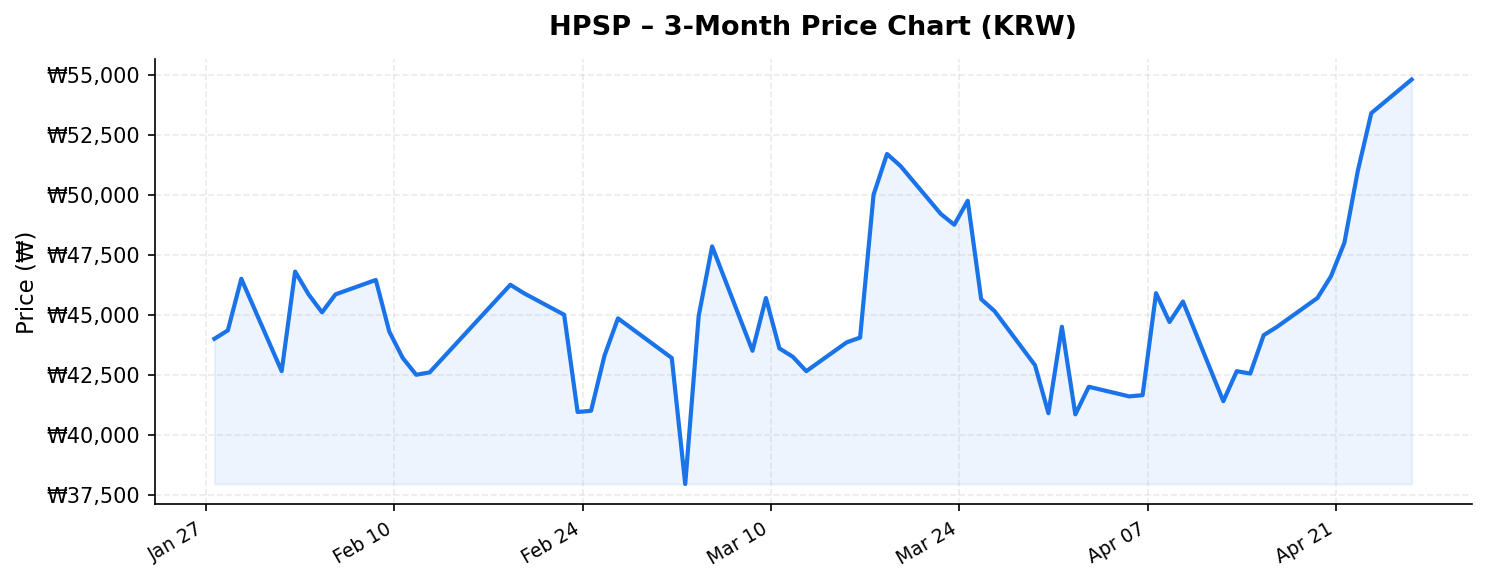

In the fast-evolving world of semiconductor manufacturing, few niche equipment makers have carved out a moat as distinctive as HPSP (HPSP, 403870.KS). The South Korean company dominates the global market for high-pressure annealing (HPA) equipment — a critical process step in advanced chip fabrication. As of April 28, 2026, HPSP shares trade at ₩36,300, sitting a notable 36.8% below their 52-week high of ₩57,400 and well above their 52-week low of ₩21,150. For international investors watching the semiconductor supply chain, this mid-range positioning raises a compelling question: is this a value opportunity in a world-class niche player, or a fair repricing of elevated expectations?

Business Overview: The Quiet Monopolist in High-Pressure Annealing

HPSP is not a household name, even among semiconductor investors. But within the fabrication facilities of the world’s leading chipmakers, its equipment is indispensable. The company designs and manufactures high-pressure annealing systems used primarily in the production of advanced DRAM, NAND flash, and logic semiconductors. High-pressure annealing involves subjecting wafers to elevated temperatures and pressures in a controlled gas environment, improving the quality of thin films and gate oxides — processes that become increasingly critical as transistor geometries shrink below 10 nanometers.

What makes HPSP remarkable is its near-monopoly status. The company commands an estimated 90%+ global market share in dedicated HPA equipment. Its primary customers include Samsung Electronics, SK Hynix, and other major foundry and memory manufacturers. This extraordinary concentration of market share stems from deep technical expertise, long-standing customer relationships, and high switching costs — once an HPA tool is qualified in a fab’s process flow, replacing it with a competitor’s system would require expensive and time-consuming requalification.

The company went public on the KOSDAQ in 2022 and quickly attracted attention from institutional investors drawn to its unique positioning. Revenue has historically been lumpy, driven by capex cycles at a small number of large customers, but the secular trend has been strongly upward as advanced semiconductor nodes increasingly require high-pressure processing steps.

Competitive Position and Growth Drivers

HPSP’s competitive advantages are multifaceted and durable, which is unusual for a company of its size (market capitalization roughly in the ₩2–3 trillion range at current prices). Several structural factors underpin the investment case:

- Near-monopoly market share: With over 90% of the global HPA equipment market, HPSP faces limited direct competition. Potential entrants face steep barriers including proprietary process knowledge, established customer qualifications, and years of field data demonstrating equipment reliability.

- Expanding addressable market: As semiconductor manufacturers push toward gate-all-around (GAA) transistor architectures, advanced 3D NAND with 300+ layers, and high-k metal gate processes in DRAM, the number of high-pressure annealing steps per wafer is increasing. This structural trend means HPSP’s equipment is needed in greater quantities even if the overall number of fab construction projects remains flat.

- High recurring revenue component: Beyond initial equipment sales, HPSP generates meaningful revenue from spare parts, maintenance, and consumables. As the installed base of HPA tools grows globally, this recurring stream provides earnings stability that partially offsets the cyclicality of new tool orders.

- Margin profile: HPSP has historically delivered operating margins in the 40–50% range, reflecting its pricing power and lean cost structure. These margins are exceptional by semiconductor equipment industry standards, where even leading players like ASML or Tokyo Electron typically operate in the 25–35% band.

The company also benefits from the broader geopolitical trend of semiconductor supply chain diversification. As new fabs are built across the United States, Japan, and Europe — often with government subsidies — each facility that incorporates advanced process nodes will likely require HPSP’s HPA equipment, expanding the company’s geographic revenue base beyond its traditional Korean customer stronghold.

Valuation and Price Analysis: What the Numbers Tell Us

At ₩36,300, HPSP sits almost exactly at the midpoint of its 52-week range (₩21,150 to ₩57,400), having recovered substantially from its lows but remaining far from its peak. This positioning suggests the market has already priced in a partial recovery from whatever pessimism drove shares toward ₩21,150, but remains skeptical about a full return to the highs seen within the past year.

The 36.8% discount to the 52-week high is significant and warrants investigation. The decline from peak levels likely reflects several factors: a broader correction in Korean semiconductor-related stocks amid memory pricing volatility, concerns about the timing and magnitude of the next capex upcycle from Samsung and SK Hynix, and some multiple compression as the market moved from pricing in hyper-growth to a more normalized earnings trajectory.

For context, at its 52-week high the stock was likely trading at a forward P/E in the 40–50x range, a premium valuation reflecting its monopoly status and growth potential. At current levels, assuming consensus earnings estimates haven’t drastically changed, the forward P/E has compressed to a more digestible range, potentially in the 25–35x band — still not cheap by traditional value metrics, but arguably reasonable for a company with 90%+ market share, 40%+ operating margins, and a growing addressable market.

The stock’s position at 71.8% above its 52-week low (₩21,150) indicates that the market has already validated a recovery thesis to some degree. Investors entering at current levels are paying a meaningful premium over the trough but still getting a substantial discount versus recent highs — the classic “middle of the range” dilemma that demands a clear-eyed assessment of forward fundamentals.

On the dividend front, HPSP has historically been a modest dividend payer, typical for growth-oriented Korean tech companies. Dividend yield at current prices is likely below 1%, making this primarily a capital appreciation story rather than an income play. International investors seeking yield should look elsewhere; those seeking exposure to a structurally advantaged semiconductor equipment franchise may find the current entry point more interesting.

Key Risks for International Investors

No investment thesis is complete without a thorough examination of risks, and HPSP carries several that international investors should carefully weigh:

- Customer concentration: HPSP derives the vast majority of its revenue from a handful of customers, primarily Samsung Electronics and SK Hynix. A significant capex cut by either customer would materially impact HPSP’s revenues and earnings. This risk is partially structural and unlikely to change given the nature of the memory semiconductor industry.

- Cyclicality: Semiconductor equipment spending is notoriously cyclical. While the secular trend toward more HPA steps per wafer provides a growth floor, HPSP is not immune to the boom-bust patterns of the semiconductor capex cycle. Quarterly results can be volatile, which may test the patience of investors accustomed to smoother earnings profiles.

- Competitive threats: While no direct competitor currently challenges HPSP’s dominance in HPA, larger equipment makers (such as Applied Materials, Tokyo Electron, or Kokusai Electric) could theoretically develop competing systems. Additionally, advances in alternative annealing technologies could over time reduce the need for high-pressure approaches, though this risk appears remote given current technology roadmaps.

- Currency risk: For international investors, the KRW/USD or KRW/EUR exchange rate adds a layer of return volatility. The Korean won has experienced periods of significant weakness, which can erode returns for foreign holders even when the underlying stock performs well.

- Liquidity and small-cap dynamics: As a KOSDAQ-listed company with a relatively modest market cap, HPSP may have lower trading volumes than large-cap Korean stocks. International investors should be mindful of bid-ask spreads and potential difficulty executing large positions without price impact.

- Geopolitical risk: Escalating U.S.-China semiconductor tensions could indirectly affect HPSP if its customers face export restrictions that limit their capacity expansion plans, thereby reducing demand for new HPA equipment.

Investment Thesis: A Rare Niche Monopoly at a More Reasonable Price

For international investors with a medium-to-long-term horizon, HPSP presents a compelling — if not entirely straightforward — investment case. The core thesis rests on three pillars: an unassailable competitive position in a critical and growing semiconductor process step, exceptional profitability that demonstrates genuine pricing power, and a structural tailwind from increasing HPA intensity in next-generation chip manufacturing.

At ₩36,300 and 36.8% off its 52-week high, the stock has shed much of the speculative premium that characterized its peak valuation. This doesn’t make it cheap in absolute terms — investors should expect to pay a premium multiple for monopoly-caliber economics — but it does offer a more favorable risk/reward setup than existed at ₩57,400.

The ideal scenario for a new investor would be entry during a period of capex pessimism (which the current price level may partially reflect) ahead of the next memory and logic investment upcycle. Given that Samsung, SK Hynix, and global foundries continue to commit to aggressive technology roadmaps through the late 2020s, the structural demand for HPSP’s equipment appears intact.

International investors should consider HPSP as a portfolio complement to larger semiconductor equipment holdings — a concentrated, high-conviction position in a rare niche monopoly rather than a core holding. Position sizing should reflect the elevated risks of customer concentration, cyclicality, and KOSDAQ liquidity dynamics.

The 52-week low of ₩21,150 serves as a useful reference point for downside risk estimation, while the 52-week high of ₩57,400 illustrates the upside potential if the next capex cycle arrives with force. At ₩36,300, investors are effectively making a bet that the next major move is more likely to be toward the upper bound than the lower — a bet supported by the company’s structural advantages but tempered by near-term cyclical uncertainty.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice, a recommendation, or a solicitation to buy or sell any securities. Investing in foreign equities involves risks including currency fluctuations, regulatory differences, and market volatility. Readers should conduct their own due diligence and consult a qualified financial advisor before making any investment decisions.