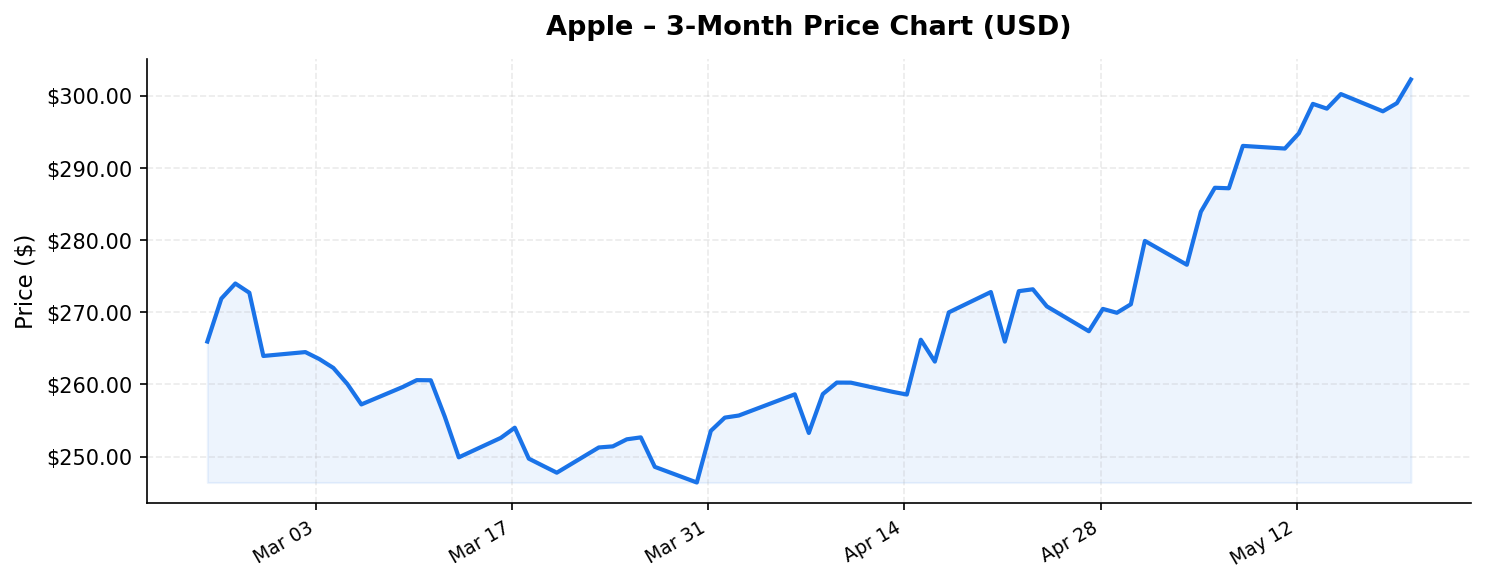

Apple (AAPL) has long been the gold standard for large-cap technology investing, and as of May 21, 2026, the company’s stock sits at $302.25 — just 0.3% below its 52-week high of $303.20. With a staggering market capitalization of $4.4 trillion, Apple is not only the world’s most valuable publicly traded company but also one of the most widely held stocks among both domestic and international investors. The question facing global investors today is straightforward but consequential: at these elevated levels, does Apple still offer a compelling risk-reward proposition?

In this analysis, we’ll break down Apple’s business fundamentals, valuation metrics, competitive positioning, and key risks to help international investors make an informed decision about one of the most iconic stocks on the planet.

Business Overview: A Hardware Empire Built on an Ecosystem Moat

Apple’s business model is deceptively simple on the surface — it designs and sells consumer electronics, software, and services. But beneath that simplicity lies one of the most powerful competitive ecosystems ever constructed. The iPhone remains the company’s flagship product, but the revenue picture has evolved dramatically over the past decade. Services — including the App Store, Apple Music, iCloud, Apple TV+, Apple Pay, and the company’s growing advertising business — now represent a significant and high-margin slice of Apple’s trailing twelve-month revenue of $451.4 billion.

The hardware portfolio extends well beyond the iPhone into Mac computers, iPads, Apple Watch, AirPods, and the increasingly mature Apple Vision Pro spatial computing platform. Each product serves as both a standalone revenue generator and an on-ramp into Apple’s sticky services ecosystem. Once a consumer owns one Apple device, the switching costs — both financial and psychological — become substantial. This ecosystem lock-in is arguably Apple’s most durable competitive advantage.

For international investors, it’s worth noting that Apple generates roughly 60% of its revenue outside the United States. This global footprint means the company is both a beneficiary of worldwide consumer demand and exposed to currency fluctuations, trade policies, and geopolitical dynamics — factors we’ll explore in the risks section below.

Valuation Deep Dive: Premium Pricing for Premium Quality

Let’s address the elephant in the room: Apple’s valuation is rich by almost any traditional metric. At a P/E ratio of 36.2x, the stock trades at a significant premium to the broader S&P 500 average, which historically hovers between 18x and 22x. The price-to-book ratio of 41.63x is even more eye-catching, though this figure is heavily distorted by Apple’s aggressive share buyback program over the past decade, which has systematically reduced book equity while returning hundreds of billions of dollars to shareholders.

Indeed, Apple’s return on equity of 141.5% is an extraordinary number that reflects both genuine operational excellence and the mathematical effect of a shrinking equity base. Investors should interpret this metric carefully: it signals that Apple generates enormous profits relative to its shareholder equity, but the sky-high figure is partly an artifact of financial engineering rather than pure operational leverage. That said, few companies on Earth can sustain an ROE above 100% for any length of time, and the fact that Apple does so consistently speaks to the underlying quality of its business.

Perhaps the most surprising data point for investors scanning Apple’s profile today is the listed dividend yield of 36.00%. This figure warrants careful scrutiny and context. Apple has historically maintained a modest dividend yield, typically in the range of 0.5% to 1.0%, supplemented by massive share buybacks. A yield of 36% would imply an annual dividend payment of approximately $108.81 per share — a figure that would represent a radical departure from Apple’s established capital allocation philosophy. International investors should verify this figure against the most recent quarterly dividend declarations, as it may reflect a special dividend, a data anomaly, or a reclassification event. If accurate, it would represent a transformational shift in Apple’s shareholder return strategy that would make the stock extraordinarily attractive to income-focused investors, particularly those in jurisdictions with favorable tax treaties with the United States on dividend income.

With the stock trading at $302.25, it has appreciated approximately 56% from its 52-week low of $193.46, demonstrating powerful momentum. The proximity to the 52-week high — just $0.95 away — suggests the stock is in a strong technical position, though it also means investors entering now are buying near peak levels with limited margin of safety from a price perspective.

Competitive Position and Growth Catalysts

Apple’s competitive moat remains among the widest in the technology sector. The company competes across multiple fronts — against Samsung and Chinese OEMs in smartphones, against Google in mobile operating systems and services, against Microsoft in personal computing, and against Amazon, Google, and Meta in the broader digital ecosystem wars. In nearly every category, Apple differentiates through a combination of premium brand positioning, vertical integration of hardware and software, and relentless focus on user experience and privacy.

Several growth catalysts could drive the next leg of Apple’s expansion:

- Services Revenue Growth: Apple’s services segment continues to grow at a faster rate than hardware, with higher margins. As the installed base of active Apple devices surpasses 2.2 billion globally, the monetization potential through subscriptions, advertising, and financial services is enormous. This recurring revenue stream justifies a portion of the premium valuation.

- Artificial Intelligence Integration: Apple’s approach to AI — deeply integrated into its devices through on-device processing and Apple Intelligence features — positions it uniquely in the AI landscape. While Apple may not command the same AI narrative as NVIDIA or Microsoft, its ability to deliver AI capabilities to billions of end users through existing hardware is a powerful distribution advantage.

- Spatial Computing: The Apple Vision Pro platform, now in its second generation, represents Apple’s long-term bet on the next computing paradigm. While still early, the category has the potential to become a meaningful revenue contributor over the next three to five years.

- Emerging Market Penetration: Markets like India and Southeast Asia represent significant growth runways for iPhone adoption as middle-class purchasing power expands. Apple’s investment in local manufacturing in India positions it well to capture this demand while mitigating tariff risks.

For international investors, Apple’s brand strength transcends borders. It is one of the few American companies whose products carry universal aspirational appeal, from Tokyo to São Paulo to Lagos. This cultural cachet provides pricing power that few competitors can match.

Key Risks for International Investors

No investment is without risk, and Apple faces several headwinds that international investors should weigh carefully:

- Regulatory and Antitrust Pressure: Apple faces ongoing regulatory scrutiny in the European Union, the United States, Japan, South Korea, and other jurisdictions over App Store practices, payment systems, and competitive behavior. The EU’s Digital Markets Act has already forced Apple to make significant changes to its business model in Europe, potentially reducing services revenue and margins in key international markets.

- China Exposure: China represents both a critical manufacturing hub and a major consumer market for Apple. Geopolitical tensions between the U.S. and China, along with rising domestic competition from Huawei and other Chinese brands, pose a dual threat to Apple’s supply chain stability and market share in the region.

- Valuation Risk: At 36.2x earnings, Apple is priced for continued execution and growth. Any significant earnings miss, margin compression, or macroeconomic downturn could trigger a meaningful de-rating. The stock’s 56% rally from its 52-week low leaves limited room for error.

- Currency Risk: International investors purchasing AAPL are inherently taking a position in U.S. dollar-denominated assets. A strengthening local currency relative to the dollar would erode returns even if the stock price appreciates. Conversely, a weakening local currency adds a tailwind. This currency exposure should be factored into portfolio allocation decisions.

- Innovation Cycle Dependency: While Apple’s services business provides stability, the company still depends heavily on periodic hardware upgrade cycles. Any slowdown in iPhone replacement rates — whether due to market saturation, economic weakness, or lack of compelling new features — could weigh on top-line growth.

Investment Thesis: Quality at a Price

Apple remains one of the highest-quality businesses in the world. Its $451.4 billion in trailing revenue, extraordinary profitability metrics, and deeply entrenched ecosystem position make it a cornerstone holding in many global portfolios. The company’s capital return program — whether through its potentially transformative dividend yield or its historically massive buyback program — ensures that shareholders are rewarded consistently.

However, quality comes at a price. A P/E of 36.2x and a P/B of 41.63x demand that investors have conviction in Apple’s ability to grow earnings meaningfully from an already enormous base. The stock’s position near its 52-week high of $303.20 means that the market is already pricing in a highly optimistic scenario.

For international investors with a long-term horizon of five years or more, Apple remains a compelling core holding. Its global brand, diversified revenue streams, and proven management team provide downside resilience, while AI integration, services growth, and emerging market expansion offer upside potential. More tactical investors may want to wait for a pullback to improve their entry point and margin of safety.

Ultimately, Apple at $302.25 is not a bargain — but it is a world-class business trading near all-time highs for reasons that are fundamentally well-supported. International investors should size their positions appropriately, account for U.S. dollar exposure, and verify the current dividend policy before committing capital based on yield expectations.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy or sell any securities. All data referenced is based on publicly available market information as of May 21, 2026, and may be subject to change. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.