare among companies of this scale and is the primary reason the market assigns such a premium valuation.

For international investors specifically, TSMC offers several attractive attributes. The ADR trades on the NYSE with deep liquidity, making it easily accessible from virtually any brokerage worldwide. The company reports in English, holds regular analyst days, and maintains transparency standards on par with U.S.-listed multinationals. Its revenue is inherently diversified across global customers and end markets, providing natural exposure to worldwide technology demand rather than any single economy.

From a portfolio construction perspective, TSMC offers differentiated exposure that is difficult to replicate. There is simply no substitute for TSMC’s role in the semiconductor value chain, and owning the stock provides indirect exposure to the success of its entire customer base — from Apple’s iPhone to NVIDIA’s AI accelerators — without the need to pick individual winners in those competitive markets.

At $395.95, TSMC is not cheap by any traditional metric. The 34x P/E and 60.57x P/B ratios price in considerable growth. But for investors with a multi-year time horizon who believe in the structural expansion of AI and advanced computing, TSMC represents a foundational holding — one that offers a unique combination of technological dominance, financial strength, and secular growth tailwinds that few companies in history have matched.

Conclusion

TSMC stands as a $2.1 trillion testament to the irreplaceable value of cutting-edge semiconductor manufacturing. Trading near its 52-week highs with strong profitability metrics and unmatched competitive positioning, the stock rewards investors who can tolerate geopolitical uncertainty and elevated valuation multiples. For international investors seeking meaningful exposure to the AI-driven future of technology, TSMC remains one of the most important stocks to understand — and potentially own — in the global equity market. The current valuation demands growth delivery, but TSMC’s track record suggests it is one of the few companies capable of meeting those expectations.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice, a recommendation, or a solicitation to buy or sell any security. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. Market data referenced is as of May 19, 2026, and may have changed since publication.