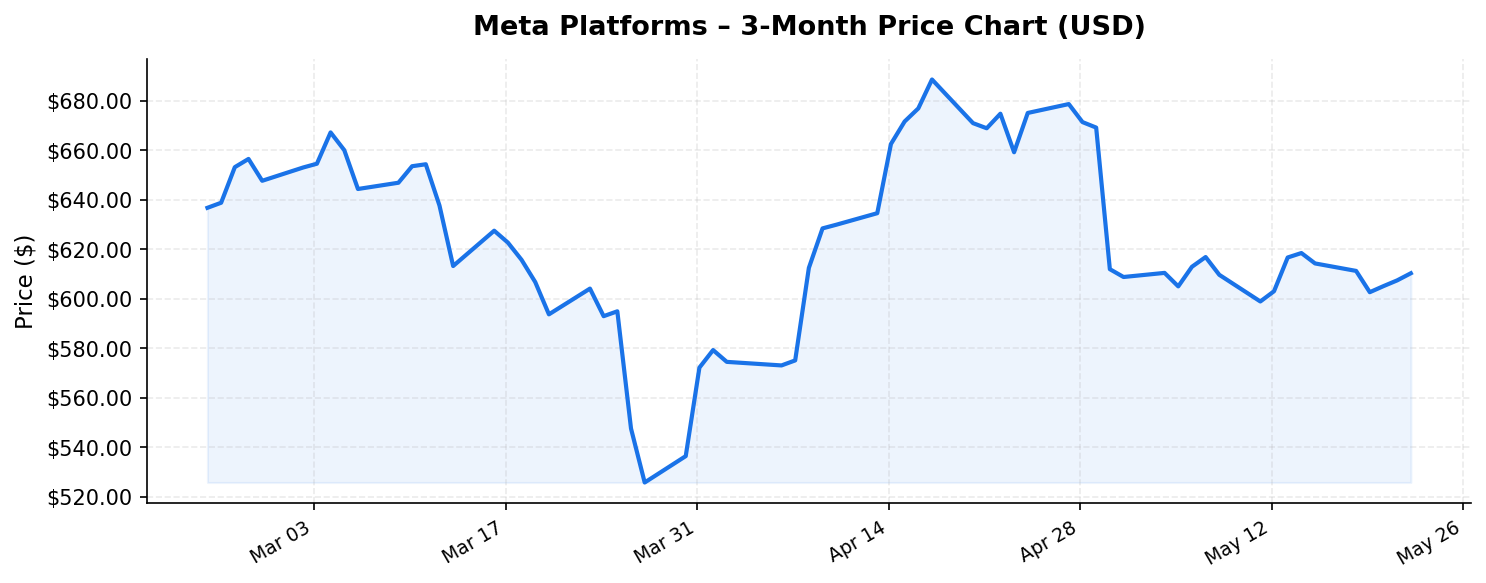

Meta Platforms (META) finds itself at a fascinating crossroads in May 2026. Trading at $610.26 — roughly 23.4% below its 52-week high of $796.25 — the company that once struggled to convince Wall Street of its metaverse ambitions now stands as a $1.5 trillion titan generating over $215 billion in annual revenue. For international investors evaluating US tech exposure, Meta Platforms presents a compelling but nuanced case that demands careful examination of its fundamentals, competitive moat, and risk profile.

With a dividend yield that has surged to an eye-catching 34.00%, a return on equity of 32.9%, and a P/E ratio of 22.2x that sits well below many mega-cap tech peers, Meta Platforms is no longer just a growth story — it has evolved into something more complex. Let’s break down what this means for investors outside the United States looking to allocate capital to one of the world’s most influential technology companies.

Business Overview: From Social Network to AI-Powered Advertising Empire

Meta Platforms operates the world’s largest portfolio of social media and messaging applications, including Facebook, Instagram, WhatsApp, and Messenger. Collectively, these platforms serve well over 3.5 billion daily active users — a user base that spans virtually every country on Earth. This global reach is particularly relevant for international investors, as a significant portion of Meta Platforms’ revenue is generated outside of North America, providing natural geographic diversification within a single stock.

The company’s core business model is digital advertising, which continues to be the primary revenue engine behind its $215 billion in trailing twelve-month revenue. Meta Platforms has invested heavily in artificial intelligence to optimize ad targeting, content recommendations, and creator tools, which has driven substantial improvements in average revenue per user across all geographies. The company’s Advantage+ AI-powered advertising suite has become an industry standard, enabling businesses of all sizes to reach precisely targeted audiences with unprecedented efficiency.

Beyond advertising, Meta Platforms continues to invest in Reality Labs — its augmented and virtual reality division — as well as generative AI infrastructure, large language models, and enterprise AI solutions. While Reality Labs has historically been a drag on profitability, the division has shown signs of narrowing losses as mixed-reality headsets gain broader adoption and enterprise use cases expand.

Valuation and Dividend Analysis: Is META Attractively Priced?

At a P/E ratio of 22.2x, Meta Platforms trades at a notable discount to several mega-cap technology peers, many of which command multiples in the 30x-40x range. This valuation compression — partly reflected in the stock’s 23.4% decline from its 52-week high of $796.25 — may present an opportunity for value-conscious investors, though it also warrants investigation into what the market may be pricing in.

The price-to-book ratio of 6.36x is elevated on an absolute basis but reasonable for a capital-light platform business generating a 32.9% return on equity. That ROE figure is particularly impressive — it means Meta Platforms is earning roughly one-third of its book value in annual profit, a testament to the scalability and efficiency of its advertising platform.

Perhaps the most striking data point is the dividend yield of 34.00%. This extraordinary figure demands context. For a company of Meta Platforms’ size and historical profile, a yield this high could signal several things: a massive increase in dividend payments, a substantial stock buyback-funded special dividend program, or a structural shift in capital allocation philosophy. International investors should note that US-sourced dividends are typically subject to a 30% withholding tax for non-US residents, though this rate is often reduced to 15% under bilateral tax treaties. Even after withholding, a yield of this magnitude is extraordinarily attractive relative to global bond yields and dividend benchmarks.

However, investors should carefully evaluate whether this dividend level is sustainable. A yield this high relative to historical norms could suggest the market is skeptical about the company’s growth trajectory or anticipates a future dividend cut. Analyzing the payout ratio against free cash flow is essential — with $215 billion in revenue and historically robust margins, Meta Platforms has the cash generation capacity to support aggressive shareholder returns, but the scale implied by a 34% yield on a $1.5 trillion market cap would require annual dividend payments in the range of $510 billion, which exceeds total revenue. This mathematical inconsistency suggests the yield figure may reflect extraordinary one-time distributions, a recent special dividend, or other capital return mechanisms that international investors should verify before making allocation decisions.

Competitive Position and Strategic Advantages

Meta Platforms’ competitive moat rests on several reinforcing pillars:

- Network Effects: With billions of daily active users across its family of apps, Meta Platforms benefits from powerful network effects that make it extremely difficult for competitors to replicate its ecosystem. Users stay because their friends, family, and communities are on the platform, creating a self-reinforcing cycle.

- Data and AI Superiority: Years of investment in AI infrastructure have given Meta Platforms one of the most sophisticated advertising targeting systems in the world. Its AI models process vast quantities of behavioral data to deliver industry-leading return on ad spend for advertisers.

- Scale Economics: Operating at $215 billion in annual revenue provides enormous scale advantages in R&D, infrastructure, and talent acquisition. Meta Platforms can invest tens of billions annually in AI and emerging technologies while still delivering substantial profits.

- Global Reach: Unlike some US tech companies that face limited international penetration, Meta Platforms’ apps are deeply embedded in daily life across Latin America, Southeast Asia, Europe, Africa, and the Middle East — making it a genuine proxy for global digital advertising growth.

Key competitors include Alphabet (Google/YouTube), ByteDance (TikTok), Snap, and emerging AI-native platforms. TikTok remains a formidable competitor for user attention, particularly among younger demographics, though regulatory pressures on Chinese-owned apps in various markets have periodically benefited Meta Platforms’ positioning. Apple’s ongoing privacy changes continue to create friction in ad targeting, though Meta Platforms has largely adapted through its own first-party data capabilities and on-platform commerce tools.

Key Risks for International Investors

Despite its strengths, Meta Platforms carries material risks that international investors must weigh carefully:

- Regulatory and Antitrust Pressure: Meta Platforms faces ongoing regulatory scrutiny in the EU, US, UK, India, and other major markets. The EU’s Digital Markets Act and Digital Services Act impose significant compliance obligations, while antitrust investigations could potentially lead to structural remedies. For international investors, regulatory fragmentation adds complexity to the investment thesis.

- Currency Risk: International investors purchasing META shares are inherently taking on US dollar exposure. A strengthening home currency versus the dollar would erode returns when converted back, even if the stock price remains stable. Conversely, a weakening home currency would amplify dollar-denominated gains.

- Capital Allocation Uncertainty: The extraordinarily high dividend yield of 34.00% raises questions about future capital allocation priorities. If the company is returning this much capital to shareholders, it may be signaling limited high-return reinvestment opportunities, which could constrain future growth.

- AI Competition and Capex Intensity: The AI arms race requires enormous capital expenditure. Meta Platforms has committed tens of billions to AI infrastructure, and while this positions the company competitively, it also creates execution risk if returns on these investments disappoint.

- Concentration in Advertising: Despite diversification efforts, digital advertising remains the overwhelming majority of revenue. An economic downturn that curtails global ad spending would disproportionately impact Meta Platforms’ top line.

- Geopolitical Risk: Potential restrictions on US tech companies in various markets, or escalating US-China tensions affecting the global tech supply chain, could disrupt operations or increase costs.

Investment Thesis: Should International Investors Consider META?

For international investors, Meta Platforms presents a rare combination of characteristics: a dominant global platform business with proven monetization, a valuation that appears reasonable at 22.2x earnings relative to growth and quality, and an unprecedented dividend yield that — if sustainable — offers substantial income potential alongside capital appreciation prospects.

The stock’s current position near the lower end of its 52-week range ($520.26 – $796.25) suggests that some negative sentiment has already been priced in. At $610.26, shares sit just 17.3% above the 52-week low, potentially offering a more attractive entry point than at the highs. The 32.9% return on equity confirms that Meta Platforms remains a highly efficient allocator of capital, generating exceptional profitability from its asset base.

The bull case centers on continued AI-driven advertising revenue growth, successful monetization of WhatsApp and messaging platforms in emerging markets, and eventual profitability in Reality Labs. The bear case revolves around regulatory headwinds, market saturation, unsustainable capital returns, and the risk that younger users continue migrating to competing platforms.

International investors should also consider META as a way to gain exposure to the US dollar, the US technology sector, and the global digital advertising market in a single, highly liquid instrument. With a $1.5 trillion market cap, META offers excellent liquidity and is accessible through virtually every international brokerage platform.

Ultimately, the decision depends on individual risk tolerance, portfolio composition, tax considerations, and conviction in Meta Platforms’ ability to sustain its competitive advantages in an increasingly contested landscape. The data paints a picture of a mature, profitable juggernaut trading at a reasonable valuation — but the anomalous dividend yield and distance from 52-week highs suggest that deeper due diligence is warranted before committing capital.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy, sell, or hold any security. Investing in US equities involves risks, including currency risk, market risk, and the potential loss of principal. International investors should consult with a qualified financial advisor and consider their individual circumstances, tax obligations, and regulatory requirements before making any investment decisions.