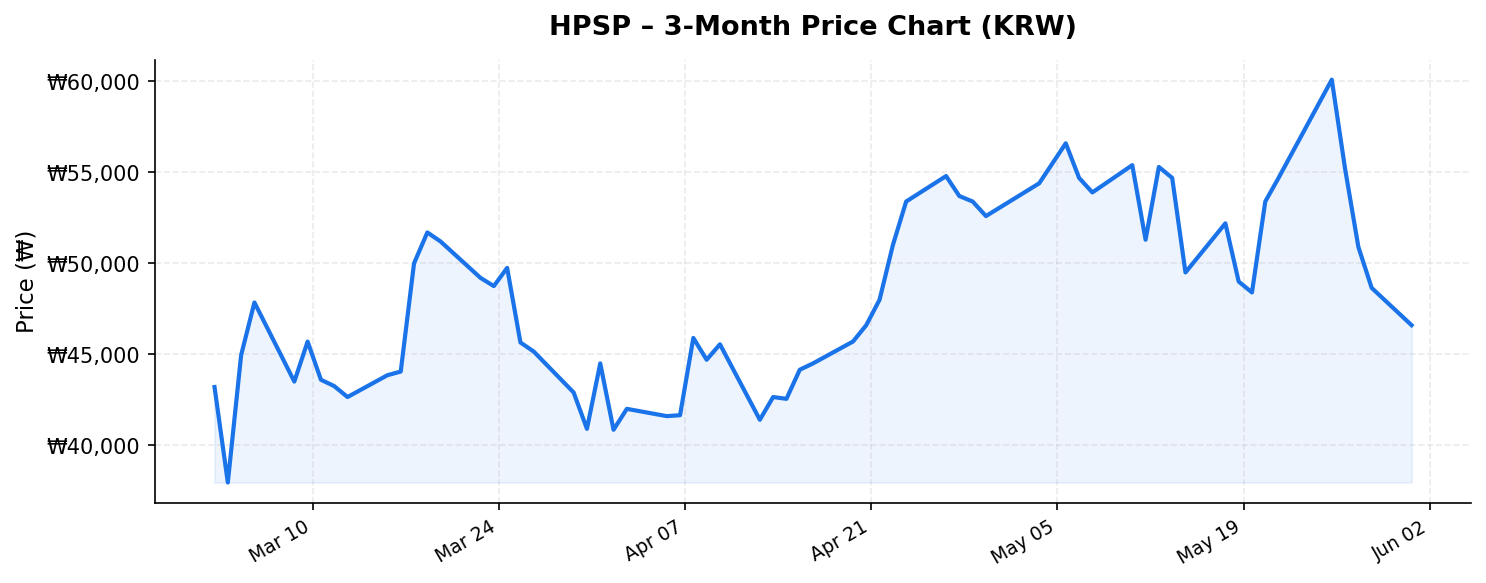

In the fast-evolving world of semiconductor manufacturing, few niche equipment makers have captured investor attention as dramatically as HPSP (HPSP, 403870.KS). The South Korean company, a dominant player in high-pressure annealing (HPA) equipment, has seen its share price plummet roughly 46.5% from its 52-week high of ₩67,800 to its current level of ₩36,300. For international investors scanning the Korean market for deep-value opportunities in the semiconductor supply chain, this drawdown raises a critical question: Is this a cyclical buying opportunity, or has the investment thesis fundamentally changed?

With the stock currently sitting much closer to its 52-week low of ₩22,250 than its peak — and trading at what could be a significant discount to its intrinsic value — a thorough, data-driven analysis is warranted. Let’s break down the business, competitive dynamics, risks, and what this all means for global investors.

Business Overview: The Monopoly in High-Pressure Annealing

HPSP specializes in high-pressure annealing (HPA) equipment, a critical process step used in advanced semiconductor fabrication. High-pressure annealing involves exposing semiconductor wafers to elevated temperatures and pressures — typically using hydrogen or deuterium gas — to repair lattice damage, improve gate oxide quality, and enhance overall device performance. As chipmakers push toward ever-smaller nodes (3nm, 2nm, and beyond), the importance of HPA in achieving reliable transistor characteristics has grown substantially.

What makes HPSP particularly compelling is its near-monopoly position. The company commands an estimated 90%+ global market share in dedicated high-pressure annealing equipment. Its primary customers include the world’s largest semiconductor manufacturers — Samsung Electronics, SK hynix, and Taiwan Semiconductor Manufacturing Company (TSMC) — as well as leading memory and logic foundries across Asia. This customer concentration, while a risk factor, also underscores the mission-critical nature of HPSP’s technology.

The company went public on the KOSDAQ in 2022 and quickly became a market darling, with its stock surging on the back of the AI-driven semiconductor capex boom. Revenue growth was explosive, driven by increasing adoption of HPA in both logic and memory fabrication lines. HPSP’s asset-light business model — it designs and assembles equipment rather than operating heavy manufacturing facilities — has historically delivered operating margins in the 40-50% range, placing it among the most profitable equipment companies globally.

What’s Behind the 46.5% Drop? Cyclical Headwinds and Valuation Reset

Understanding the decline from ₩67,800 to today’s ₩36,300 requires examining both macro and company-specific factors.

- Semiconductor capex cyclicality: After an unprecedented surge in capital expenditure by memory and foundry players in 2024–2025, driven by AI infrastructure buildout, the industry has entered a more measured spending phase. Some major customers have deferred or right-sized equipment orders, directly impacting HPSP’s near-term revenue visibility.

- Valuation compression: At its peak, HPSP traded at price-to-earnings (P/E) multiples exceeding 50x — a premium justified by hypergrowth expectations. As growth expectations moderated, the market repriced the stock aggressively. At ₩36,300, the forward P/E has likely compressed to the 20–30x range (depending on 2026–2027 earnings estimates), which is more in line with specialty equipment peers.

- Competition concerns: While HPSP’s dominance remains intact, reports of potential competitive entrants — including efforts by Japanese and domestic Korean equipment firms to develop alternative HPA solutions — have introduced a risk premium. Even if these competitors are years away from viable products, the market has begun discounting the possibility of margin erosion.

- Foreign investor rotation: Broader KOSDAQ weakness and foreign capital outflows from Korean mid-cap growth stocks have added technical selling pressure, exacerbating the drawdown beyond what fundamentals alone might justify.

It’s worth noting that at ₩36,300, the stock is approximately 63% above its 52-week low of ₩22,250, suggesting the market has already found a floor and partially recovered from the worst of the selloff. The current price sits roughly at the midpoint of the 52-week range, which could indicate a period of consolidation as investors reassess the company’s trajectory.

Competitive Moat and Long-Term Growth Drivers

Despite near-term headwinds, HPSP’s structural advantages remain formidable. International investors should weigh the following factors carefully:

1. Technological lock-in and switching costs: Semiconductor fabrication is one of the most process-sensitive industries in the world. Once a chip manufacturer qualifies an equipment vendor for a specific process step, switching to an alternative supplier involves months — sometimes years — of requalification, yield risk, and production disruption. HPSP’s equipment is deeply embedded in the production flows of Samsung, SK hynix, and TSMC. This creates a durable competitive moat that is difficult for new entrants to breach.

2. Expanding addressable market: The transition to gate-all-around (GAA) transistor architectures at 2nm and below is expected to increase the number of HPA steps required per wafer. Additionally, advanced 3D NAND memory (with 300+ layers) demands more annealing steps to manage stress and defect density. Both trends structurally expand HPSP’s total addressable market (TAM) over the medium to long term, regardless of short-term capex fluctuations.

3. Margin resilience: HPSP’s asset-light model and dominant market share give it exceptional pricing power. Even during periods of softer demand, the company has historically maintained operating margins well above 40%. This profitability profile compares favorably to larger, more diversified equipment peers like Tokyo Electron or ASML, which operate at lower margin profiles due to greater operational complexity.

4. Recurring revenue potential: As the installed base of HPSP equipment grows, so does the opportunity for service, maintenance, and upgrade revenue. While this segment is still a relatively small portion of total sales, its growth trajectory adds stability and recurring cash flow to the business model.

For global investors seeking exposure to the semiconductor equipment value chain without the lofty valuations of mega-cap names, HPSP offers a differentiated profile: a small-to-mid-cap company with monopoly-like market share, best-in-class margins, and direct leverage to the most advanced chipmaking processes on the planet.

Key Risks for International Investors

No investment thesis is complete without a candid assessment of risks. For HPSP, several deserve close attention:

- Customer concentration: With a handful of customers representing the vast majority of revenue, the loss or reduced spending by any single client could have an outsized impact on financial performance. Samsung and SK hynix alone likely account for a significant portion of annual orders.

- Emerging competition: While HPSP’s moat is wide, the semiconductor equipment industry is intensely competitive. Japanese firms with deep process technology expertise, as well as Chinese companies benefiting from government subsidies, could eventually develop credible HPA alternatives. Any meaningful loss of market share would severely impact the premium valuation investors assign to the stock.

- Geopolitical risk: U.S.-China semiconductor export controls and evolving trade policies could reshape capital spending patterns in ways that are difficult to predict. If Chinese chipmakers — a potential growth market for HPSP — are restricted from purchasing advanced equipment, it could limit TAM expansion.

- Currency and liquidity considerations: International investors face KRW/USD exchange rate risk. Additionally, as a KOSDAQ-listed mid-cap, HPSP’s daily trading volume may be lower than what large institutional investors require, potentially leading to wider bid-ask spreads and execution challenges.

- Dividend yield: HPSP is a growth-oriented company and does not offer a compelling dividend yield. Investors seeking income from Korean equities would be better served by large-cap names. The investment case here is predicated entirely on capital appreciation driven by earnings growth.

Conclusion: A Compelling Entry Point for Patient, Growth-Oriented Investors

At ₩36,300 — down 46.5% from its 52-week high — HPSP presents an intriguing risk-reward proposition for international investors willing to look past near-term cyclical noise. The company’s near-monopoly in high-pressure annealing, structural tailwinds from advanced node transitions, and exceptional margin profile create a long-term growth story that remains intact despite the recent drawdown.

The valuation reset from peak euphoria to more reasonable levels has arguably made the stock more attractive on a risk-adjusted basis. With the price sitting well above its 52-week low of ₩22,250, the market appears to have established a support level, and the current consolidation phase could represent a window for accumulation.

That said, investors must size their positions carefully given the customer concentration, emerging competition risks, and inherent volatility of mid-cap semiconductor equipment stocks. HPSP is not a defensive holding — it is a high-conviction bet on the continued advancement of semiconductor manufacturing technology. For those with a 3-5 year investment horizon and a tolerance for volatility, the current price level deserves serious consideration.

Disclaimer: This blog post is for informational and educational purposes only and does not constitute financial advice, a recommendation, or a solicitation to buy or sell any security. Investors should conduct their own due diligence, consult with a qualified financial advisor, and consider their individual risk tolerance before making any investment decisions. Market data referenced in this article is as of June 2, 2026, and is subject to change.