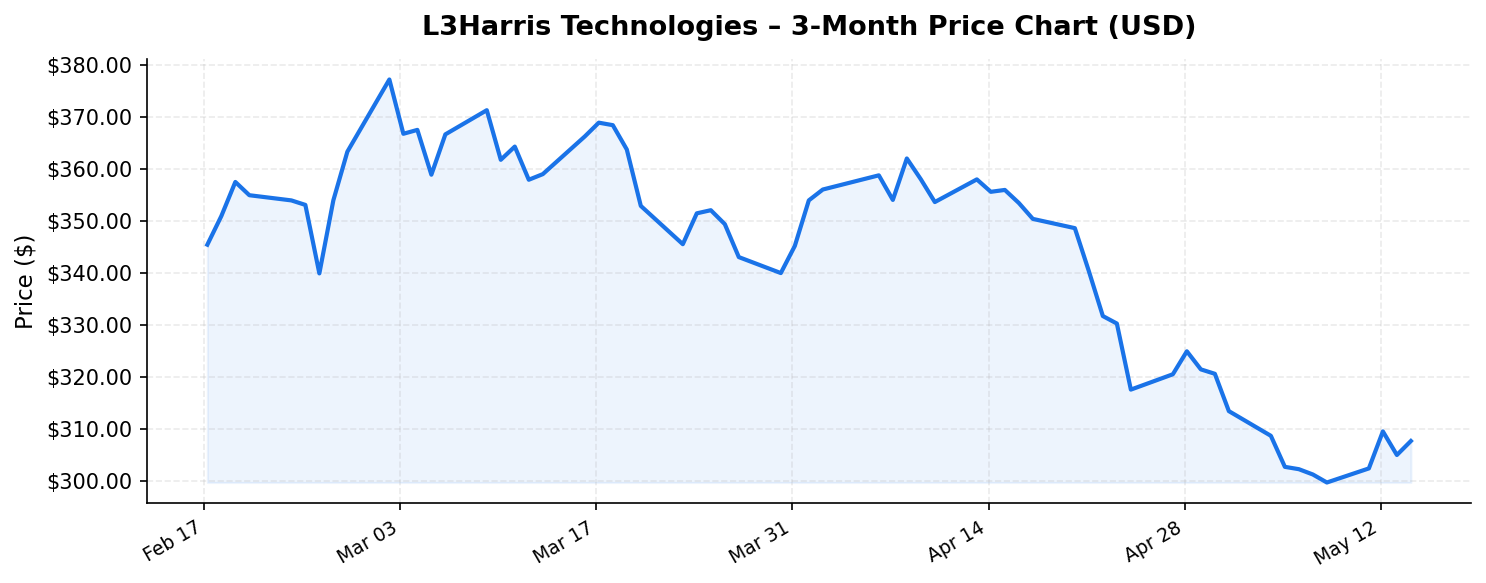

L3Harris Technologies (LHX) occupies a pivotal position in the global defense and aerospace industry, serving as the sixth-largest U.S. defense contractor by revenue. With geopolitical tensions elevated across multiple theaters — from Eastern Europe to the Indo-Pacific — defense spending tailwinds remain robust. But at a current price of $307.62, sitting roughly 18.9% below its 52-week high of $379.23, is LHX a compelling opportunity or a value trap? In this analysis, we break down the company’s fundamentals, competitive moat, risks, and what international investors should consider before adding this name to their portfolios.

Business Overview: A Diversified Defense Powerhouse

L3Harris Technologies was formed through the 2019 merger of L3 Technologies and Harris Corporation, creating a broad-spectrum defense technology company with trailing twelve-month revenue of $12.9 billion. The company operates across four primary segments: Integrated Mission Systems, Space & Airborne Systems, Communication Systems, and Aerojet Rocketdyne (acquired in 2023). Its product portfolio spans tactical radios, electronic warfare systems, intelligence and surveillance platforms, satellite payloads, missile propulsion, and advanced sensors.

What makes L3Harris Technologies distinctive is its positioning as a “sixth prime” — large enough to compete for major platform-level contracts, yet nimble enough to serve as a critical supplier of subsystems and components to larger primes like Lockheed Martin, Northrop Grumman, and Raytheon. This dual role provides revenue diversification and reduces dependence on any single mega-program. The U.S. Department of Defense remains the company’s dominant customer, but L3Harris Technologies also generates meaningful international revenue, with allied nations increasingly turning to American defense firms amid rising security concerns.

With a market capitalization of $57.3 billion, L3Harris Technologies is firmly in large-cap territory, offering the liquidity and institutional coverage that international investors typically seek when allocating to U.S. equities.

Valuation and Market Position: Parsing the Numbers

At $307.62 per share, LHX trades at a price-to-earnings ratio of 33.4x, which is notably above the defense sector median of approximately 20-24x. This premium valuation demands scrutiny. Part of the elevated P/E likely reflects integration costs and amortization charges related to the Aerojet Rocketdyne acquisition, which can temporarily depress reported earnings. If we adjust for non-recurring items and acquisition-related accounting, the normalized earnings multiple is likely more reasonable — though still not cheap by historical defense sector standards.

The price-to-book ratio of 2.99x is relatively in line with peers, reflecting the significant goodwill and intangible assets on L3Harris Technologies’ balance sheet following its M&A-driven growth strategy. International investors should note that high goodwill balances are common among defense consolidators but do introduce impairment risk if integration synergies fail to materialize.

Perhaps the most eye-catching data point is the reported dividend yield of 163.00%. This figure almost certainly reflects a data anomaly — potentially a special distribution, a stock split adjustment, or a reporting error in the feed. For context, L3Harris Technologies has historically paid a quarterly dividend yielding approximately 2.0-2.5% annually, and the company has a strong track record of dividend growth, having increased its payout for over 20 consecutive years. International investors should verify the actual current annual dividend per share through the company’s investor relations page or their brokerage platform before making any investment decision based on yield assumptions. If the actual yield is in the 2.0-2.5% range, it remains attractive relative to the broader S&P 500 average of approximately 1.3%, and the consistency of increases adds a compounding element that income-oriented investors will appreciate.

Looking at the stock’s position within its 52-week range of $226.47 to $379.23, the current price of $307.62 sits in the upper-middle portion of the range — about 36% above the 52-week low but 18.9% below the peak. This suggests the stock has recovered meaningfully from its lows but has given back gains from its highs, potentially offering a more attractive entry point than was available at peak pricing.

Competitive Strengths and Growth Catalysts

L3Harris Technologies benefits from several structural advantages that international investors should weigh:

- Mission-critical technology moats: The company’s tactical communications systems, including the Falcon series of radios, are deeply embedded in U.S. and allied military operations. Switching costs are exceptionally high, creating recurring revenue streams through upgrades, maintenance, and new variants.

- Rising global defense budgets: NATO members are accelerating their commitments to spend 2% or more of GDP on defense. The U.S. defense budget continues to grow, with bipartisan support. This macro backdrop provides a multi-year revenue tailwind for the entire sector, and L3Harris Technologies is well-positioned to capture its share.

- Aerojet Rocketdyne integration: The 2023 acquisition of Aerojet Rocketdyne added solid rocket motor and missile propulsion capabilities — a strategically critical supply chain node. As the U.S. and allies seek to replenish missile inventories, this segment could become a significant growth driver. Synergy targets from the acquisition remain a near-term catalyst for margin expansion.

- Space and electronic warfare growth: L3Harris Technologies is a leading provider of space-based sensors and payloads for the U.S. Space Force, as well as advanced electronic warfare systems. Both areas are receiving outsized budget allocations as the Pentagon prioritizes space domain awareness and electromagnetic spectrum operations.

- International sales expansion: With allied nations in Europe, the Middle East, and the Asia-Pacific ramping defense procurement, L3Harris Technologies’ international order book is growing. The company’s communications and ISR (intelligence, surveillance, and reconnaissance) products are particularly well-suited for export.

From a revenue perspective, the $12.9 billion TTM figure represents solid top-line scale, and management has guided for mid-single-digit organic revenue growth in the near term, supplemented by margin expansion as integration efficiencies take hold.

Key Risks for International Investors

No defense investment is without risk, and international investors face some unique considerations with LHX:

- Valuation risk: At 33.4x earnings, the stock is priced for execution. Any disappointment in integration synergies, contract wins, or margin trajectory could trigger a multiple compression. The premium P/E leaves limited room for error.

- Budget and political risk: While defense spending enjoys bipartisan support, continuing resolution cycles, government shutdowns, and shifting political priorities can create near-term funding uncertainty. Any meaningful pivot toward fiscal austerity could pressure defense stocks broadly.

- Currency risk: International investors purchasing LHX in U.S. dollars are exposed to USD fluctuations. A strengthening home currency relative to the dollar would erode returns when converted back, even if the stock price appreciates in dollar terms.

- Concentration risk: The U.S. government accounts for the majority of L3Harris Technologies’ revenue. While this provides stability, it also means the company’s fortunes are closely tied to a single customer’s procurement decisions.

- Integration execution: The Aerojet Rocketdyne acquisition is still being integrated. Large defense mergers have historically faced challenges in achieving projected synergies on schedule. Any delays or cost overruns could weigh on profitability and investor sentiment.

- ESG and ethical screening: Many international institutional investors and funds apply ESG screens that exclude defense and weapons manufacturers. This can limit the buyer base for LHX and create selling pressure if ESG mandates tighten further in key markets like Europe.

Investment Thesis: Is LHX a Buy for International Portfolios?

L3Harris Technologies presents a nuanced case for international investors. On the positive side, the company operates in a structurally growing market, holds defensible competitive positions in mission-critical technologies, and offers a reliable (and growing) dividend — a relatively rare combination in the defense sector. The stock’s 18.9% discount to its 52-week high provides a more favorable entry point than recent peaks, and the macro environment of rising global defense spending is firmly supportive.

On the other hand, the 33.4x P/E multiple requires confidence that earnings will grow into the valuation through synergy realization, organic growth, and margin expansion. International investors must also factor in currency exposure and the reality that defense stocks carry unique political and regulatory risks that differ from typical industrial or technology investments.

For long-term investors with a multi-year horizon, L3Harris Technologies offers exposure to one of the most durable secular trends in global markets — the rearming of Western democracies. The company’s diversified portfolio, growing international footprint, and disciplined capital allocation (including consistent dividend increases) make it a credible core holding for investors seeking defense sector exposure. However, position sizing should reflect the premium valuation and the inherent concentration risks tied to government spending.

International investors should also conduct due diligence on the reported 163% dividend yield figure, which appears anomalous. If the true yield is in the historically consistent 2.0-2.5% range, LHX remains an above-average income generator with a strong growth overlay — but this data point warrants verification before it factors into any investment decision.

Disclaimer: This blog post is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any securities. Investors should conduct their own research and consult with a qualified financial advisor before making investment decisions. Market data referenced is as of May 15, 2026, and may be subject to change or contain inaccuracies.