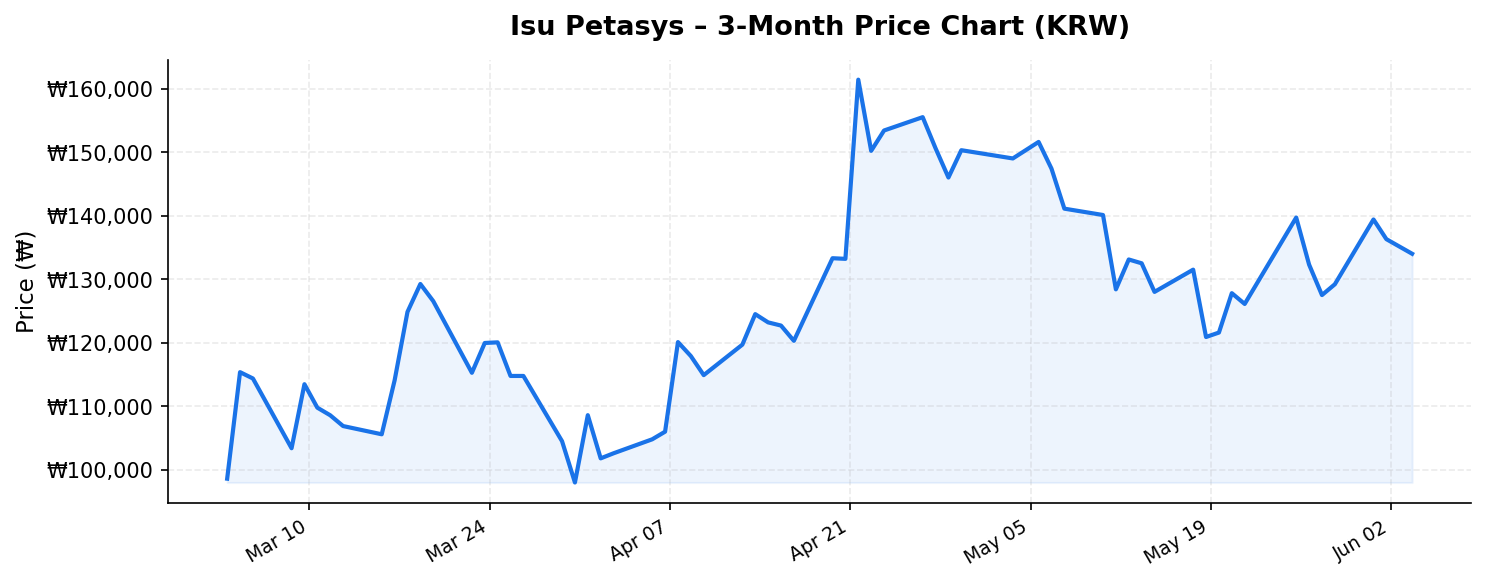

In a market where technology hardware companies often trade at nosebleed valuations with negligible dividends, Isu Petasys (이수페타시스, 007660.KS) stands out as a striking anomaly. The Korean printed circuit board (PCB) specialist currently trades at ₩133,900 per share with a market capitalization of ₩9.8 trillion (~$7.2 billion USD), and it’s offering investors a remarkable 17.00% dividend yield. With a return on equity of 29.9% and trailing twelve-month revenue of ₩1.2 trillion, Isu Petasys has transformed from a mid-cap industrial supplier into one of the most compelling stories on the Korea Exchange. But is this too good to be true, or is there a fundamental thesis that justifies these numbers? Let’s break it down.

Business Overview: From Niche PCB Maker to AI Infrastructure Beneficiary

Isu Petasys is a subsidiary of the Isu Group, one of South Korea’s mid-tier conglomerates. The company specializes in the manufacture of multilayer printed circuit boards (MLB PCBs), which are essential components embedded in virtually every electronic device — from servers and networking equipment to automotive electronics and telecommunications infrastructure. What has catapulted the company into the spotlight, however, is its strategic positioning in the high-layer-count PCB segment used in AI servers, high-performance computing (HPC), and next-generation networking switches.

As global demand for AI infrastructure has surged — driven by hyperscaler capital expenditure from the likes of Microsoft, Google, Amazon, and Meta — the need for advanced PCBs capable of handling higher signal integrity, greater thermal management, and more complex routing has exploded. Isu Petasys has emerged as one of the few manufacturers globally capable of producing 30+ layer PCBs at scale with the quality standards demanded by Tier 1 OEMs and ODMs. This has placed the company squarely in the supply chain for Nvidia’s GPU server platforms, particularly through partnerships with server assemblers and major Korean electronics conglomerates.

The company’s TTM revenue of ₩1.2 trillion represents a dramatic escalation from just a few years ago, when annual sales hovered in the ₩300-400 billion range. This revenue trajectory underscores the structural demand tailwinds the company is riding, rather than a one-off cyclical bump.

Valuation, Price Action, and That Extraordinary Dividend Yield

At ₩133,900, Isu Petasys sits approximately 18.6% below its 52-week high of ₩164,400 and a staggering 241% above its 52-week low of ₩39,200. This range alone tells a story of explosive re-rating: the stock has been one of the best performers on the KOSPI over the past year as the market has aggressively repriced the company’s earnings power in the AI era.

The current pullback from the 52-week high may actually represent an attractive entry point for investors who missed the initial run-up. A nearly 19% drawdown from peak levels, in the context of a stock that has more than tripled from its lows, could be interpreted as healthy consolidation rather than a trend reversal — particularly if the fundamental growth drivers remain intact.

The headline number that will immediately catch income-oriented investors’ attention is the 17.00% dividend yield. This is extraordinarily high by any global standard, and especially unusual for a technology-adjacent growth company. Several factors likely explain this yield. First, Isu Petasys has historically maintained a generous dividend payout policy, and the surge in profitability — reflected in the 29.9% ROE — has allowed the company to dramatically increase absolute dividend payments. Second, there may be elements of special dividends or one-time distributions that inflate the trailing yield figure. International investors should carefully examine whether this yield is sustainable on a forward basis or whether it reflects a one-time capital return event.

Even if the forward yield normalizes to, say, 8-10%, that would still place Isu Petasys among the most generous dividend payers in the global technology sector. Combined with the growth profile, this creates a rare “growth plus income” proposition that is difficult to find elsewhere.

From a valuation perspective, the price-to-sales ratio based on the ₩9.8 trillion market cap and ₩1.2 trillion in TTM revenue works out to roughly 8.2x. For a PCB manufacturer, this is elevated relative to historical norms — traditional PCB companies globally trade at 1-3x sales. However, Isu Petasys is clearly being valued as an AI infrastructure play rather than a commodity PCB maker, and in that context, the multiple is more justifiable when compared to peers in the AI supply chain that trade at double-digit revenue multiples.

Competitive Position and Structural Advantages

The global PCB industry is highly fragmented, with major production concentrated in Taiwan, China, Japan, and South Korea. Isu Petasys competes against established players like Unimicron and Nan Ya PCB in Taiwan, Ibiden and Shinko Electric in Japan, and domestic rival Samsung Electro-Mechanics. What differentiates Isu Petasys is its focused specialization in high-layer-count, high-frequency PCBs — a niche that requires significant technical expertise, capital investment, and rigorous quality control.

Barriers to entry in this segment are meaningful. Producing 30+ layer PCBs with the yield rates and reliability demanded by AI server platforms requires years of process optimization, proprietary manufacturing know-how, and deep customer qualification cycles. Once a PCB supplier is designed into a server platform, switching costs are high, as any change requires extensive revalidation and testing. This creates a degree of customer lock-in that provides revenue visibility and pricing power.

Isu Petasys has also benefited from the “Korea discount” working in reverse — as geopolitical tensions between the U.S. and China have prompted supply chain diversification away from Chinese manufacturers, Korean suppliers have gained share. The company’s geographic positioning in South Korea, a close U.S. ally with robust intellectual property protections, makes it a preferred partner for Western hyperscalers seeking to de-risk their supply chains.

The 29.9% return on equity is a testament to the company’s operational efficiency and the favorable unit economics of its product mix. High-layer-count PCBs command significantly higher average selling prices (ASPs) and margins compared to commodity boards, and Isu Petasys’s product shift toward these premium segments has driven substantial margin expansion.

Key Risks for International Investors

Despite the compelling growth narrative, several risks warrant careful consideration:

- AI Capex Cyclicality: The current AI infrastructure build-out is unprecedented, but history teaches us that technology investment cycles can be volatile. Any deceleration in hyperscaler spending — whether due to macroeconomic headwinds, overcapacity concerns, or a shift in AI development paradigms — would directly impact demand for Isu Petasys’s products. The stock’s 241% appreciation from its 52-week low already prices in significant growth expectations.

- Dividend Sustainability: A 17% yield is exceptional, but investors must assess whether it reflects a sustainable payout policy or a one-time distribution. If earnings growth plateaus or reverses, maintaining such a high payout could strain the balance sheet or signal that management sees limited reinvestment opportunities.

- Customer Concentration: Companies riding the AI wave often derive a large share of revenue from a small number of hyperscaler-linked customers. Any loss of a key account or a shift in platform design that favors alternative PCB architectures (such as substrate-like PCBs or silicon interposers) could meaningfully impact revenue.

- Currency Risk: International investors are exposed to KRW/USD fluctuations. A strengthening Korean won could boost returns for foreign holders, while depreciation would erode them. The won has been volatile in recent years, adding an additional layer of uncertainty.

- Valuation Premium: At over 8x sales, the stock is priced for perfection. Any earnings miss or guidance reduction could trigger a sharp correction, as the market has limited tolerance for disappointment at these multiples.

- Liquidity and Access: While Isu Petasys is listed on the KOSPI and accessible through most international brokerage platforms that offer Korean market access, foreign investors may face settlement and tax withholding complexities. Korea imposes a withholding tax on dividends paid to non-residents, which would reduce the effective yield.

Investment Thesis: A Rare Convergence of Growth, Income, and Structural Tailwinds

For international investors seeking exposure to the AI infrastructure theme beyond the obvious names like Nvidia, TSMC, or Broadcom, Isu Petasys offers a differentiated entry point through the critical but often-overlooked PCB layer of the technology stack. The company’s TTM revenue of ₩1.2 trillion, ROE of 29.9%, and 17% dividend yield represent a rare convergence of growth and income characteristics that few AI-adjacent companies can match globally.

The stock’s current price of ₩133,900, sitting 18.6% below its 52-week high, may represent a reasonable entry point for long-term investors willing to ride out near-term volatility. The structural demand drivers — AI server proliferation, network infrastructure upgrades, supply chain diversification — are multi-year themes that provide a strong foundation for continued revenue growth.

However, this is not a risk-free proposition. The elevated valuation, questions around dividend sustainability, and the inherent cyclicality of technology hardware spending demand a measured approach. Position sizing should reflect both the upside potential and the downside risks. Investors would be well-served by monitoring quarterly earnings for signs of order backlog trends, margin sustainability, and management’s forward guidance on capital allocation and dividends.

Isu Petasys has executed a remarkable transformation from a niche industrial supplier to a globally relevant AI infrastructure beneficiary. Whether the stock can sustain its momentum will ultimately depend on the durability of the AI build-out cycle and the company’s ability to defend its competitive moat in high-complexity PCB manufacturing. For those who believe in the long-term trajectory of AI infrastructure spending, this Korean small-to-mid-cap-turned-large-cap deserves a place on the watchlist — if not in the portfolio.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or an offer to buy or sell any securities. All data is based on publicly available information as of June 4, 2026, and may not reflect the most current developments. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.